- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Entergy’s Valuation After New Hyundai Steel And Posco Power Supply Agreement

Entergy’s new industrial power deal

Entergy (ETR) has agreed to supply electric services to Hyundai Steel and Posco’s upcoming electric arc furnace mill in Donaldsonville, Louisiana, tying the utility to Hyundai Motor Group’s first North American steelmaking project.

See our latest analysis for Entergy.

Despite a recent pullback, with a 7 day share price return of around 3% lower and a 30 day share price return down about 5.1%, Entergy’s year to date share price return of 16.8% and 1 year total shareholder return of 35.4% suggest momentum has been stronger over longer periods as investors weigh industrial growth deals like the Hyundai Steel and Posco project against broader utility sector risks.

If this agreement has you thinking about power infrastructure more broadly, it could be worth widening your search with our curated list of 35 power grid technology and infrastructure stocks

With Entergy trading at US$109.58 against an average analyst price target near US$122.93 and an internal intrinsic value estimate that is higher again, should you see an undervalued utility here, or assume markets are already pricing in future growth?

Most Popular Narrative: 9% Undervalued

Entergy’s most followed valuation narrative puts fair value at about $119.83 per share, above the last close of $109.58. This sets up a clear gap for investors to assess.

Substantial long term electricity demand growth is expected from industrial development, population migration to the Gulf South, and large scale data center expansions in Entergy's service territory, potentially driving robust load growth and higher regulated revenues.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue trajectory and margin profile would need to line up with that outlook, and what earnings multiple the narrative leans on to reach its fair value? The answer ties together growth assumptions, profitability targets, and a richer future valuation that might surprise investors used to typical utility pricing.

Result: Fair Value of $119.83 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still a few pressure points to watch, especially Entergy’s significant Gulf South exposure to extreme weather and the funding needs of its sizeable capital plan.

Find out about the key risks to this Entergy narrative.

Another angle on valuation

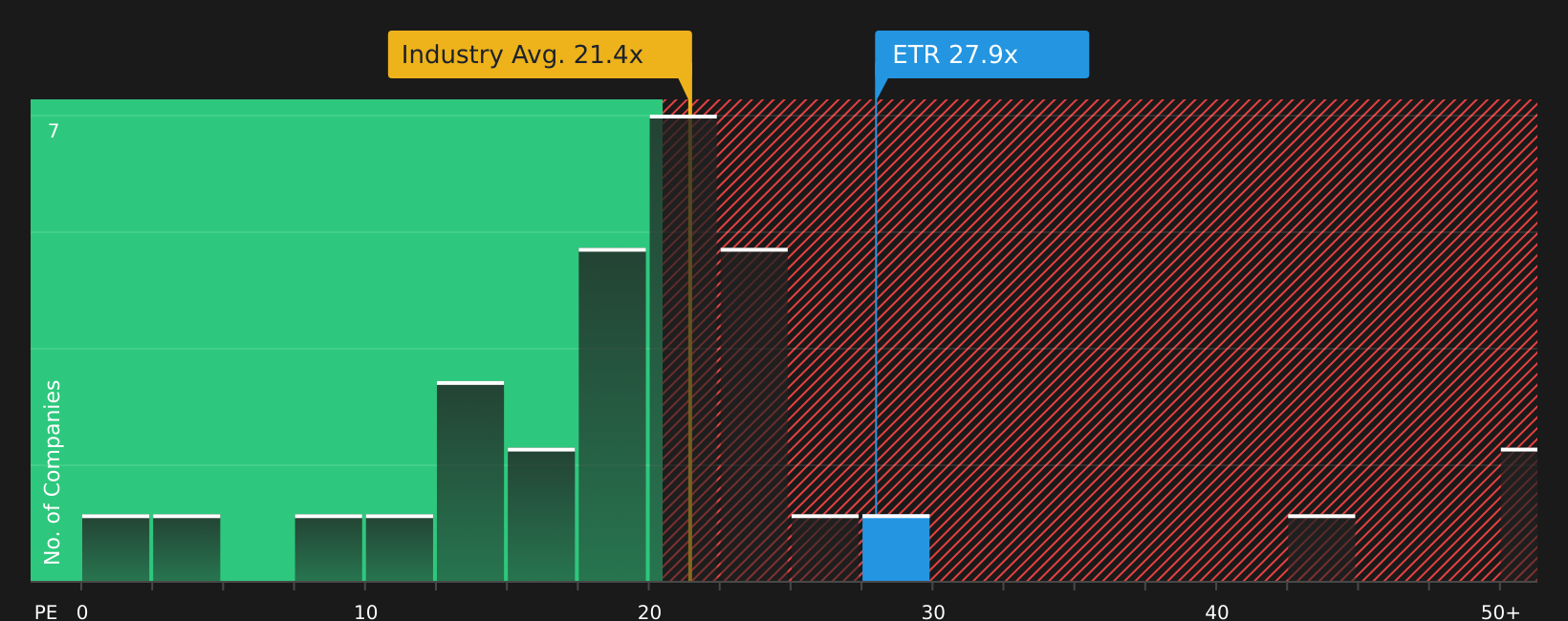

The fair value narrative points to Entergy trading below an estimated value of $119.83, but the simple P/E picture looks tighter. At about 28.1x earnings, the stock is roughly in line with a fair ratio of 28.1x while sitting well above the US Electric Utilities industry at 20.9x and a peer average of 17.7x. That kind of premium can reflect confidence or crowding, so how comfortable are you paying up for this story?

For a closer look at how this earnings multiple stacks up against what the market could move toward as a fair ratio, and how that affects both upside and downside room, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mix of optimism and caution in this story feels familiar, move quickly and look at the data for yourself to decide where you stand by weighing the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If you are serious about growing your portfolio, do not stop at a single utility stock when there are other focused idea lists ready to scan.

- Target higher income potential by reviewing companies in the 12 dividend fortresses that could suit a yield focused approach.

- Hunt for potential bargains across sectors with the 51 high quality undervalued stocks and see which stocks line up with your return and risk expectations.

- Prioritise resilience by checking companies in the 65 resilient stocks with low risk scores that match your comfort level when markets get choppy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com