- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Exploring 3 Undiscovered Gems in the US Market

The United States market has experienced a notable upswing, climbing 2.2% in the past week and 31% over the last year, with earnings projected to grow by 17% annually. In this dynamic environment, identifying stocks that combine strong fundamentals with growth potential can uncover hidden opportunities for investors seeking to capitalize on emerging trends.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.27% | 1.25% | -3.09% | ★★★★★★ |

| Southern Michigan Bancorp | 108.80% | 7.38% | 0.84% | ★★★★★★ |

| Sound Financial Bancorp | 16.13% | 0.44% | -12.60% | ★★★★★★ |

| Oakworth Capital | 51.38% | 15.89% | 14.04% | ★★★★★★ |

| SIFCO Industries | 12.27% | -4.21% | -2.87% | ★★★★★★ |

| Anbio Biotechnology | NA | -30.09% | -3.45% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| Winchester Bancorp | 123.28% | 9.14% | -54.82% | ★★★★★★ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

Amtech Systems (ASYS)

Simply Wall St Value Rating: ★★★★★★

Overview: Amtech Systems, Inc. manufactures and sells capital equipment and related consumables for semiconductor device fabrication and packaging globally, with a market cap of $311.59 million.

Operations: Amtech Systems generates revenue primarily from the sale of capital equipment and consumables used in semiconductor device fabrication and packaging. The company's financial performance is influenced by its net profit margin, which has shown variability over recent periods.

Amtech Systems, a player in the semiconductor industry, has recently turned profitable with net income hitting US$1.17 million for Q2 2026, compared to a loss of US$31.81 million the previous year. The company is seeing robust growth driven by AI-related products, with recurring revenue streams now making up 40% of total sales. Despite its success, Amtech's reliance on mature semiconductor markets and modest R&D spending could pose challenges as it navigates potential downturns in AI capital expenditures. Analysts have set a price target of US$16 per share, reflecting cautious optimism about future earnings potential amidst these hurdles.

Interface (TILE)

Simply Wall St Value Rating: ★★★★★★

Overview: Interface, Inc. is a company that designs, produces, and sells modular carpet products across various regions including the United States, Canada, Latin America, Europe, Africa, Asia, and Australia with a market capitalization of approximately $1.73 billion.

Operations: Interface generates revenue primarily from two segments: Americas (AMS) contributing $859.69 million and Europe, Africa, Asia, and Australia (EAAA) with $560.87 million.

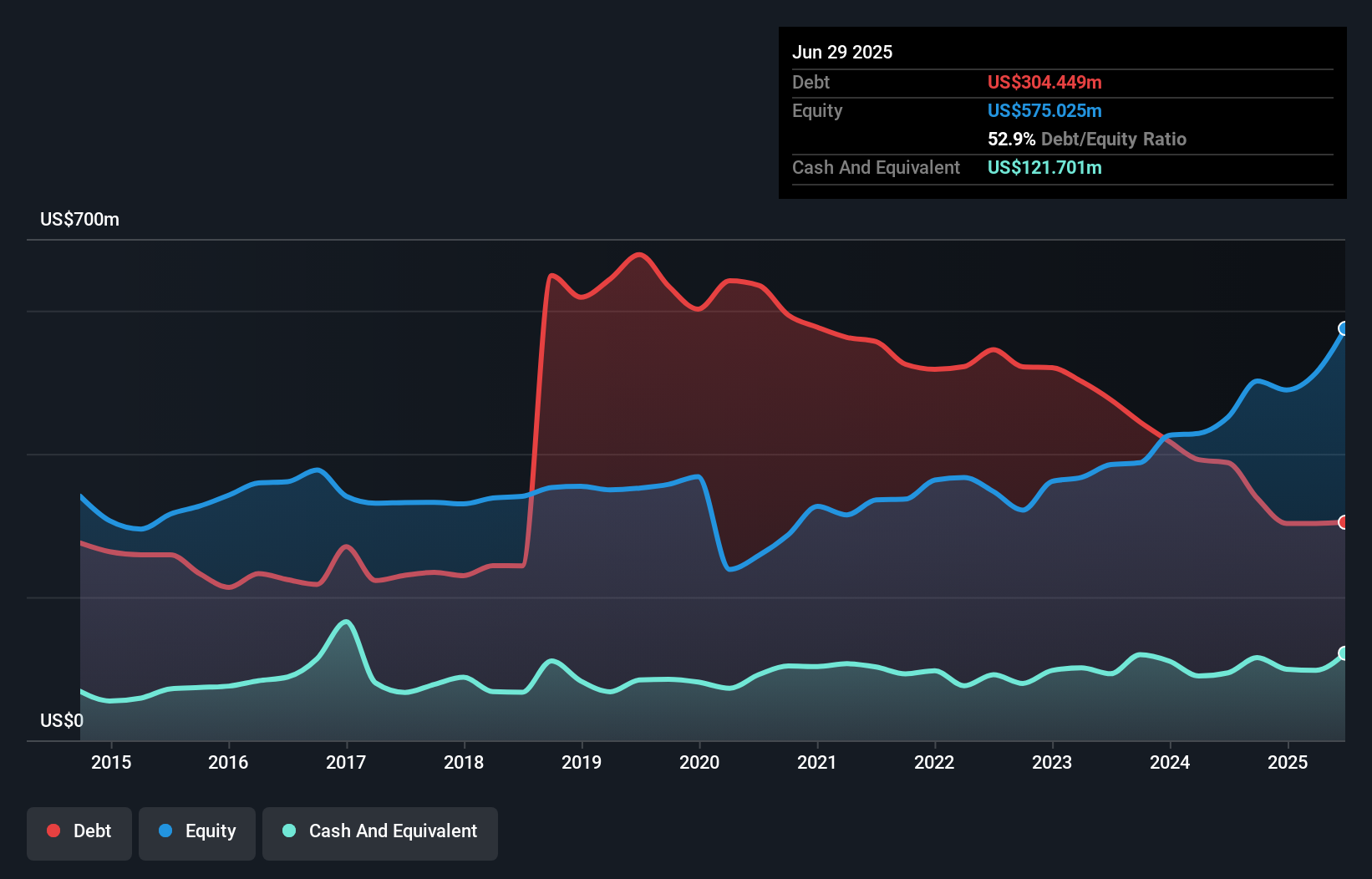

Interface is catching attention with its focus on sustainable flooring solutions, notably expanding its rubber portfolio with noravant™, a PVC-free resilient option. The company has shown impressive financial health, reducing its debt to equity ratio from 178.5% to 31% over five years and maintaining a satisfactory net debt to equity ratio of 21.3%. Earnings grew by 46.3% last year, outpacing the industry average of 7.1%. Recent share repurchases totaling $35.35 million reflect confidence in future growth prospects, while raised earnings guidance for fiscal year 2026 underscores optimism about upcoming performance in the commercial services sector.

Koppers Holdings (KOP)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Koppers Holdings Inc. is a company that offers treated wood products, wood preservation chemicals, and carbon compounds across the United States, Australasia, Europe, and other international markets with a market capitalization of $846 million.

Operations: Koppers Holdings generates revenue primarily from treated wood products, wood preservation chemicals, and carbon compounds. The company's net profit margin exhibits fluctuations, influenced by market conditions and operational costs across its diverse geographical markets.

Koppers Holdings, a nimble player in the chemicals sector, has showcased impressive earnings growth of 202% over the past year, outpacing industry averages. Despite a hefty net debt to equity ratio of 159.9%, their interest payments are well-covered by EBIT at three times coverage. The recent quarter saw a shift from a net loss to an income of US$7.1 million, with basic earnings per share improving from a loss of US$0.68 to US$0.36. While high debt levels and market challenges persist, strategic transformations and sustainability initiatives suggest potential for enhanced profit margins and long-term growth prospects.

Key Takeaways

- Explore the 340 names from our US Undiscovered Gems With Strong Fundamentals screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com