- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Stronger Margins And Completed Buyback Could Be A Game Changer For ATI (ATI)

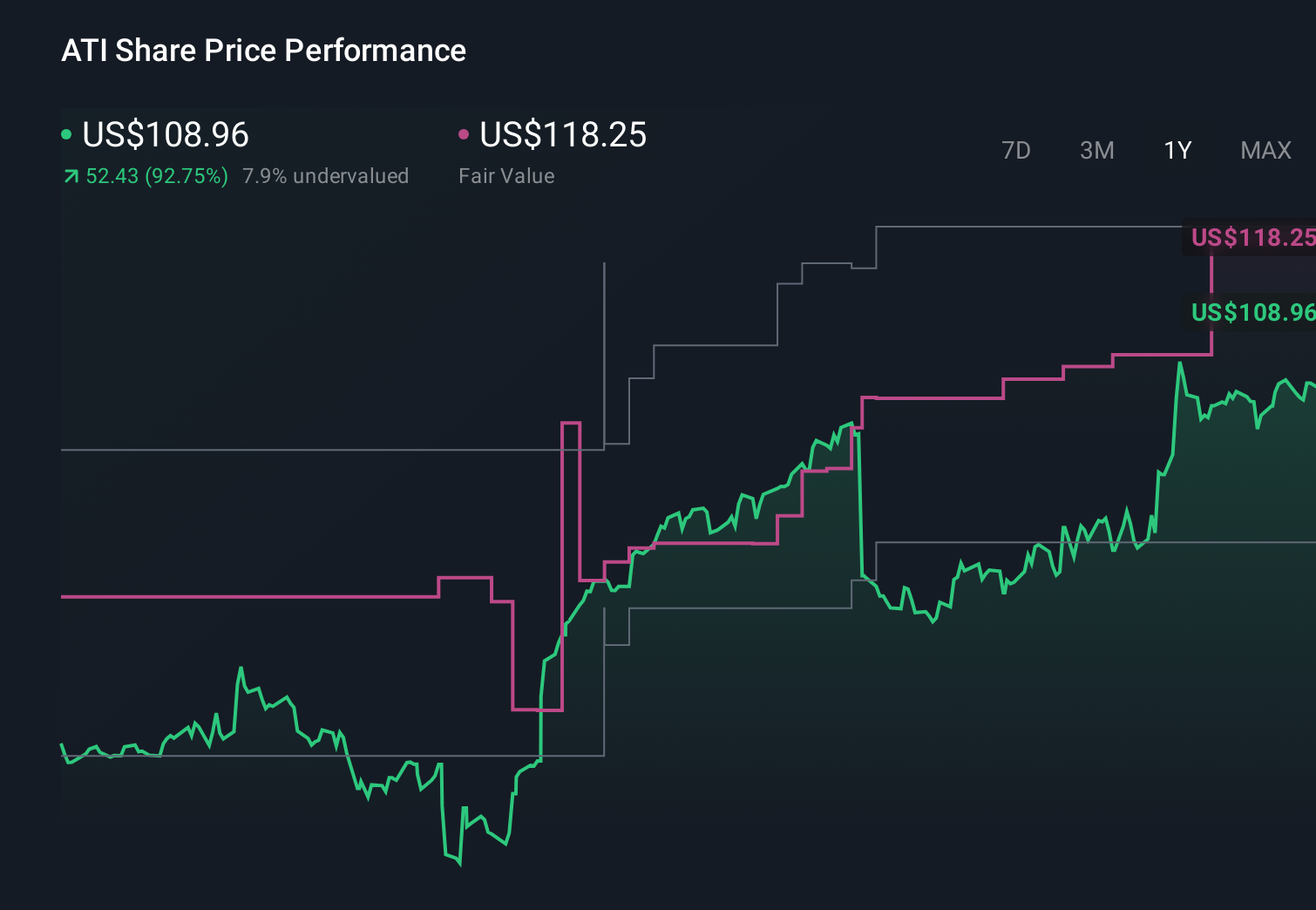

- ATI Inc. recently reported past first-quarter 2026 results showing modest sales growth to US$1,151.5 million and higher net income of US$118.2 million, while also completing a US$655.12 million share repurchase program covering 8,819,175 shares since its September 2024 authorization.

- Together, stronger earnings per share alongside a completed multi-year buyback highlight ATI’s focus on boosting profitability and returning capital to shareholders.

- With Q1 margin improvement now clear, we’ll examine how this earnings strength reshapes ATI’s investment narrative and future expectations.

Find 49 companies with promising cash flow potential yet trading below their fair value.

ATI Investment Narrative Recap

To own ATI, you need to believe its focus on high value aerospace and defense alloys can offset softer industrial markets and a concentrated customer base. The latest Q1 2026 results and completed US$655.12 million buyback support that thesis near term, with margin gains and higher EPS as the key catalyst. The biggest risk remains ATI’s dependence on a handful of major aerospace OEMs, and this update does not materially change that exposure.

The most relevant announcement here is ATI’s Q1 2026 earnings: sales were essentially flat at US$1,151.5 million year on year, but net income rose to US$118.2 million and diluted EPS increased to US$0.85. Management highlighted that richer product mix and stronger aerospace and defense demand helped margins. For investors focused on near term catalysts, this margin expansion matters more than top line growth, especially given concerns about weaker industrial and medical markets.

But while margins are improving today, investors should be aware that ATI’s reliance on a concentrated set of aerospace customers could...

Read the full narrative on ATI (it's free!)

ATI's narrative projects $5.9 billion revenue and $862.2 million earnings by 2029. This requires 8.8% yearly revenue growth and a roughly $436.7 million earnings increase from $425.5 million today.

Uncover how ATI's forecasts yield a $178.67 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were far more cautious, assuming ATI’s revenue would grow to about US$5.1 billion and earnings to around US$612.9 million by 2028, which paints a much less generous outcome than the stronger margin and buyback story you see in the latest quarter, so it is worth asking whether this new information will pull expectations closer to their view or push them further apart.

Explore 6 other fair value estimates on ATI - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your ATI research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free ATI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATI's overall financial health at a glance.

No Opportunity In ATI?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com