- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

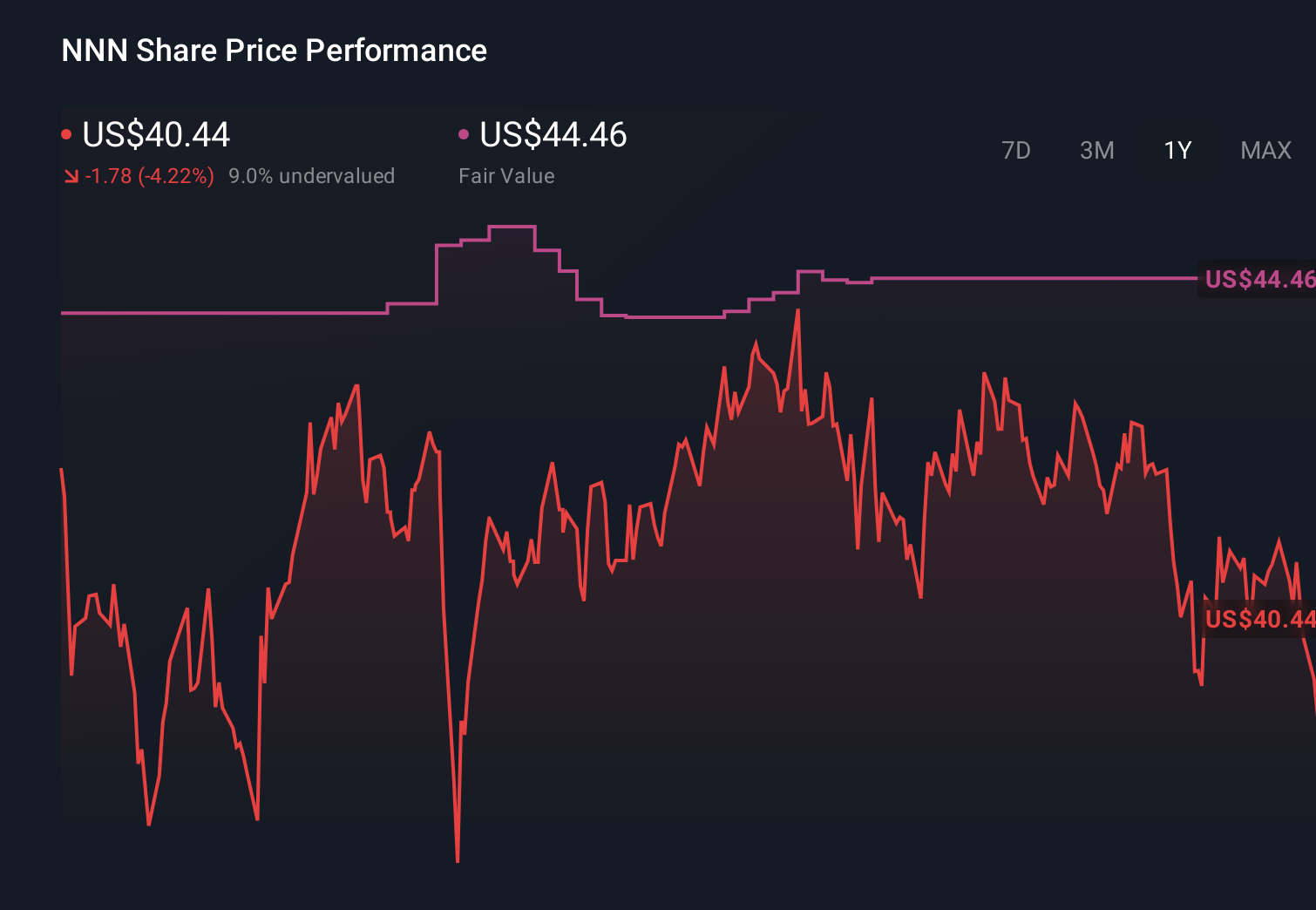

How Investors May Respond To NNN REIT (NNN) Using Asset Sales To Upgrade Its Portfolio

- Earlier in May 2026, NNN REIT reported Q1 results and outlined a more proactive asset sale program, supported by US$1.20 billion of liquidity and long-dated debt averaging nearly 11 years.

- Management also raised its 2026 AFFO per share guidance, signaling that planned asset sales are intended to upgrade portfolio quality rather than simply shrink the balance sheet.

- Next, we’ll examine how this renewed focus on portfolio-enhancing asset sales could influence NNN REIT’s existing investment narrative.

Find 52 companies with promising cash flow potential yet trading below their fair value.

NNN REIT Investment Narrative Recap

To own NNN REIT, you need to believe in a steady, income-focused retail REIT that can balance disciplined growth with careful risk management. The latest Q1 update, including higher 2026 AFFO guidance and a more proactive asset sale program funded by US$1.20 billion of liquidity and long-dated debt, appears to support the near term earnings and dividend story. It does not materially change the biggest current risk, which is tenant and bad debt exposure in a still-challenging retail backdrop.

Among recent announcements, the Board’s decision to maintain the quarterly dividend at US$0.60 per share stands out in light of the refreshed asset sale plan. For investors, a consistent dividend alongside portfolio-enhancing dispositions and raised AFFO guidance ties directly into the main catalyst: whether NNN can use self-funded recycling to support earnings and keep its high payout level sustainable without leaning heavily on more expensive external capital.

Yet beneath the reassuring liquidity and dividend headlines, tenant risk and potential retailer bankruptcies remain a factor investors should be aware of as...

Read the full narrative on NNN REIT (it's free!)

NNN REIT's narrative projects $1.1 billion revenue and $451.6 million earnings by 2029. This requires 4.7% yearly revenue growth and about a $65.1 million earnings increase from $386.5 million today.

Uncover how NNN REIT's forecasts yield a $45.97 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$46 to US$81, showing how far apart individual views on NNN REIT can be. When you weigh those opinions against the company’s increased focus on portfolio-enhancing asset sales and higher 2026 AFFO guidance, it underlines why exploring several contrasting views can be helpful before judging how resilient that earnings path might be.

Explore 2 other fair value estimates on NNN REIT - why the stock might be worth just $45.97!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NNN REIT research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NNN REIT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NNN REIT's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com