- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Should Chipotle’s Transaction Uptick and Expansion Push Require Action From Chipotle Mexican Grill (CMG) Investors?

- In recent days, Chipotle Mexican Grill has highlighted student ordering trends through its Chipotle U Rewards program, detailed a long-term plan to grow its North American store base from 4,000 to 7,000 locations, and reported Q1 2026 comparable sales growth of 0.5% driven by a 0.6% increase in transactions despite margin pressure.

- At the same time, bullish analyst commentary, inclusion on billionaire investor Dan Loeb’s list of preferred large caps, and a new 6.2% ownership stake disclosed by Capital World Investors have reinforced confidence in Chipotle’s expansion ambitions and its efforts to balance growth with rising labor and food costs.

- Now we’ll examine how renewed transaction growth and confidence in Chipotle’s long-term expansion plans may influence the company’s investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

Chipotle Mexican Grill Investment Narrative Recap

To be comfortable owning Chipotle, you need to believe its brand, digital ecosystem and unit growth can overcome cost inflation and competitive pressure. Right now, the key near term catalyst is a return to healthier transaction growth, while the biggest risk is margin compression from wages, food and tariffs. The latest data showing slightly positive traffic and added institutional interest are directionally helpful, but do not materially change either the main catalyst or the core risk.

The most relevant recent development is management’s reiteration of a plan to grow the North American store base from 4,000 to 7,000 locations. This long term expansion target sits alongside renewed positive traffic and initiatives like Chipotle U Rewards, and it ties directly into the main catalyst: whether Chipotle can keep adding profitable units and transactions without letting higher labor, ingredient and build out costs erode restaurant level returns.

Yet beneath the growth story, investors still need to watch how persistent cost inflation and potential tariffs could pressure margins and returns on new units...

Read the full narrative on Chipotle Mexican Grill (it's free!)

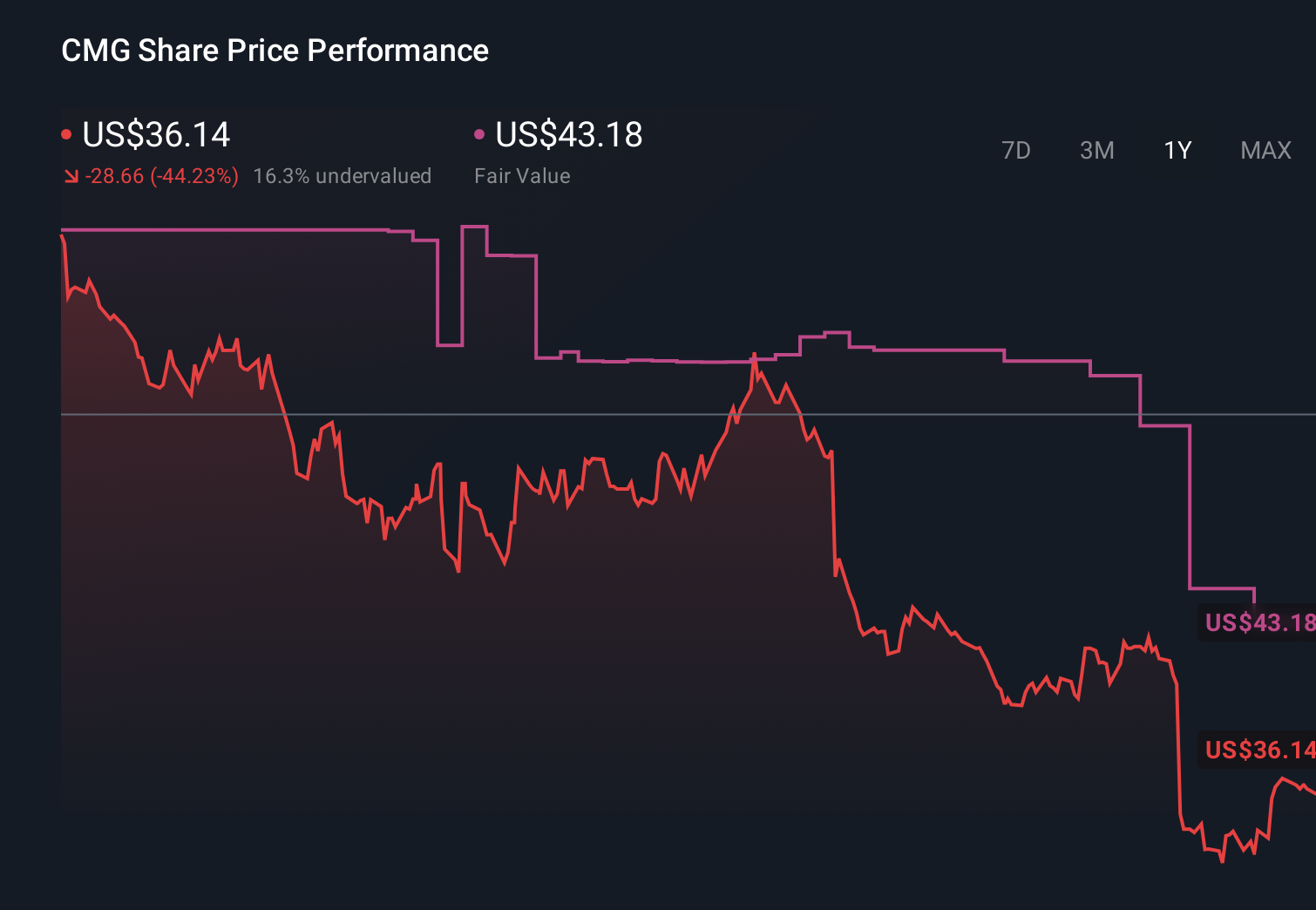

Chipotle Mexican Grill's narrative projects $16.3 billion revenue and $2.0 billion earnings by 2029. This requires 10.2% yearly revenue growth and about a $0.5 billion earnings increase from $1.5 billion today.

Uncover how Chipotle Mexican Grill's forecasts yield a $43.40 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could climb to about US$17.1 billion and earnings to US$2.2 billion, yet the latest news on modest traffic gains and Chipotle U engagement may either support that upbeat view or highlight how much it depends on loyalty driven spend and consistent execution.

Explore 18 other fair value estimates on Chipotle Mexican Grill - why the stock might be worth as much as 62% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Chipotle Mexican Grill research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Chipotle Mexican Grill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Chipotle Mexican Grill's overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com