- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Delek Logistics Partners (DKL) Valuation After Its Recent Debt Tender And New Bond Offering

Delek Logistics Partners (DKL) is in focus after bondholders tendered approximately 67.7% of its 7.125% Senior Notes due 2028, alongside an $800 million offering of new 2034 notes intended to reshape the company’s debt profile.

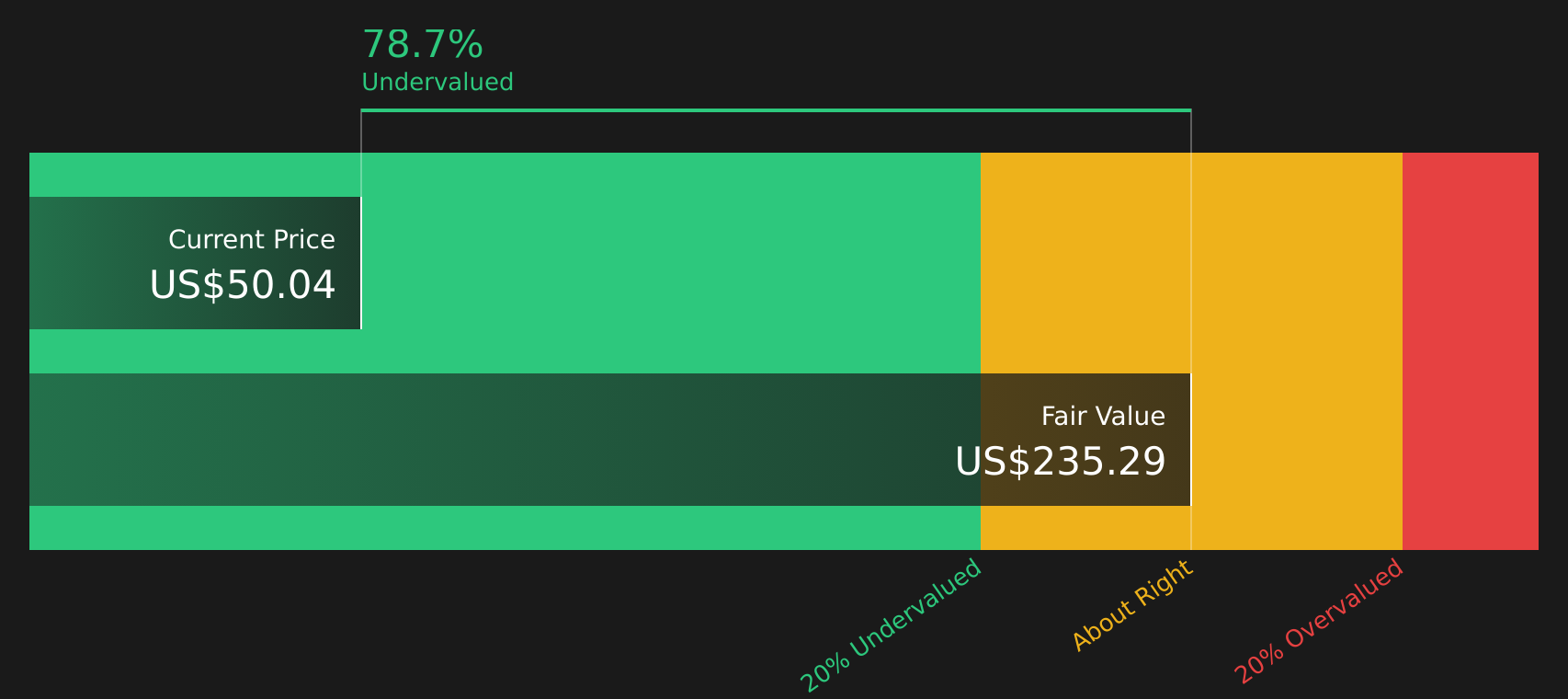

See our latest analysis for Delek Logistics Partners.

The tender offer and new 2034 notes come after a period where the stock has shown mixed momentum, with a 30 day share price return of 4.04% but a 90 day share price decline of 4.49%. At the same time, the 1 year total shareholder return of 38.37% points to stronger longer term gains.

If this type of balance sheet reshaping has you thinking about where else capital could work hard, it may be worth scanning 37 power grid technology and infrastructure stocks

With revenue of US$1,060.86 million, net income of US$169.78 million, an intrinsic discount near 78% and only a small 0.8% gap to the analyst target, is there real upside left here, or is the market already pricing in future growth?

Most Popular Narrative: 1% Undervalued

With Delek Logistics Partners last closing at $51.00 against a narrative fair value of $51.40, the current set up hinges on how future projects and cash flows play out under a 7.28% discount rate.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs, likely boosting gathering and processing volumes, EBITDA, and revenue growth.

Curious what kind of revenue path and margin uplift would need to come from Libby 2 and the broader Permian system for this valuation to stack up. The narrative leans on measured top line growth, thicker margins, and a future earnings multiple that is slightly richer than today. Want to see how those moving parts combine to arrive at a fair value that sits just above the current price.

Result: Fair Value of $51.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the picture could change if energy transition trends soften long term fossil fuel demand, or if high leverage and interest costs squeeze future earnings and flexibility.

Find out about the key risks to this Delek Logistics Partners narrative.

Another Angle On Valuation

The first take uses a cash flow view that points to an intrinsic value far above the current $51.00 price, with DKL trading at an estimated 78.4% discount to future cash flow value. That is a big gap. The key question is whether the assumptions behind those cash flows feel realistic to you.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With the mix of potential rewards and flagged risks in mind, this may be a good moment to review the numbers yourself and stress test your thesis against 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your style even better, so use the Simply Wall Street Screener to widen your watchlist.

- Target steady compounding potential by reviewing companies in the 14 dividend fortresses that aim to pair income with resilience.

- Hunt for mispriced opportunities using the 46 high quality undervalued stocks that filters for quality businesses trading below fair value estimates.

- Prioritise sleep at night holdings through the 68 resilient stocks with low risk scores designed to surface stocks with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com