- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At SiteOne Landscape Supply (SITE) Valuation After Recent Share Price Weakness

SiteOne Landscape Supply (SITE) has been drawing attention after a stretch of weaker share performance, with the stock down about 21% over the past month and about 25% over the past 3 months.

See our latest analysis for SiteOne Landscape Supply.

With the share price down 20.53% over the past 30 days and 25.29% over 3 months, while the 1 year total shareholder return is only down 6.98%, recent weakness appears more like fading momentum than a sudden shift in the long term picture.

If this kind of volatility has you scanning for other opportunities, it could be a useful moment to widen your search and check out 18 top founder-led companies

So, with the stock under pressure, current revenue of $4,705.5m and net income of $152.5m, plus a value score of 2 and an 11.04% intrinsic discount, is there a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 13% Undervalued

SiteOne's most followed narrative pegs fair value around $131.30, compared with the last close at $114.71, framing the recent pullback in a different light.

SiteOne is the largest wholesale distributor of landscaping supplies in the U.S., serving professional contractors rather than DIY consumers. Its catalog spans irrigation systems, hardscapes, nursery products, lighting, and erosion control, inputs that are essential, not discretionary, for commercial and residential projects alike.

Want to see what justifies that valuation gap? The narrative focuses on earnings expansion, consistent revenue growth, and a profit margin profile that targets higher levels over time.

Result: Fair Value of $131.30 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to factor in risks such as weaker contractor spending if housing activity remains soft, and pressure on margins if input costs or competition increase.

Find out about the key risks to this SiteOne Landscape Supply narrative.

Another View: Valuation Through Earnings

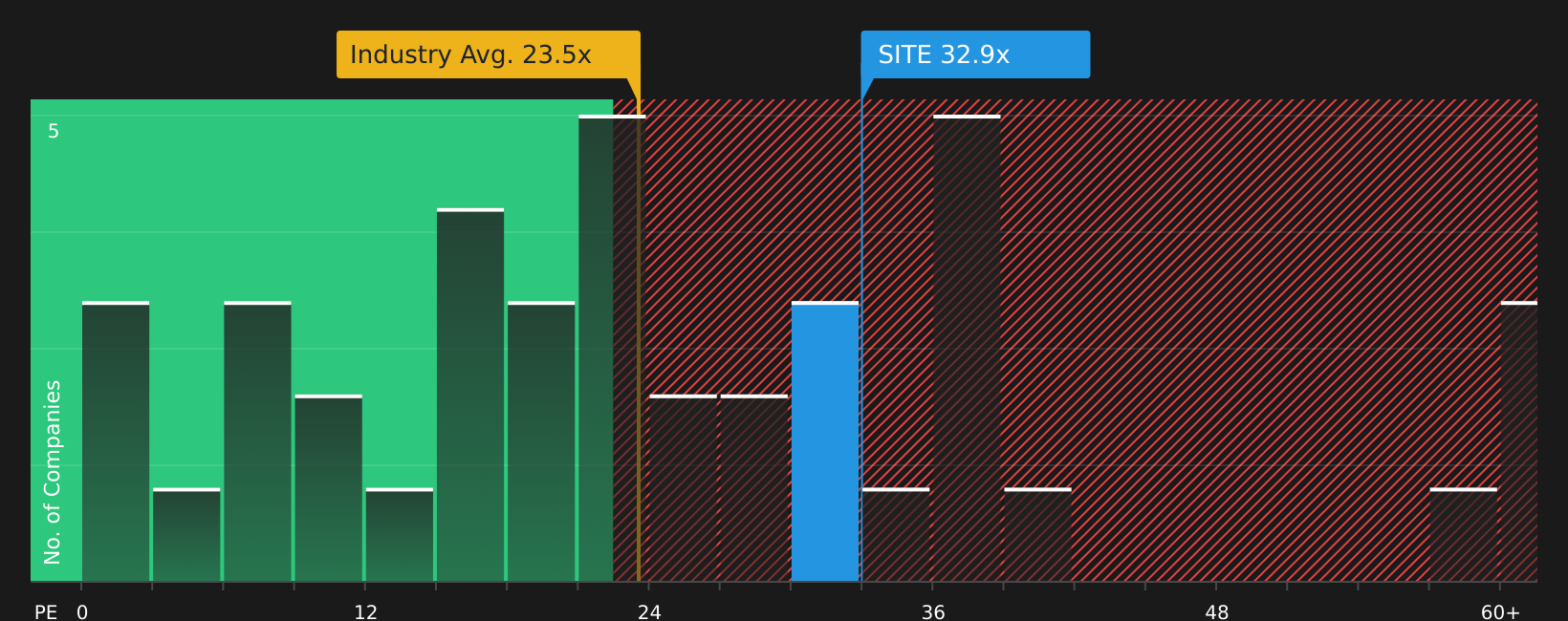

The user narrative leans on fair value of $131.30, but the P/E ratio of 33.3x tells a different story. That is richer than the US Trade Distributors industry at 24x, the peer average at 21.5x, and even the fair ratio of 30.3x. This points to some valuation risk if sentiment cools.

For a closer look at how this earnings multiple compares across peers and against the fair ratio, including where the market could shift if expectations reset, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

After weighing both the pullback and the richer P/E, it helps to move quickly. Review the underlying data and decide where you stand on SiteOne's potential rewards, starting with 4 key rewards.

Looking for more investment ideas?

If SiteOne is on your radar, do not stop there. The wider market is full of stocks that fit different goals, and this is the moment to scan for them.

- Target long term value potential by reviewing companies highlighted in 51 high quality undervalued stocks.

- Strengthen your income focus by checking stocks in the 12 dividend fortresses.

- Hunt for early stage opportunities with solid fundamentals using the 29 elite penny stocks with strong financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com