- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Stanley Black & Decker (SWK) Offering Value After Its Recent 11.8% Share Price Move

- Wondering whether Stanley Black & Decker stock at around US$75 is giving you value or asking too much? Price is only half the story; the real question is what you are getting for it.

- Over the last month the share price has risen 11.8%, yet it is still down 1.7% year to date and up 10.2% over the past year, which can leave the stock looking very different depending on your time frame.

- Recent coverage has focused on how the stock's multi year performance, including a 3 year return of 3.8% and a 5 year decline of 57.5%, contrasts with its more recent 30 day move. This mix of shorter term strength and longer term weakness has put extra attention on whether the current price really reflects what the business is worth.

- On Simply Wall St's 6 point valuation check, Stanley Black & Decker currently scores 4 out of 6, so the rest of this article will walk through what different valuation approaches say about the stock today and then finish with a broader way to think about value beyond just the numbers.

Find out why Stanley Black & Decker's 10.2% return over the last year is lagging behind its peers.

Approach 1: Stanley Black & Decker Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting the company’s future cash flows and discounting them back to today using a required rate of return. It focuses on what cash you might reasonably expect the business to generate in the future, expressed in today’s dollars.

For Stanley Black & Decker, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is about $683.5 million. Analyst estimates and extrapolations then project annual Free Cash Flow rising to $1,773.3 million in 2035, with interim years such as 2026 to 2029 ranging from $719.9 million to $1,168 million. Simply Wall St uses analyst inputs where available and then extends the series using its own assumptions.

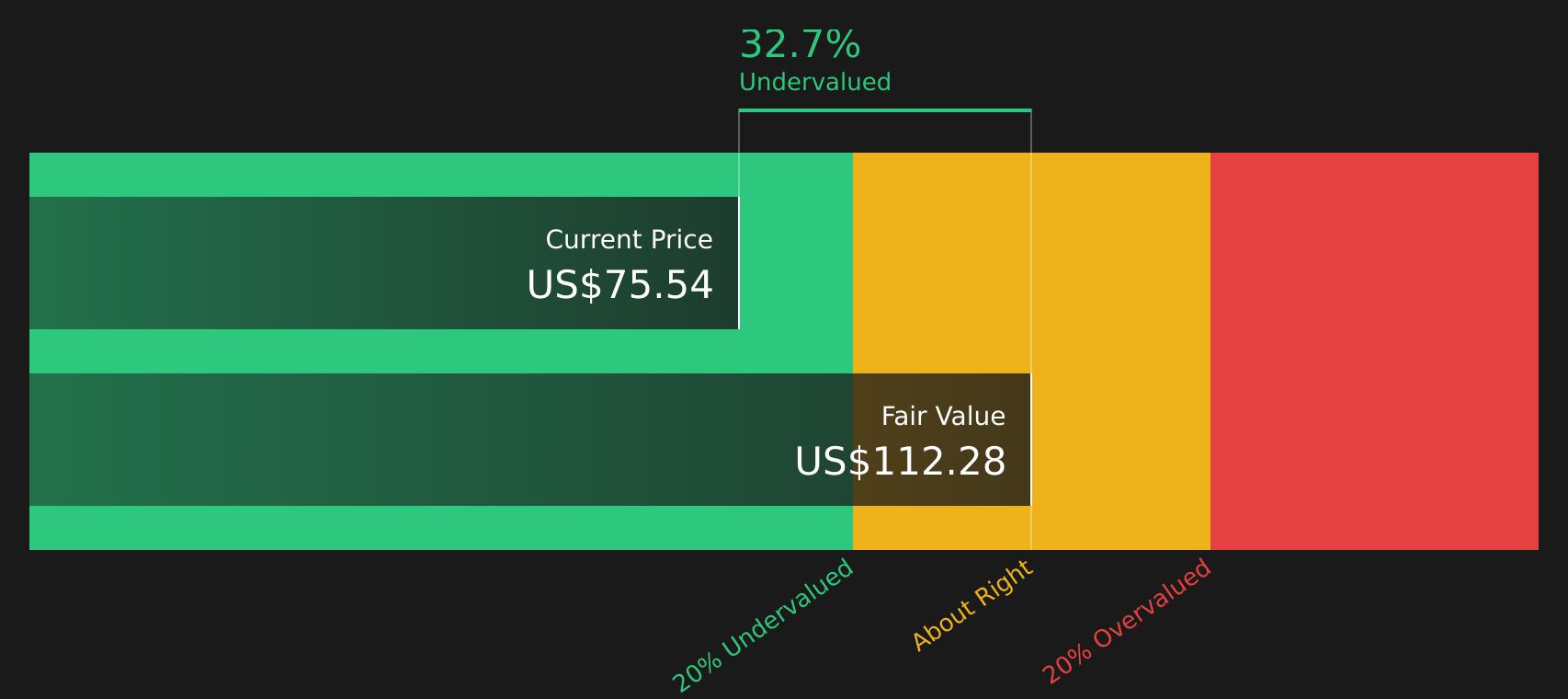

When all these projected cash flows are discounted back, the model arrives at an estimated intrinsic value of $118.10 per share. Compared with a current share price around $75, this implies the stock trades at roughly a 36.4% discount to that DCF estimate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Stanley Black & Decker is undervalued by 36.4%. Track this in your watchlist or portfolio, or discover 50 more high quality undervalued stocks.

Approach 2: Stanley Black & Decker Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about value because it links what you pay for each share to the earnings that support that share. It helps you see how many dollars of price you are paying for each dollar of current earnings.

What counts as a reasonable P/E depends on what investors expect for future growth and how much risk they see. Higher growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually calls for a lower one.

Stanley Black & Decker currently trades on a P/E of 31.48x. That is above the Machinery industry average P/E of 25.91x and also above the peer average of 24.77x. Simply Wall St also calculates a proprietary “Fair Ratio” for the stock of 39.86x, which reflects factors like earnings growth, profit margins, the industry it operates in, company size and specific risks.

This Fair Ratio is more tailored than a simple comparison with peers or the industry because it adjusts for company specific characteristics rather than assuming all stocks should trade on the same multiple. Since the Fair Ratio of 39.86x is higher than the current 31.48x, the P/E based view points to the stock being undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Stanley Black & Decker Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring that to life by letting you attach a clear story about Stanley Black & Decker to specific forecasts for revenue, earnings, margins and a Fair Value, then compare that Fair Value with the current price. All of this is available within an easy tool on Simply Wall St's Community page that updates automatically when new earnings or news arrive. You can see, for example, how one investor might back a more optimistic view with a Fair Value around US$116.82 while another takes a cautious stance closer to US$65.00, and then decide which story best fits your own view before making your next move.

For Stanley Black & Decker however we will make it really easy for you with previews of two leading Stanley Black & Decker Narratives:

Start with the bullish view, which leans into margin recovery, steady revenue growth, and a higher fair value anchored by stronger earnings.

🐂 Stanley Black & Decker Bull Case

Fair Value: US$116.82

Current price vs this Fair Value: around 35.7% below that estimate based on the latest close of US$75.14.

Revenue growth assumption: 2.10% a year.

- This view assumes cost savings and supply chain changes help push net margins toward 7.2% over the next few years, with earnings rising to about US$1.2b and US$7.38 per share by around April 2029.

- It also leans on steady growth in tool demand, particularly from DEWALT, plus connected and battery powered products, to support higher earnings and a future P/E of 20.8x on those 2029 earnings.

- In this scenario US$116.82 is framed as a fair value that sits near the bullish end of analyst targets, while still asking you to test the revenue, margin, and discount rate assumptions against your own view of the business.

Now set that against a more cautious story, which assumes flatter sales, softer valuation multiples, and a fair value that sits below where the stock is currently trading.

🐻 Stanley Black & Decker Bear Case

Fair Value: US$65.00

Current price vs this Fair Value: around 15.6% above that estimate based on the latest close of US$75.14.

Revenue growth assumption: 0.05% a year.

- This narrative works off the idea that revenue stays broadly flat and margins only reach about 7.0%, leading to earnings of roughly US$1.1b and US$6.82 per share by around April 2029.

- It assumes the stock would need to trade on a lower future P/E of 12.5x, reflecting pressure from aging demographics, smart home adoption, higher input costs, and tougher competition.

- On these assumptions the fair value arrives at US$65.00, which sits toward the lower end of analyst targets, and asks you to judge whether muted growth and a reduced multiple better match your expectations for the business.

Both narratives use the same company and many of the same data points, but they put different weights on growth, margins, and the right P/E. The most useful step now is to decide which story feels closer to your own view of Stanley Black & Decker and then stress test the key assumptions rather than focusing only on the current share price.

Do you think there's more to the story for Stanley Black & Decker? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com