- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How HELIOS-B Phase 3 Vutrisiran Data and Real-World Evidence Expansion Will Impact Alnylam (ALNY) Investors

- Earlier in May 2026, Alnylam Pharmaceuticals reported new HELIOS-B Phase 3 analyses showing vutrisiran delivered durable transthyretin knockdown, consistent clinical benefits across high-risk ATTR-CM subgroups, and low, placebo-like vitamin A-related ocular event rates over more than 25,000 patient-years of exposure.

- The company also launched the large DemonsTTRate real-world outcomes study and highlighted over 13,000 patient-years of global vutrisiran experience, deepening the clinical evidence base for its transthyretin franchise in both cardiomyopathy and polyneuropathy.

- We’ll now examine how HELIOS-B’s robust outcomes in high-risk ATTR-CM patients may influence Alnylam’s existing investment narrative around its TTR portfolio.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you essentially need to believe its RNAi TTR franchise can keep growing despite pricing pressure and heavy reliance on AMVUTTRA. The key near term catalyst remains execution in ATTR-CM, while the biggest current risk is that concentrated TTR revenues face margin compression and payer pushback. The latest HELIOS-B data strengthen the clinical case for vutrisiran but do not fundamentally change that risk reward balance in the short term.

Among recent developments, the Q1 2026 results stand out alongside HELIOS-B. Alnylam reported US$1,167.18 million in quarterly revenue and US$205.99 million in net income and reiterated 2026 guidance, including US$4.4 billion to US$4.7 billion from TTR products. For investors, this pairing of strong, TTR-driven financials with additional Phase 3 and real world support for vutrisiran is central to assessing how durable that TTR dependence may be if competitive or pricing pressures intensify.

But against this strength, investors should also be aware of the growing pressure on AMVUTTRA net pricing and margins...

Read the full narrative on Alnylam Pharmaceuticals (it's free!)

Alnylam Pharmaceuticals' narrative projects $7.0 billion revenue and $1.9 billion earnings by 2028.

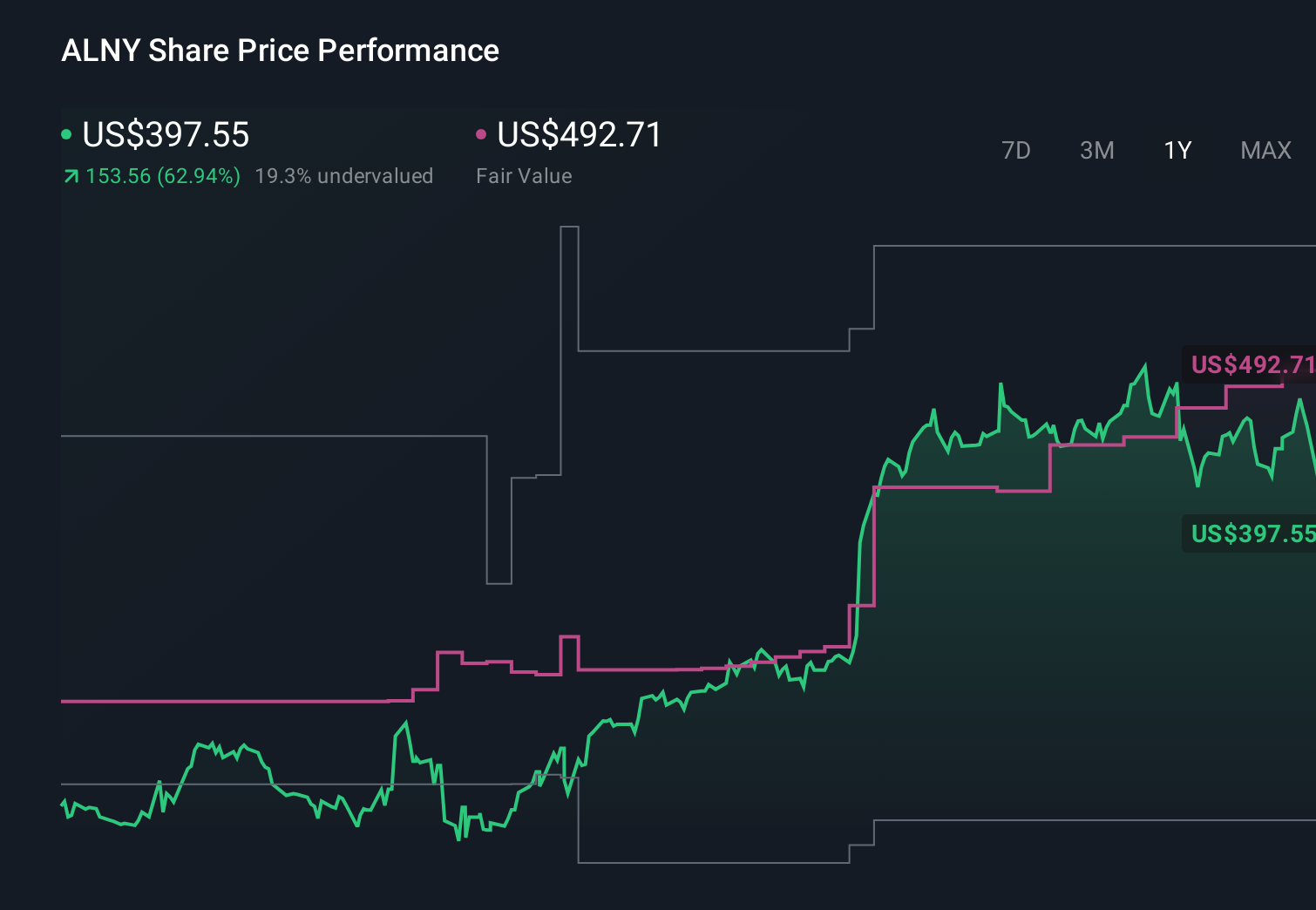

Uncover how Alnylam Pharmaceuticals' forecasts yield a $491.92 fair value, a 72% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Alnylam could reach about US$11.5 billion in revenue and US$3.4 billion in earnings by 2029, which is a far more aggressive path than consensus. In light of the new HELIOS B data and the risk that AMVUTTRA pricing and margins could erode, you may find it useful to compare how that bullish view could shift against more conservative expectations.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth just $311.72!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

No Opportunity In Alnylam Pharmaceuticals?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 52 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 43 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com