- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Should Textron’s Expanded Melbourne Facility and New Government Orders Require Action From Textron (TXT) Investors?

- Textron’s aviation businesses recently expanded their footprint and order book, including a larger Melbourne service facility and new aircraft orders from Life Flight Network and the U.S. Department of Agriculture.

- These moves deepen Textron’s aftermarket service reach and highlight continuing demand for its aircraft in both emergency medical transport and specialized government programs.

- We’ll now examine how the expanded Melbourne service facility shapes Textron’s existing investment narrative around aviation aftermarket growth.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Textron Investment Narrative Recap

To own Textron, you need to believe in its shift toward a focused aerospace and defense company, with aviation aftermarket growth and Bell’s helicopter programs doing much of the work. The expanded Melbourne facility supports the aftermarket catalyst but does not materially change the near term picture. The bigger swing factor remains execution on the Industrial separation, while cost control and product mix, especially in Aviation, still sit at the top of the current risk list.

Within the latest announcements, the Melbourne expansion stands out as most relevant here. It adds capacity to serve more than 1,400 aircraft across Australia and Asia Pacific, directly tying into Textron Aviation’s aftermarket opportunity. For investors watching whether higher margin services can offset mix and cost pressures, this new facility is a tangible, incremental data point rather than a game changer by itself.

Yet, against this progress, investors should still keep a close eye on how rising geopolitical and tariff risks could...

Read the full narrative on Textron (it's free!)

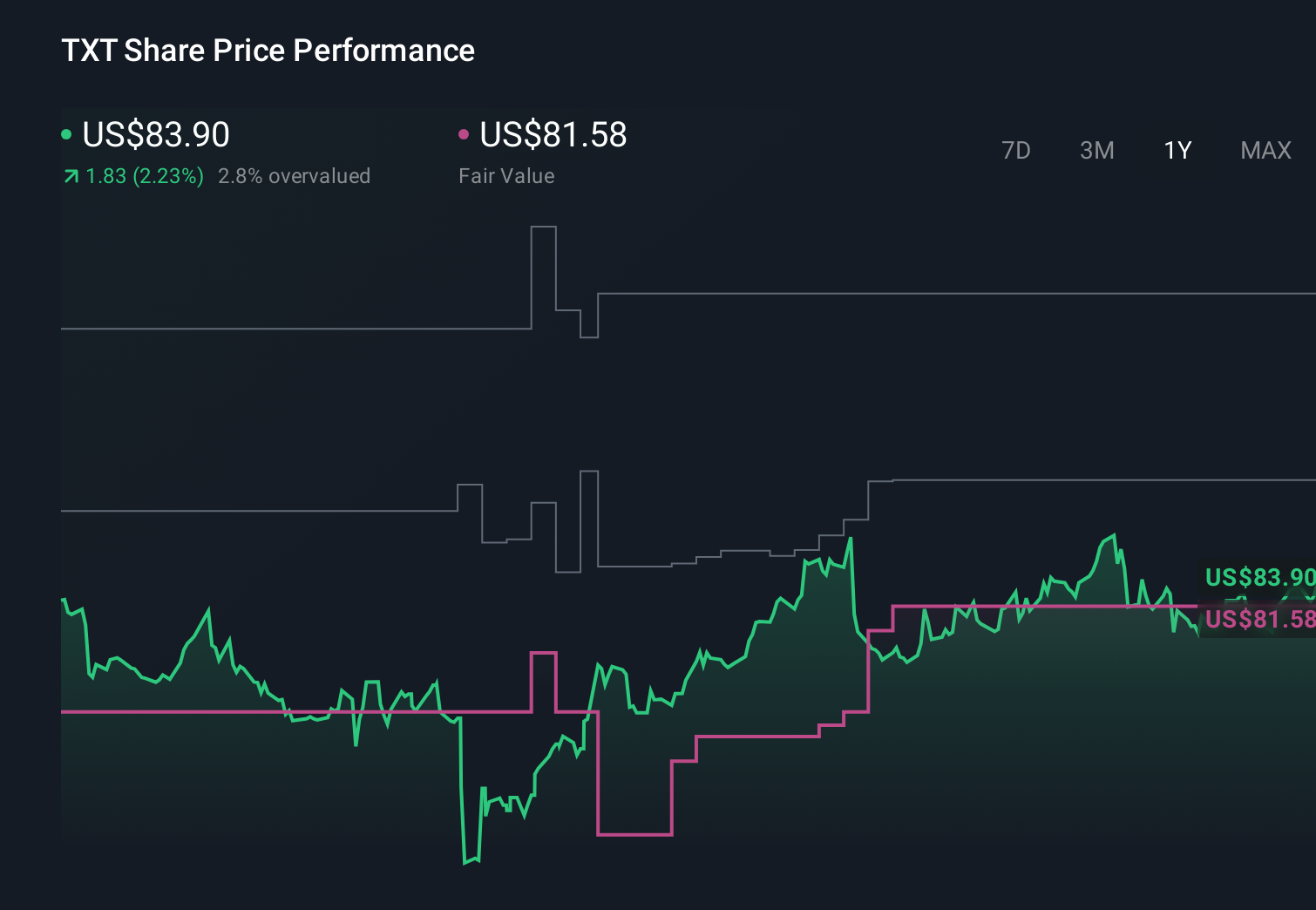

Textron’s narrative projects $16.7 billion revenue and $1.2 billion earnings by 2029. This requires 4.2% yearly revenue growth and a roughly $300 million earnings increase from $923.0 million today.

Uncover how Textron's forecasts yield a $98.95 fair value, a 9% upside to its current price.

Exploring Other Perspectives

While the consensus story leans on steady aftermarket growth, the most optimistic analysts see up to US$17.3 billion of revenue and US$1.2 billion of earnings, and view moves like Melbourne as potential proof points that could either reinforce or challenge their far more bullish expectations.

Explore 5 other fair value estimates on Textron - why the stock might be worth as much as 53% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Textron research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Textron research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Textron's overall financial health at a glance.

No Opportunity In Textron?

Our top stock finds are flying under the radar-for now. Get in early:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com