- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

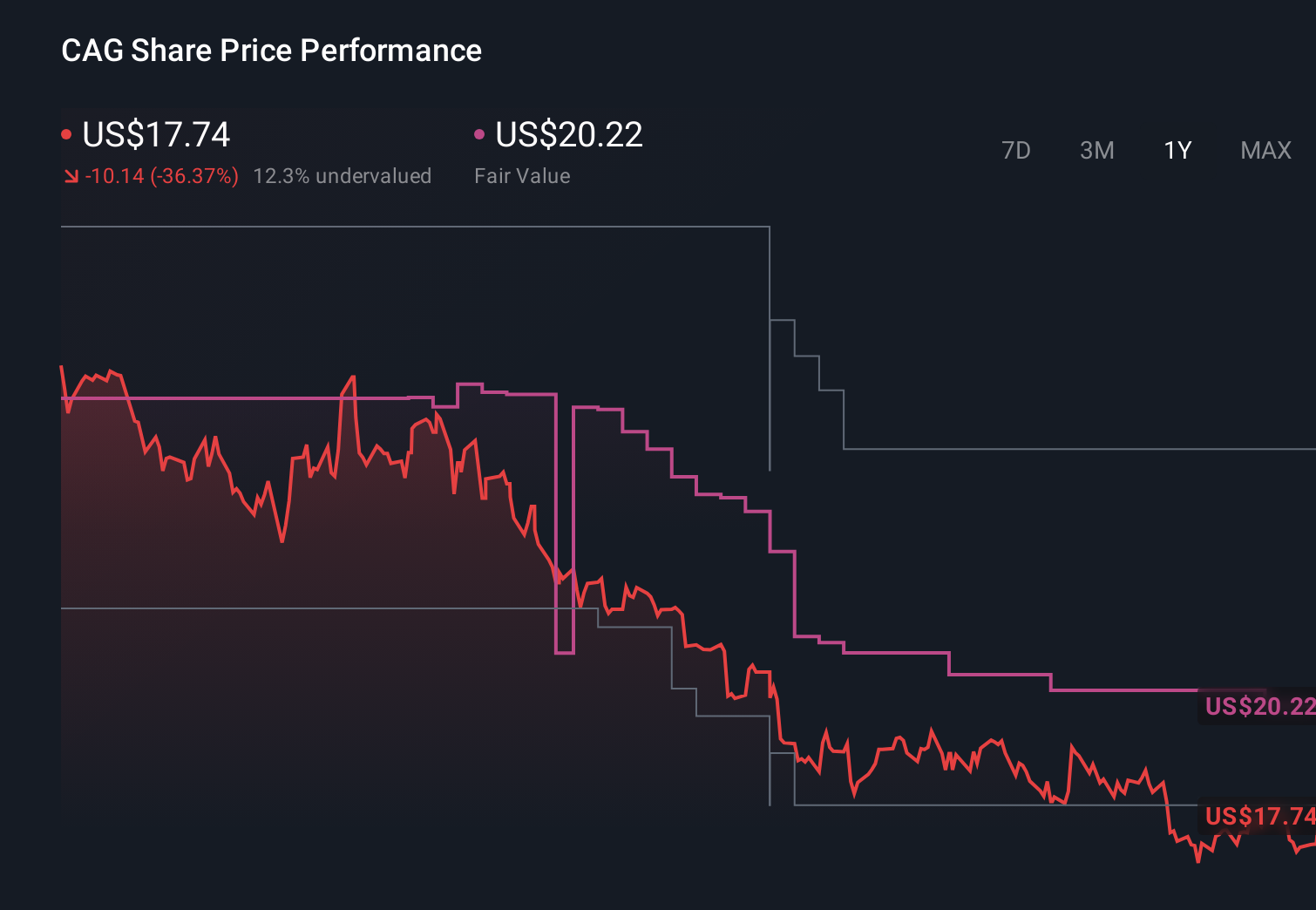

Did Conagra’s New Virtual-Friendly Bylaws Reveal a Deeper Shift in CAG’s Profit Priorities?

- On May 5, 2026, Conagra Brands’ board approved amended and restated bylaws that permit virtual stockholder meetings, modernize shareholder proposal and nomination requirements, and remove outdated provisions.

- This governance update arrives as Conagra contends with persistent margin pressures from elevated input costs and inflation, putting its profitability under strain.

- We’ll now examine how ongoing inflation-driven margin pressure may reshape Conagra’s investment narrative and the assumptions supporting its future earnings profile.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Conagra Brands Investment Narrative Recap

To own Conagra Brands today, you need to believe its packaged food brands can convert steady demand into healthier profits despite ongoing inflation and margin pressure. The bylaw changes around virtual meetings and shareholder procedures do not materially alter the key near term catalyst, which remains Conagra’s ability to control input costs, nor the biggest risk, which is sustained margin compression from elevated cost of goods sold.

The most relevant recent development alongside the bylaw update is management’s outlook for about 7% cost of goods sold inflation in fiscal 2026, which underscores how stubborn input cost pressure remains. That expectation sits uncomfortably against hopes for margin improvement, making any near term earnings recovery heavily dependent on execution in pricing, productivity, and supply chain efficiency.

Yet behind the appeal of a value priced food giant, investors should be aware of the risk that persistent inflation and high costs could...

Read the full narrative on Conagra Brands (it's free!)

Conagra Brands’ narrative projects $11.4 billion revenue and $875.0 million earnings by 2029.

Uncover how Conagra Brands' forecasts yield a $16.01 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were recently modeling earnings of about US$1.4 billion on roughly flat revenue by 2029, which is far more upbeat about Conagra’s margin recovery than consensus, and you should recognize that views on how inflation, debt, and demand shape out from here can differ sharply and may shift again as the latest margin and governance developments sink in.

Explore 10 other fair value estimates on Conagra Brands - why the stock might be worth over 3x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Conagra Brands research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Conagra Brands research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Conagra Brands' overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 17 early-stage AI stocks could fund your retirement.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com