- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Higher-for-Longer Rates Might Change The Case For Investing In Customers Bancorp (CUBI)

- In the past week, April CPI data came in at 3.8%, pushing the US 10-year Treasury yield to 4.43% and signaling that interest rates may stay higher for longer, which weighed on regional bank sentiment including Customers Bancorp.

- This macro backdrop highlights the tension for banks between potential benefits from higher asset yields and mounting pressure on funding costs as deposit competition intensifies.

- We’ll now examine how the prospect of higher-for-longer interest rates may influence Customers Bancorp’s technology-led growth and digital-asset-focused narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Customers Bancorp Investment Narrative Recap

To own Customers Bancorp today, you need to believe that its technology-heavy, digital-asset-focused model can turn higher-cost deposits into durable earnings while managing the risks that come with a concentrated cubiX funding base. The latest CPI print and higher 10-year yield pressure the near term catalyst of net interest income expansion by squeezing funding costs, while also sharpening the main risk around deposit stickiness and liquidity. Overall, the April data reinforces existing concerns rather than creating a new, material shock.

Against this backdrop, the recent Q1 2026 results are especially relevant. Customers Bancorp reported net interest income of US$191.35 million and net income of US$69.65 million, alongside lower net charge offs than a year ago. For investors, this print provides an updated read on how the bank is balancing tech investment, digital-asset growth, and funding costs at a time when higher for longer rates could stress cubiX deposits and compress margins if competition intensifies.

Yet while Customers Bancorp’s tech story is appealing, the concentration of digital asset related deposits raises funding and liquidity questions that investors should be aware of...

Read the full narrative on Customers Bancorp (it's free!)

Customers Bancorp's narrative projects $958.3 million revenue and $387.9 million earnings by 2029. This requires 5.9% yearly revenue growth and about a $118.6 million earnings increase from $269.3 million today.

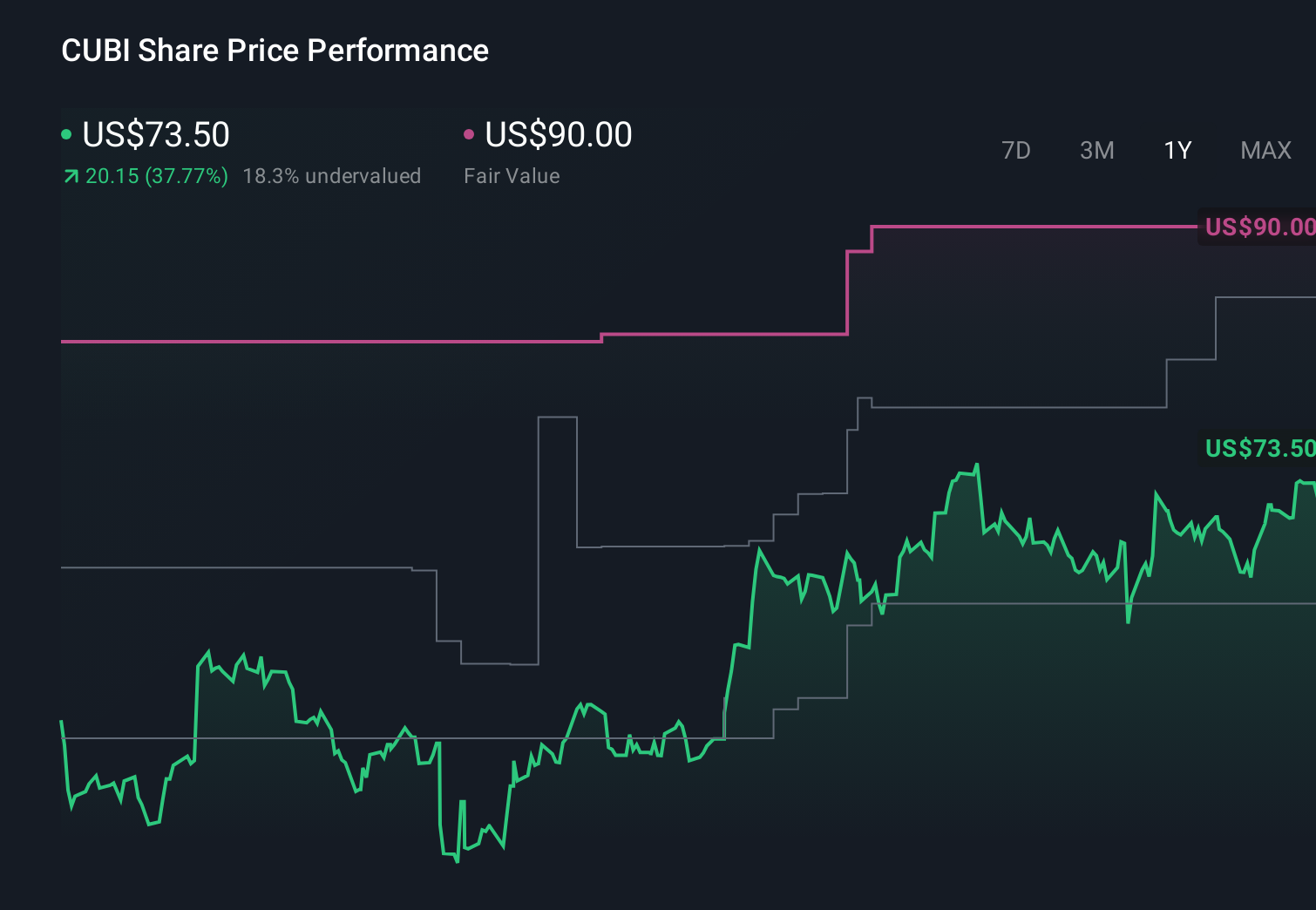

Uncover how Customers Bancorp's forecasts yield a $90.00 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming earnings could reach about US$387.4 million by 2029, yet still worrying that rising fintech competition and regulatory complexity might blunt the benefits of Customers Bancorp’s tech investments, which shows how differently you and other investors might interpret the latest higher for longer rate shock.

Explore 3 other fair value estimates on Customers Bancorp - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Customers Bancorp research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free Customers Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Customers Bancorp's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 17 early-stage AI stocks could fund your retirement.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com