- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Why COMPASS Pathways (CMPS) Is Up 13.1% After FDA Fast-Track Moves For COMP360 Profit Shift

- In the first quarter of 2026, COMPASS Pathways reported net income of US$91.2 million, or US$0.71 per share, and announced U.S. FDA acceptance of a rolling New Drug Application and a National Priority Review Voucher for its COMP360 psilocybin therapy in treatment-resistant depression.

- This combination of an accounting-driven swing to profitability and accelerated regulatory review for COMP360 marks a key moment for COMPASS Pathways’ shift from pure R&D focus toward potential commercial readiness.

- We’ll now examine how the rolling NDA process and Priority Review Voucher for COMP360 could reshape COMPASS Pathways’ investment narrative.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

COMPASS Pathways Investment Narrative Recap

To own COMPASS Pathways, you need to believe COMP360 can progress from a late‑stage asset to an approved, used treatment for severe mental health conditions, without exhausting the balance sheet first. The rolling NDA and National Priority Review Voucher sharpen the near term focus on U.S. approval timing as the key catalyst, while the biggest current risk is still that any regulatory, clinical or launch delay could increase funding needs and prolong the path to sustainable, operating‑driven profitability.

The most relevant new development here is the FDA’s acceptance of a rolling NDA and award of a Commissioner’s National Priority Review Voucher for COMP360 in treatment resistant depression. Together, they could shorten the U.S. review clock once the NDA is complete and align more closely with COMPASS’s early commercial buildout, amplifying both the upside of a smoother launch and the execution risk if physician uptake, reimbursement or operational readiness lag behind the accelerated regulatory timetable.

Yet while regulatory momentum looks encouraging, investors should be aware that any shift in trial outcomes, label terms or payer behavior could still...

Read the full narrative on COMPASS Pathways (it's free!)

COMPASS Pathways' narrative projects $193.1 million revenue and $24.2 million earnings by 2029. This requires revenue to grow from zero to $193.1 million and a $261.5 million earnings increase from -$237.3 million today.

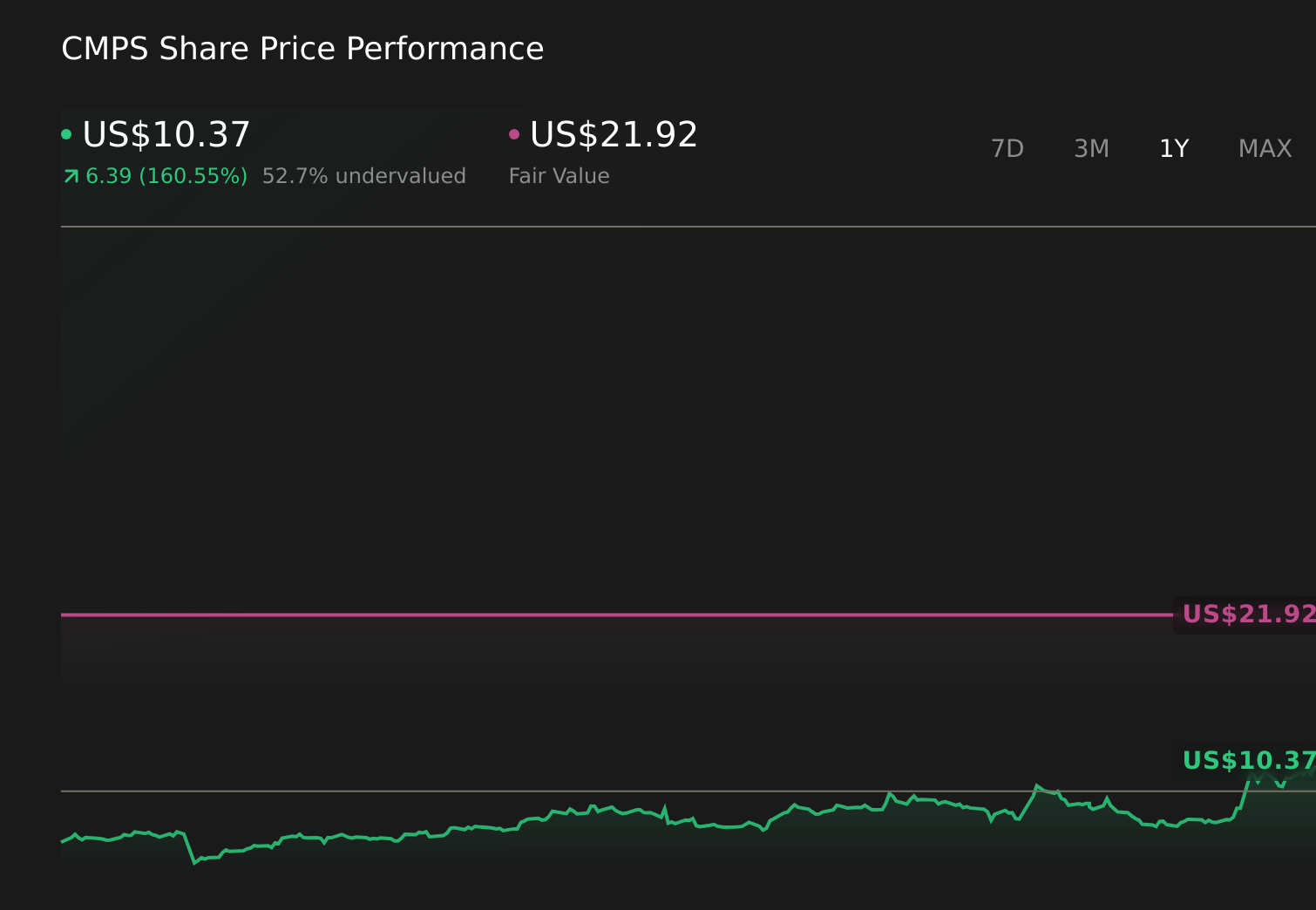

Uncover how COMPASS Pathways' forecasts yield a $21.92 fair value, a 106% upside to its current price.

Exploring Other Perspectives

Before this news, the most bearish analysts saw revenue only reaching about US$59.5 million by 2029 and still questioned profitability, so compared with consensus their view of COMP360’s launch and adoption risks is far more cautious, and it is worth understanding how that more pessimistic scenario could interact with today’s faster review path.

Explore 5 other fair value estimates on COMPASS Pathways - why the stock might be worth 18% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your COMPASS Pathways research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free COMPASS Pathways research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate COMPASS Pathways' overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com