- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Fastenal (FAST) Valuation Check After Q1 Earnings Beat Revenue Forecasts And Expands Inventory Technology Plans

Fastenal (FAST) just reported first quarter results that matched earnings expectations, while revenue came in slightly ahead, supported by stronger daily sales, new contracts, and growth across manufacturing and non residential construction customers.

See our latest analysis for Fastenal.

Fastenal's latest earnings have landed against a backdrop where the stock is trading at US$44.00, with a 1-day share price return of 1.71% but a 30-day share price return that is down 3.89%. The 5-year total shareholder return of 87.76% points to stronger longer term momentum.

If you are weighing Fastenal's results against other industrial and infrastructure trends, this is a useful moment to broaden your search with 35 power grid technology and infrastructure stocks

With earnings on track, revenue slightly ahead, and the stock at US$44.00 with a small discount to analyst targets, should you see Fastenal as undervalued at this level, or has the market already priced in future growth?

Most Popular Narrative: 5.4% Undervalued

Fastenal's most followed narrative pegs fair value at $46.49, a touch above the last close at $44.00, which puts the current price inside a relatively tight valuation band.

The company is expanding its Fastenal Managed Inventory (FMI) technology which currently represents over 43% of revenue, aiming to enhance revenue growth by increasing efficiency in customer supply chains. Fastenal aims to increase its digital footprint to represent 66-68% of sales, up from 61%, potentially boosting revenue by optimizing purchasing and operational efficiency.

Want to understand why this valuation leans slightly above today's price? The narrative leans heavily on digital adoption, recurring revenue style contracts, and richer margins built into those assumptions.

Result: Fair Value of $46.49 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on execution, because ongoing trade tensions and tariff costs could pressure supply chains, while higher inventory levels may strain cash flow and flexibility.

Find out about the key risks to this Fastenal narrative.

Another View: Rich Multiples Cloud The Undervaluation Story

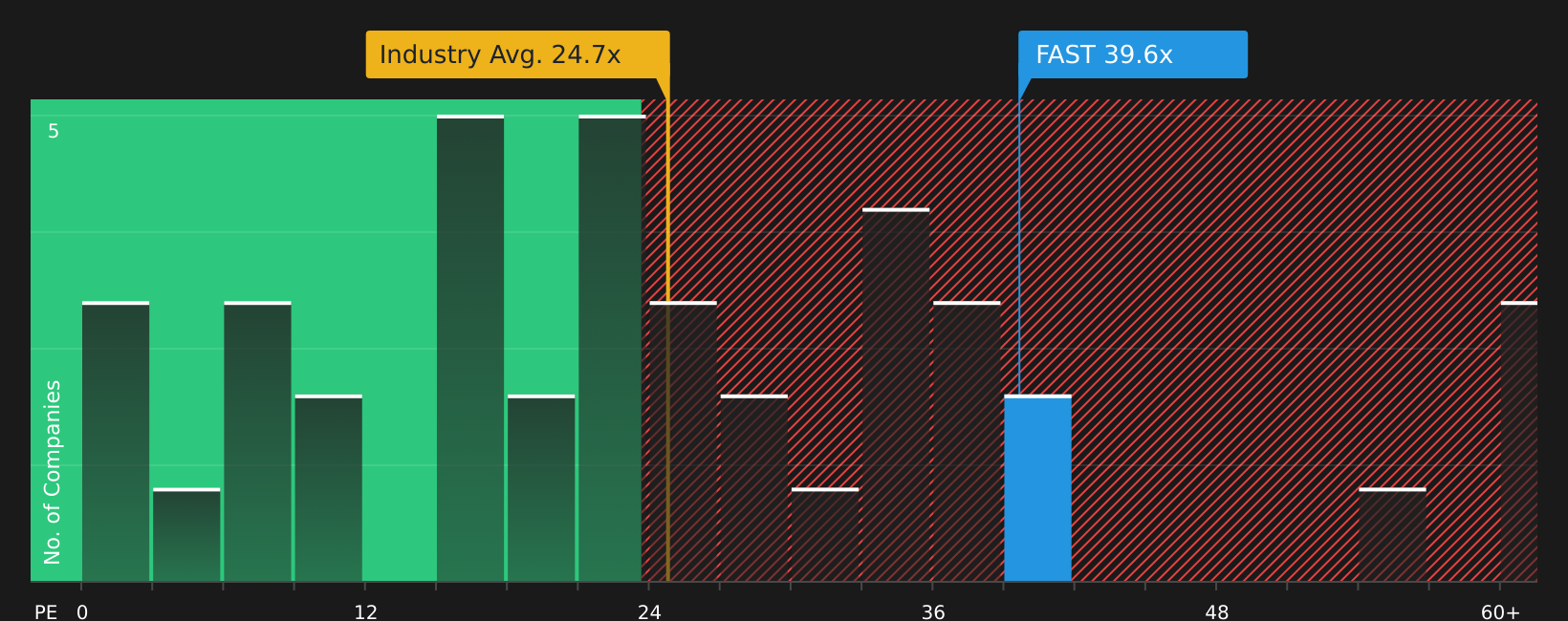

That 5.4% “undervalued” narrative sits awkwardly against Fastenal's current P/E of 38.9x, which is well above the industry at 24x and a fair ratio estimate of 29.6x. In plain terms, the stock already carries a premium, so is the cushion to fair value really that comfortable?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of risks and rewards seems finely balanced, consider your next steps while the details are fresh in your mind and weigh the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Fastenal does not fully fit your plan, do not stop here. Use this moment to broaden your watchlist with focused stock ideas built from clear fundamentals.

- Target higher potential returns with a curated set of underpriced opportunities using the 51 high quality undervalued stocks.

- Prioritise resilience and capital preservation by reviewing companies identified in the 65 resilient stocks with low risk scores.

- Hunt for less crowded opportunities by scanning the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com