- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Ingersoll Rand (IR) Using Partnerships To Redefine Its Edge In Oil-Free Air Technology?

- Ingersoll Rand recently announced a multiyear partnership with Garrett Motion to co-develop next-generation oil-free air technologies aimed at improving energy efficiency, reliability, and air purity for critical applications in sectors such as food and beverage and life sciences, with initial products planned for select customers in 2026 and broader rollout in 2027.

- This collaboration highlights how Ingersoll Rand is leaning on external engineering expertise to accelerate innovation in oil-free compression, a niche where stricter purity and sustainability requirements can meaningfully differentiate equipment providers.

- We’ll now examine how this focus on next-generation oil-free, energy-efficient air systems could influence Ingersoll Rand’s broader investment narrative.

AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Ingersoll Rand Investment Narrative Recap

To own Ingersoll Rand, you need to believe in its ability to keep turning niche, mission critical compression technologies into steady growth, despite recent margin pressure, one off charges, and softer share performance. The Garrett Motion partnership reinforces the near term catalyst around higher value, oil free, energy efficient systems, but does not fundamentally change the biggest current risk: that organic orders in core Compressors and Power Tools remain muted, challenging expectations for meaningful growth in coming years.

Among recent developments, ongoing share repurchases stand out alongside this technology partnership. Ingersoll Rand has bought back about 25.9 million shares for roughly US$1.85 billion so far under its plan, even as revenue growth guidance for 2026 sits at 2.5% to 4.5%. For investors, pairing disciplined capital returns with investments in oil free innovation may be central to whether the stock can justify its relatively high earnings multiple over time.

Yet behind the appeal of cleaner, oil free air systems, investors should still be aware of how acquisition missteps or integration issues could...

Read the full narrative on Ingersoll Rand (it's free!)

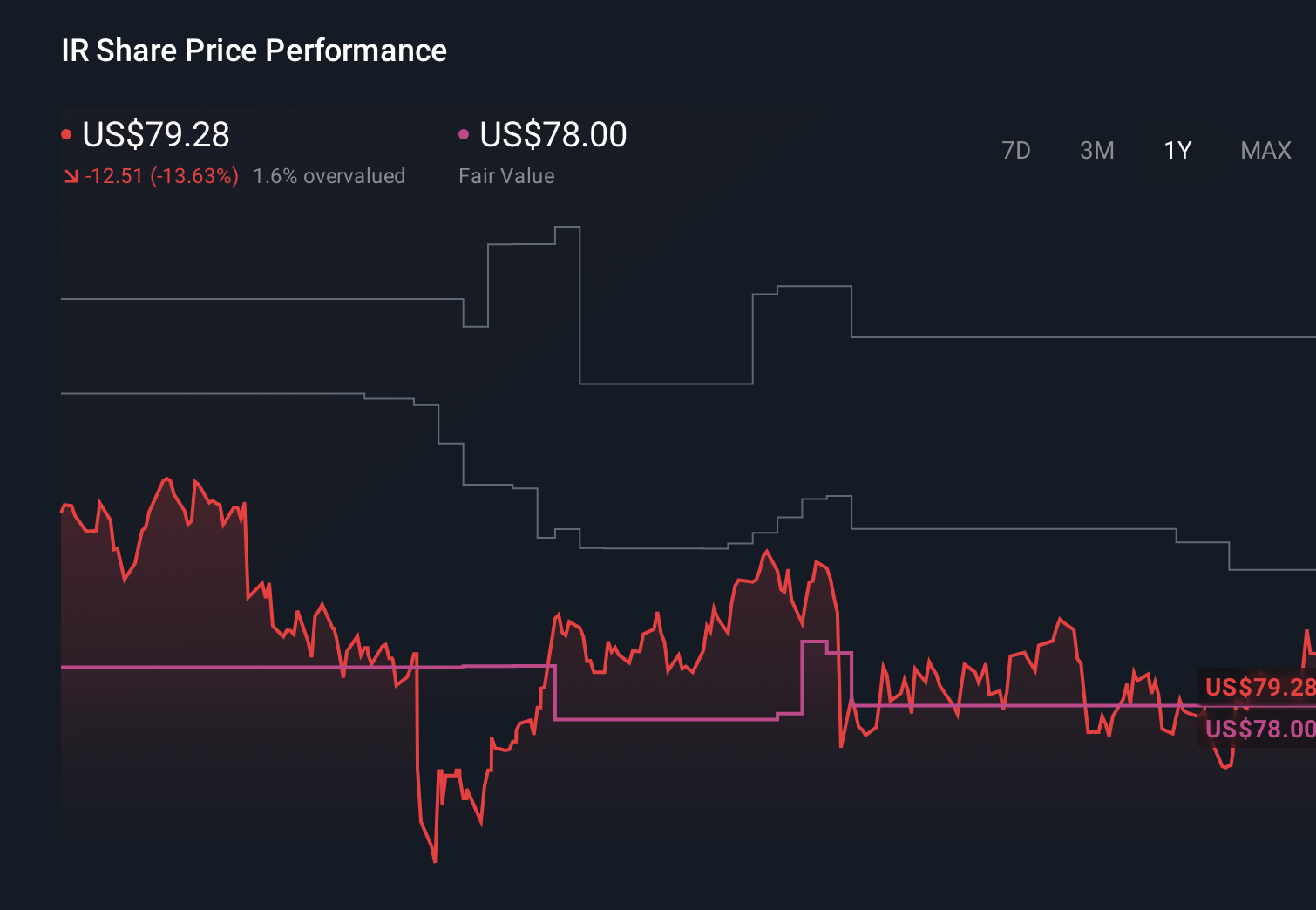

Ingersoll Rand's narrative projects $9.0 billion revenue and $1.4 billion earnings by 2029. This requires 4.9% yearly revenue growth and an earnings increase of about $0.8 billion from $587.0 million.

Uncover how Ingersoll Rand's forecasts yield a $94.00 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue around US$8.8 billion and earnings of US$1.5 billion by 2028, so this oil free push could either reinforce those upbeat expectations or expose how dependent they are on smooth expansion into new markets and acquisitions, reminding you that reasonable views on Ingersoll Rand’s future can differ widely.

Explore 3 other fair value estimates on Ingersoll Rand - why the stock might be worth as much as 34% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ingersoll Rand research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ingersoll Rand research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ingersoll Rand's overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com