- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

It's Been 5 Years Since Tilray Merged With Aphria to Create a "Global Cannabis Leader." Here's How It's Done Since Then

Key Points

Tilray and Aphria merged just over five years ago, in what was a massive merger in the marijuana industry.

While the combined business has grown in size, it hasn't exactly been a growth machine.

In May 2021, Tilray Brands (NASDAQ: TLRY), which was then known as just Tilray, merged with low-cost cannabis producer Aphria, in what was a massive deal in the marijuana industry. The press release announcing the deal said the combined businesses would create "a global cannabis leader." The expectation was that the entity would be able to grow into new markets and be profitable.

Today, Tilray Brands is one of the leading cannabis companies in the world, but it's been a volatile five years since this merger was completed. Let's take a look at how the business has performed since then, how the stock has done, and whether it's a good investment to consider for growth investors today.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Tilray has grown via diversification, but sustained profitability remains elusive

Tilray has expanded over the years by entering new international markets and also by acquiring beverage companies. With the marijuana market in the U.S. remaining off-limits and significant challenges in the Canadian market, Tilray has needed to pursue other opportunities. Acquiring craft brewers has been one that it has taken advantage of. Today, beverages account for roughly one-quarter of its business.

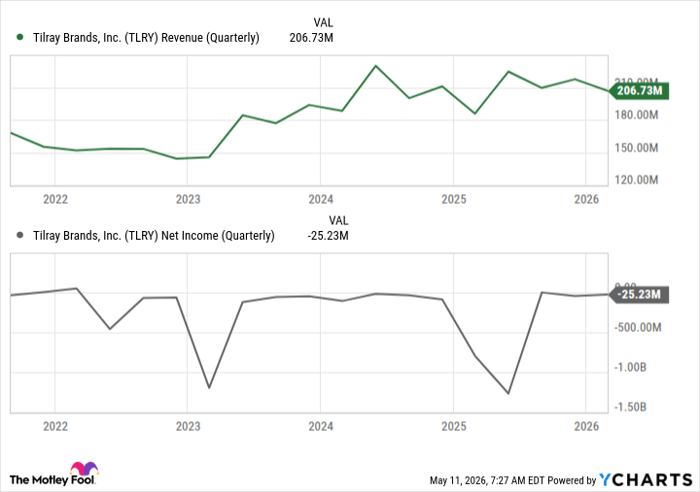

TLRY Revenue (Quarterly) data by YCharts

Tilray's revenue has been choppy, and although it has risen considerably over the years, it may have fallen short of the type of growth that investors may have expected from the business. Potentially more troubling is the lack of profitability and continued challenges in staying out of the red. Its bottom line has fluctuated, and at this stage, it's difficult to make the case that it has a path to the sustained profitability it was aiming for with its merger five years ago.

With limited growth and a poor bottom line, it's little surprise that the stock hasn't performed well; shares of Tilray are down more than 96% in the past five years.

Investors shouldn't expect a turnaround anytime soon

Tilray hasn't been a good buy for a long time. This year, its shares are down 38% as it continually struggles to attract investors. There isn't a big growth catalyst waiting in the wings to help the business turn things around. While its valuation has declined significantly, that alone isn't necessarily a reason to buy the stock, given the risk that it contains.

This is a highly risky stock to invest in, and while speculators may be able to generate gains due to its volatility and during brief periods of bullishness and excitement (such as when there's hope of marijuana reform in the U.S.), Tilray has unfortunately not given investors much of a reason to trust the stock as a long-term investment.

David Jagielski, CPA has no position in any of the stocks mentioned. The Motley Fool recommends Tilray Brands. The Motley Fool has a disclosure policy.