- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Vaxcyte (PCVX) Is Down 10.1% After Wider Q1 Loss But Completing Key VAX-31 Phase 3 Enrollment

- Vaxcyte recently reported first-quarter 2026 results showing a wider net loss of US$320.62 million, with basic and diluted loss per share from continuing operations of US$2.30, compared with a loss of US$140.72 million and US$1.04 per share a year earlier.

- Around the same time, the company completed enrollment in its adult Phase 3 OPUS-1, OPUS-2 and OPUS-3 trials for VAX-31 and set plans to start a Phase 1 adult study for its VAX-A1 Group A Strep vaccine candidate, signaling meaningful progress across its late-stage and early-stage vaccine pipeline despite higher quarterly losses.

- Next, we’ll examine how completing enrollment in the VAX-31 Phase 3 OPUS trials might influence Vaxcyte’s existing investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

Vaxcyte Investment Narrative Recap

To own Vaxcyte, you need to believe its broad pneumococcal and Group A Strep pipeline can eventually justify years of heavy spending before any commercial revenue. The wider first quarter 2026 loss and rising per share losses highlight the main near term risk: cash burn and potential future financing needs. Completing enrollment across the adult OPUS Phase 3 trials keeps the key short term catalyst intact, as investors now look ahead to the first OPUS-1 readout in late 2026.

Among recent updates, the completion of enrollment in OPUS-1, OPUS-2 and OPUS-3 for VAX-31 is most relevant here. It ties the current increase in losses directly to progress on the pivotal adult program that underpins the investment thesis and the timing of potential future regulatory filings. In parallel, the planned mid 2026 Phase 1 start for VAX-A1 adds an earlier stage, higher uncertainty program that could amplify both the upside and the execution risk profile.

Yet behind this apparent pipeline momentum, investors should be aware of how quickly higher quarterly losses could interact with...

Read the full narrative on Vaxcyte (it's free!)

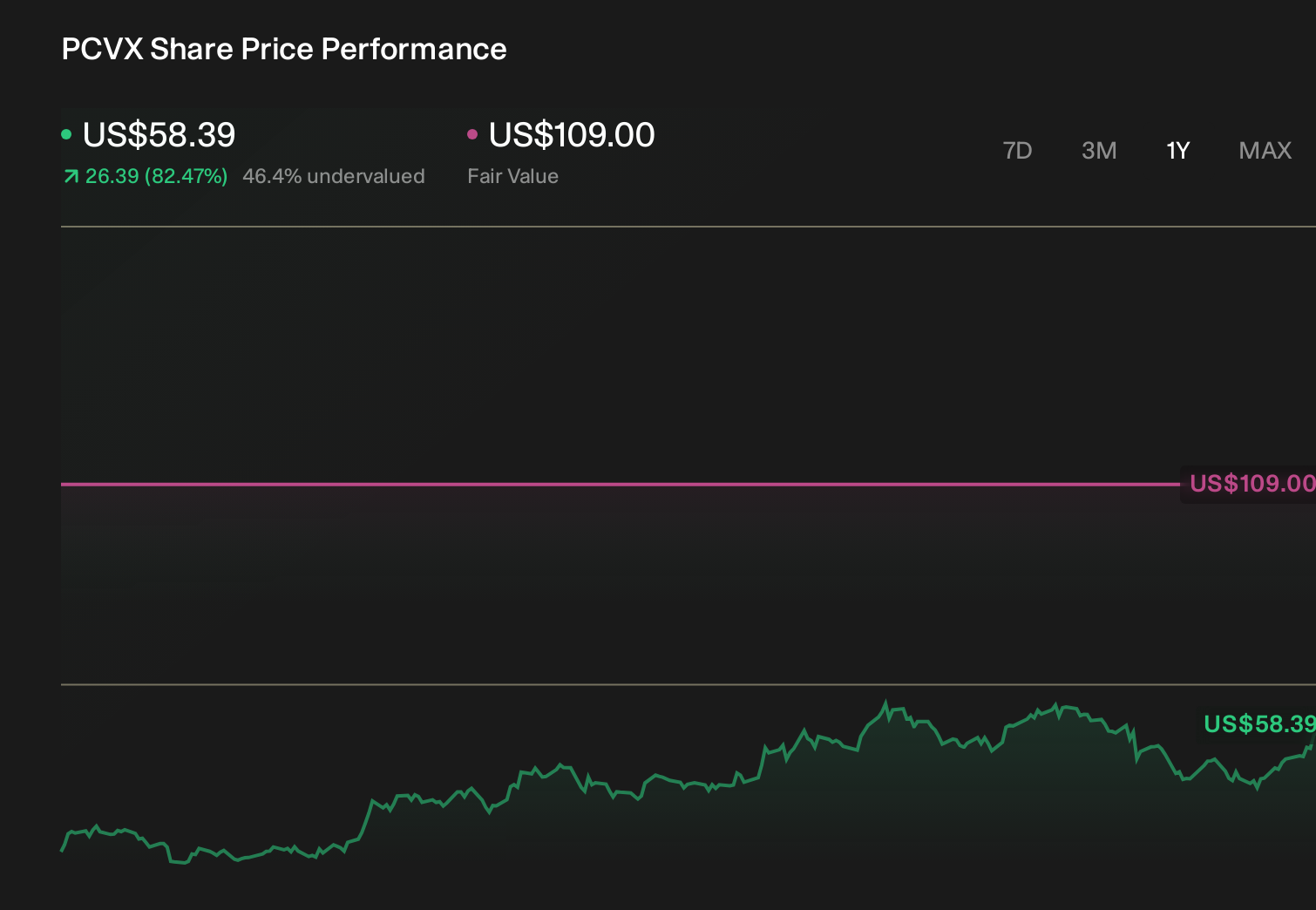

Vaxcyte's narrative projects $224.6 million in revenue and $28.1 million in earnings by 2029. This implies an earnings increase of about $794.7 million from -$766.6 million today.

Uncover how Vaxcyte's forecasts yield a $109.00 fair value, a 112% upside to its current price.

Exploring Other Perspectives

While the consensus sees OPUS data as a key catalyst, the most pessimistic analysts, who only projected about US$15.3 million of revenue by 2029, highlight how differing views on trial outcomes and cash burn can lead to very different expectations for Vaxcyte’s future.

Explore 3 other fair value estimates on Vaxcyte - why the stock might be worth just $93.03!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Vaxcyte research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Vaxcyte research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vaxcyte's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com