- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Tronox Holdings (TROX) Valuation After Recent Pullback And Mixed Fair Value Signals

Recent price move puts Tronox in focus

Tronox Holdings (TROX) is back on many watchlists after a recent pullback, with the stock down about 13% over the past month but still showing a positive return over the past 3 months.

See our latest analysis for Tronox Holdings.

The recent slide, with a 7 day share price return of down 14.79% and 30 day share price return of down 12.83%, contrasts with Tronox Holdings’ strong year to date share price return of 86.18% and 1 year total shareholder return of 56.71%. However, longer term total shareholder returns over 3 and 5 years remain weak, suggesting short term momentum is fading after a strong rebound.

If you are comparing Tronox with other materials and industrial related ideas, this could be a good moment to scan for opportunities across 8 top copper producer stocks

With Tronox trading close to analyst targets, showing a large intrinsic discount estimate but carrying recent losses and weak multi year returns, should you see value that the market is missing or assume that future growth is already priced in?

Most Popular Narrative: 1% Overvalued

Tronox's most followed narrative pegs fair value at about $7.88, almost level with the last close at $7.95. This puts the focus squarely on the underlying earnings story and what has to go right to justify that number.

The company's ongoing cost improvement program and operational efficiency initiatives, including vertical integration and strategic mining investments, are anticipated to deliver $125 million to $175 million in sustainable annual savings by the end of 2026 and lower unit feedstock costs in 2026, which should enhance net margins and overall profitability beyond current expectations.

Want to see what is backing that tight gap between fair value and price? The narrative leans heavily on revenue resilience, margin repair, and a leaner cost base. Curious how those moving parts get translated into a discounted cash flow at an 11% hurdle rate, and what kind of future profit multiple that implies for a still unprofitable stock?

Result: Fair Value of $7.88 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still plenty that can go wrong, with high net leverage of about US$2.9b and tougher regulation potentially squeezing already weak profitability.

Find out about the key risks to this Tronox Holdings narrative.

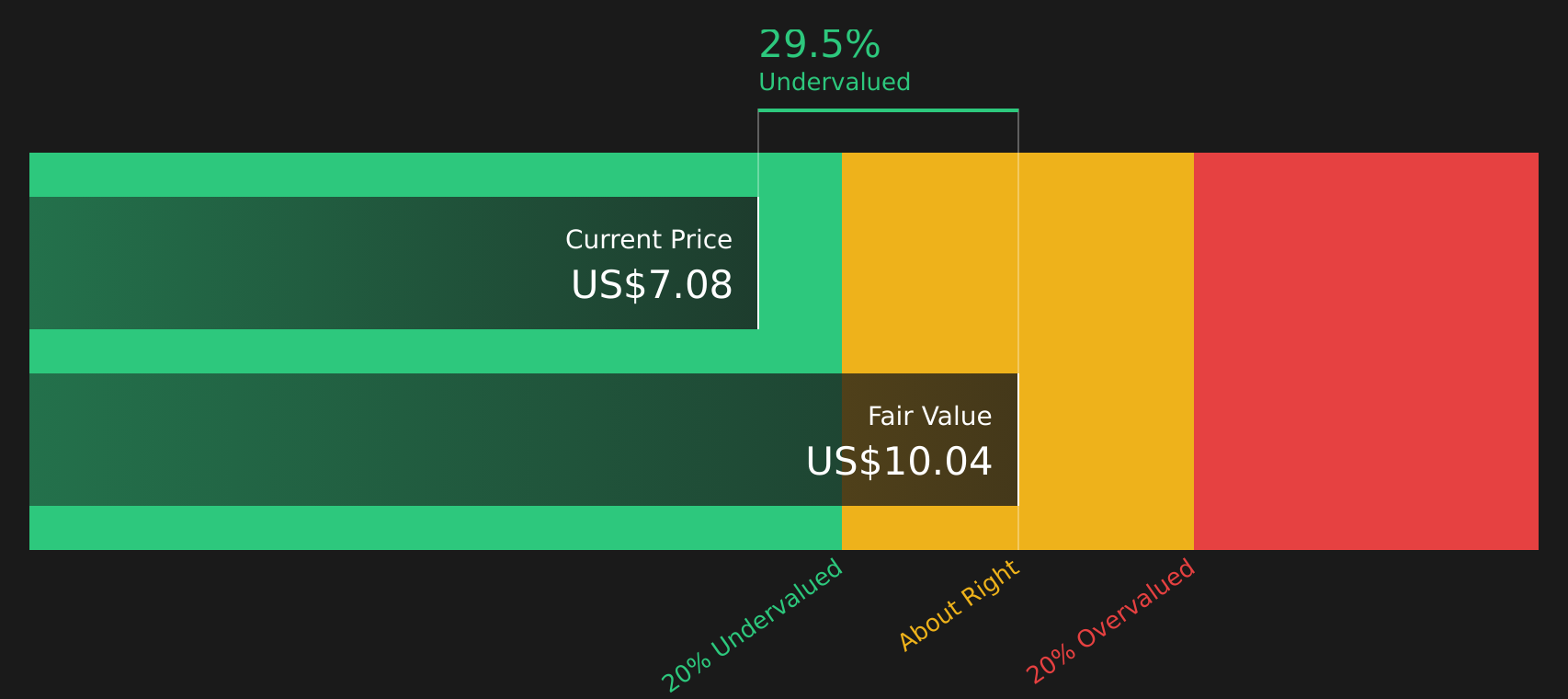

Another way to look at value

The SWS DCF model presents a very different picture. It shows Tronox trading at a large discount to an estimated future cash flow value of $17.38, while the most popular narrative views the stock as slightly overvalued around $7.88. Which story do you think lines up better with the risks on the table?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With mixed signals on value and sentiment, it helps to look past headlines and check the underlying data yourself. To weigh the potential upside against the downside in a balanced way, start with the 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your goals even better, so use the tools available and keep your watchlist sharp.

- Scan for potential bargains that pair quality with attractive pricing by checking the 52 high quality undervalued stocks.

- Strengthen your income focus by reviewing companies in the 12 dividend fortresses that offer higher yields with supporting fundamentals.

- Reduce portfolio stress by searching for companies in the 65 resilient stocks with low risk scores that score well on resilience and financial stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com