- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Why Ternium (TX) Is Up 5.2% After Margin-Rich Q1 2026 Results And Heavy Latin America Bets

- Ternium S.A. reported past first-quarter 2026 results with revenue of US$3,934 million, essentially flat year over year, while net income attributable to shareholders rose to US$213 million and Adjusted EBITDA increased to US$479 million, reflecting higher steel prices and better margins.

- Behind these stronger profits, Ternium poured US$406 million into expanding its Pesquería industrial center in Mexico and spent US$315 million to lift its Usiminas stake, moves that weighed on free cash flow but further embedded the company in key Latin American steel markets.

- We’ll now examine how this margin-rich quarter, underpinned by higher steel prices and efficiency gains, reshapes Ternium’s previously balanced investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Ternium Investment Narrative Recap

To stay invested in Ternium, you need to believe its heavy buildout in Mexico and deeper foothold in Brazil can justify today’s capital intensity and Latin American concentration. The latest quarter’s stronger margins help the near term case, but negative free cash flow and a thinner net cash cushion keep execution risk around the US$4 billion capex cycle and regional import pressure front and center. On balance, the news reinforces rather than changes the key near term catalyst and risk.

The clearest recent signal is the board’s April decision to cut the proposed 2025 dividend to US$2.20 per ADS, shortly before reporting a quarter of higher profitability but cash outflows tied to US$406 million in Pesquería spending and US$315 million for more Usiminas shares. For investors, that pairing of stronger earnings with a lower payout highlights how much management is prioritizing balance sheet resilience while the big Mexico projects move from spending phase toward payoff.

Yet even with healthier margins today, investors should be aware that heightened capex demands and trade driven price pressure could still...

Read the full narrative on Ternium (it's free!)

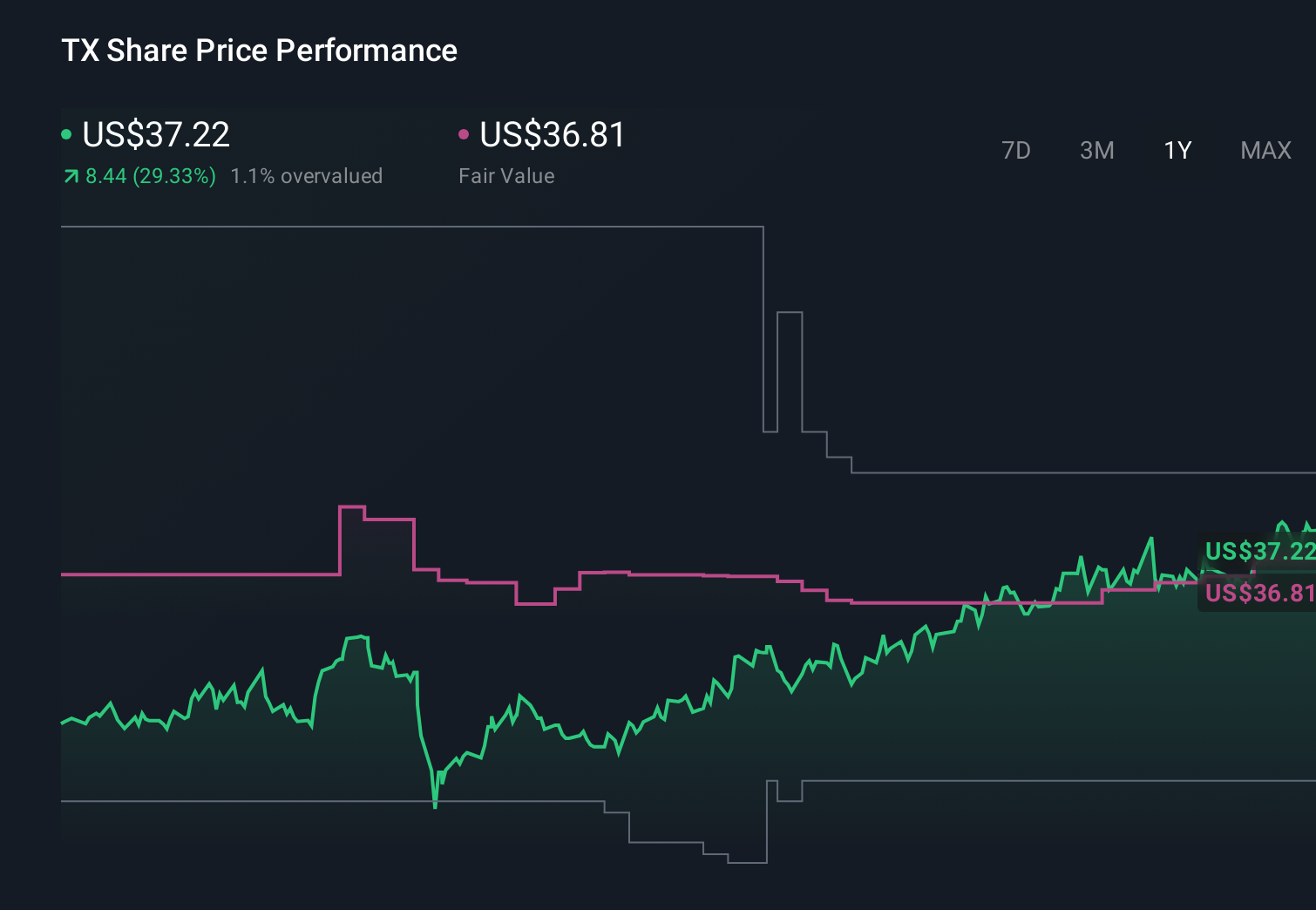

Ternium's narrative projects $18.1 billion revenue and $1.0 billion earnings by 2029.

Uncover how Ternium's forecasts yield a $43.46 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Relative to this, the lowest analysts were far more cautious, assuming revenues of about US$17.4 billion and only modest margin gains by 2029, whereas the latest profit jump and heavier capex around Pesquería could eventually push some of those pessimistic views to reassess or, if execution falters, look prescient.

Explore 4 other fair value estimates on Ternium - why the stock might be worth as much as 74% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Ternium research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ternium research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ternium's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com