- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Federated Hermes’ (FHI) Dividend Hike and ESOP Shelf Quietly Reframing Its Capital Allocation Playbook?

- In late April 2026, Federated Hermes reported first-quarter revenue of US$478.96 million and net income of US$96.38 million, alongside a quarterly dividend increase to US$0.38 per share payable on May 15, following its Annual General Meeting.

- Just days later, the company filed a US$270.60 million shelf registration for 5,000,000 Class B common shares linked to its employee stock ownership plan, underscoring an emphasis on employee alignment and capital-raising flexibility.

- We’ll now examine how Federated Hermes’ higher dividend and ESOP-related shelf registration filing could influence its existing investment narrative.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Federated Hermes Investment Narrative Recap

To own Federated Hermes, you need to be comfortable with a mid sized active manager that leans heavily on money market funds and aims to grow across cash, fixed income and ESG focused strategies. The latest dividend increase and ESOP related shelf registration do not materially change the near term picture, where the key catalyst remains demand for money market and cash management products, while the biggest risk is continued fee pressure and competition from lower cost passive products.

The first quarter 2026 earnings release is most relevant here, as it shows revenue of US$478.96 million and net income of US$96.38 million. Against a backdrop of fee compression risk, these results help frame whether Federated Hermes can keep funding dividend increases and broader growth initiatives from its underlying cash generation, rather than relying too heavily on capital markets transactions such as the new US$270.60 million ESOP related shelf registration.

But investors should also be aware that growing reliance on money market funds exposes the business to shifts in regulation and interest rate conditions, which could...

Read the full narrative on Federated Hermes (it's free!)

Federated Hermes' narrative projects $2.0 billion revenue and $422.2 million earnings by 2029.

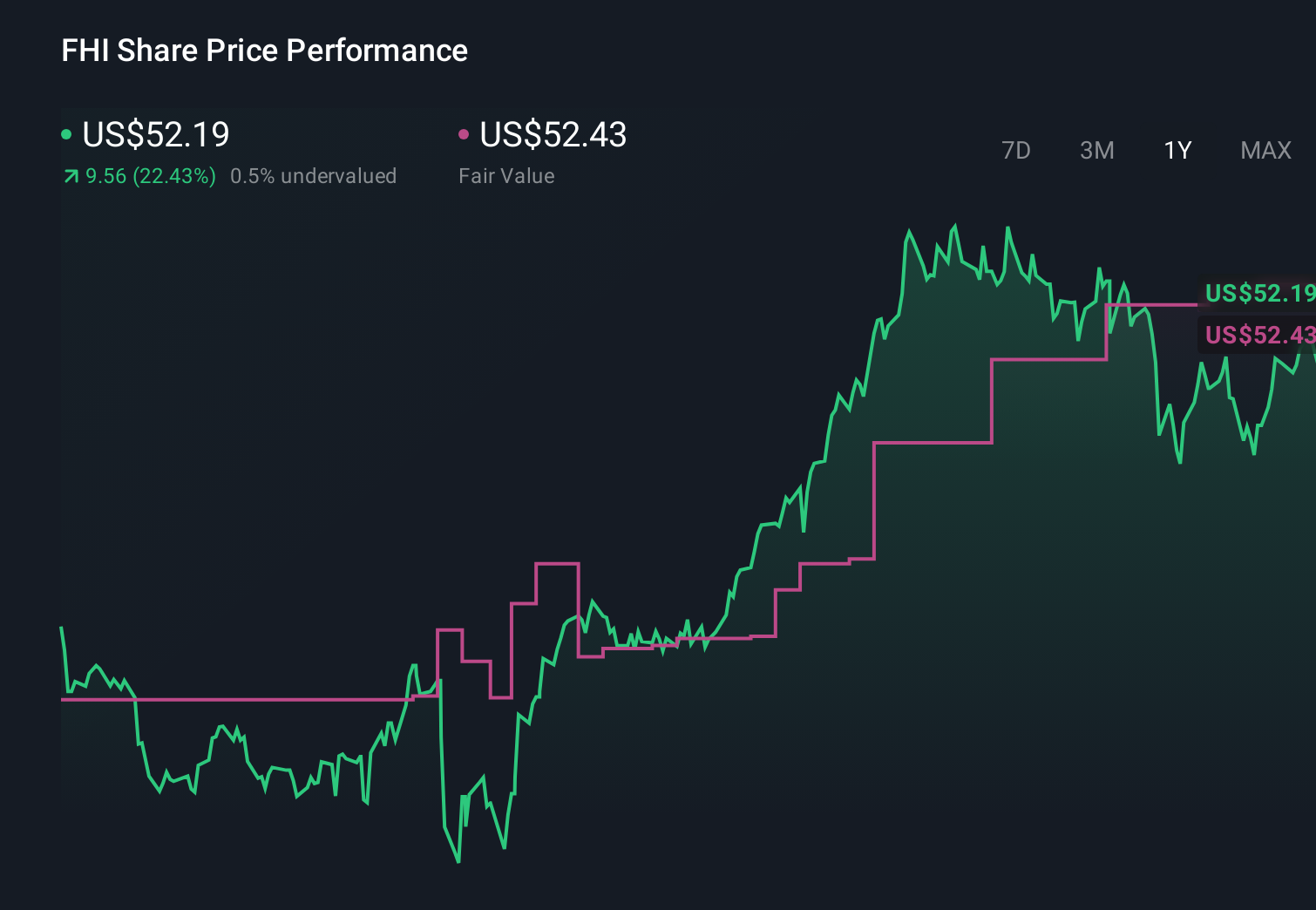

Uncover how Federated Hermes' forecasts yield a $57.14 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently place fair value for Federated Hermes between US$52.35 and US$68.27, underscoring how far opinions can diverge. Against this spread, the central risk that fee compression and passive products could pressure active management margins over time is a key factor readers may want to weigh when comparing these different views.

Explore 4 other fair value estimates on Federated Hermes - why the stock might be worth just $52.35!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Federated Hermes research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Federated Hermes research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Federated Hermes' overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com