- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Ingersoll Rand (IR) Valuation After Recent Share Price Weakness

Why Ingersoll Rand (IR) is on investors’ radar

Ingersoll Rand (IR) has drawn investor attention after a period of mixed share performance, with the stock showing negative returns over the past week, month and past 3 months despite positive multi year total returns.

See our latest analysis for Ingersoll Rand.

At a share price of US$77.50, Ingersoll Rand’s short term share price return has been weak, with a 21.32% 3 month decline. However, the 3 year total shareholder return of 34.14% reflects a much stronger longer term outcome.

If you are comparing IR with other industrial and infrastructure related opportunities, it can help to widen the lens and review 36 power grid technology and infrastructure stocks

With annual revenue and net income growth, a small modeled intrinsic discount, and a price about 22% below the average analyst target, is IR quietly offering value, or is the market already baking in the next leg of growth?

Most Popular Narrative: 20% Undervalued

Ingersoll Rand’s most followed narrative points to a fair value of about $96.47 per share, compared with the recent close at $77.50. This puts the focus firmly on future cash generation and profitability assumptions behind that gap.

Ingersoll Rand is capitalizing on accelerating global demand for energy-efficient and sustainable industrial equipment, supported by new breakthroughs like the CompAir Ultima oil-free compressor and the EVO Series electric diaphragm pump, both delivering notable efficiency gains. These innovations reinforce pricing power and are anticipated to drive revenue growth and margin expansion as regulatory and customer focus on sustainability intensifies.

Curious what kind of revenue path, margin uplift and future P/E this narrative needs to reach that fair value number? The full story spells out a detailed glide path for growth, profitability and share count that goes well beyond recent results.

Result: Fair Value of $96.47 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on acquisitions adding value and industrial spending holding up, since difficult integrations or weaker capital investment could quickly challenge that 20% undervalued story.

Find out about the key risks to this Ingersoll Rand narrative.

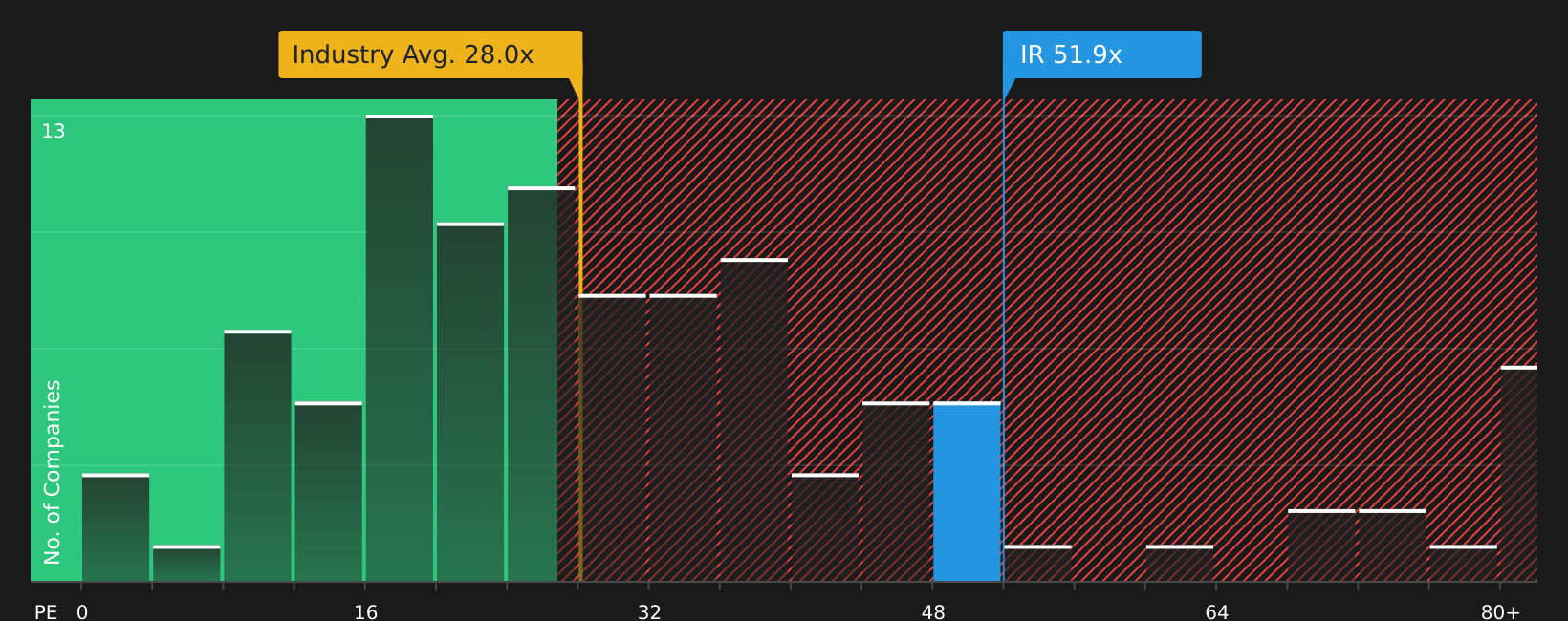

Another View: Rich Earnings Multiple Raises the Bar

The underpriced story built around fair value sits beside a very different signal from the current P/E. IR trades on 51.7x earnings, compared with about 28x for the US Machinery industry, 36.8x for peers and a fair ratio of 38.2x, which points to meaningful valuation risk if sentiment cools.

That kind of premium means investors are paying a higher price for the growth and margin narrative. The key question is whether IR can deliver enough earnings progress for the share price to grow into this multiple or if expectations may prove too full.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages on value and expectations can be confusing, so check the underlying data, weigh both the risks and rewards, and decide whether the story adds up for you with 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If IR feels interesting but you want stronger diversification, do not stop here. Widen your search with targeted stock ideas that fit different portfolio goals.

- Target potential mispricing by scanning companies that combine quality fundamentals with attractive pricing through the 51 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies offering higher yields and resilient payouts using the 12 dividend fortresses.

- Prioritise resilience by focusing on companies with lower risk characteristics and steadier profiles via the 72 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com