- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

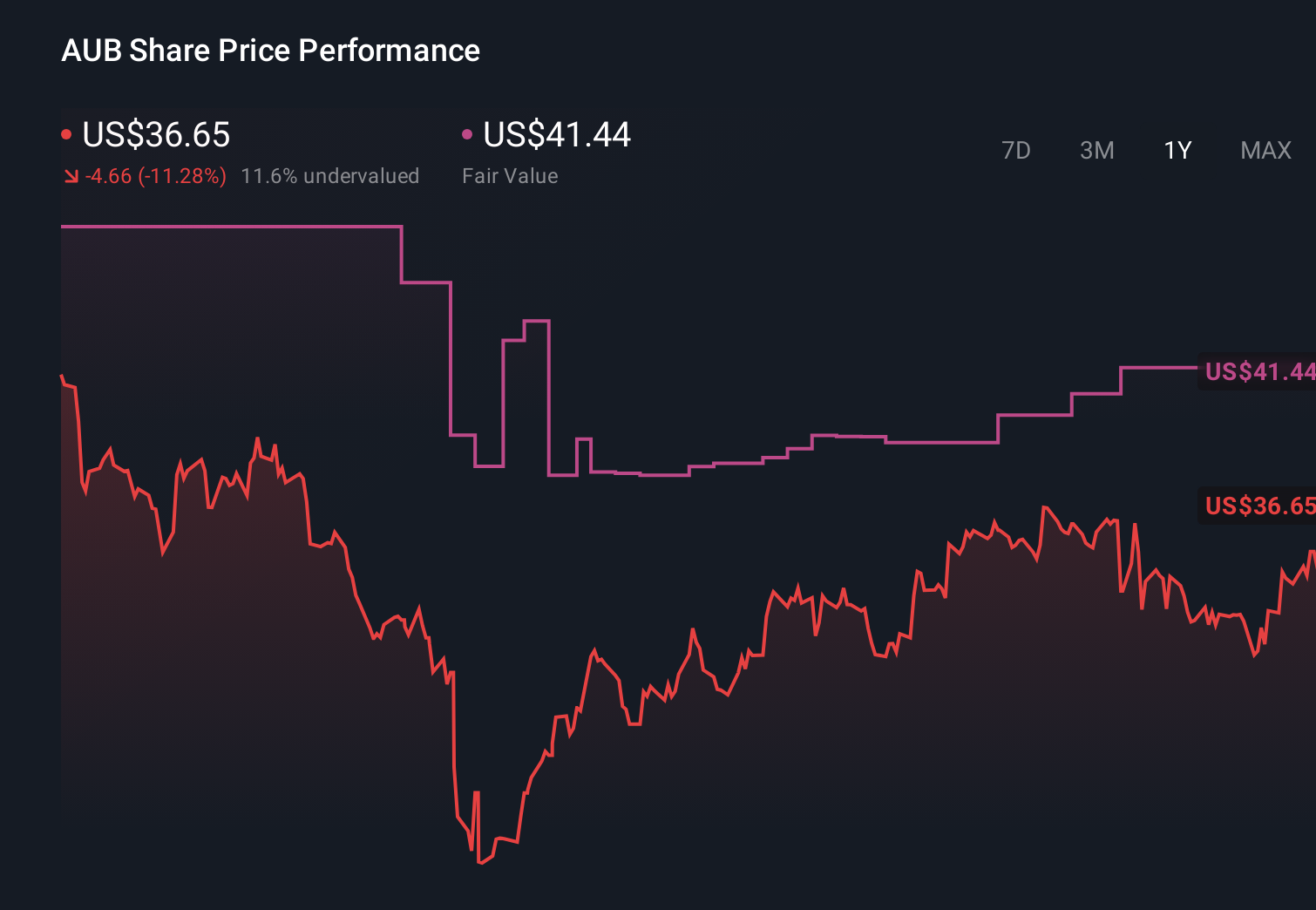

The Bull Case For Atlantic Union Bankshares (AUB) Could Change Following New Buyback And Dividend Plan - Learn Why

- In early May 2026, Atlantic Union Bankshares Corporation declared its regular quarterly dividends on common and 6.875% Series A preferred stock, while also unveiling Board authorization for a new US$250 million common share repurchase program running through May 5, 2027.

- Together, these cash returns and planned buybacks highlight management’s current focus on capital distribution alongside ongoing community initiatives such as supporting affordable housing developments in Washington, D.C.

- Next, we’ll examine how the newly authorized US$250 million share repurchase program may influence Atlantic Union Bankshares’ investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Atlantic Union Bankshares Investment Narrative Recap

To own Atlantic Union Bankshares, you need to believe in its community banking model across the Mid Atlantic, its expansion into growth markets, and its ability to manage credit and integration risks. The new US$250 million buyback and reaffirmed dividends signal no obvious change to the near term earnings catalyst or to the key risks around regional concentration and post acquisition execution.

The newly authorized US$250 million share repurchase program is the most relevant development here, because it sits alongside management’s existing focus on efficiency and capital deployment. How aggressively this authorization is used could intersect with the ongoing integration of recent acquisitions and investments in digital capabilities that underpin the core growth narrative.

Yet against this, investors should be aware of how concentrated Atlantic Union remains in Mid Atlantic economies and how quickly digital only competitors are...

Read the full narrative on Atlantic Union Bankshares (it's free!)

Atlantic Union Bankshares’ narrative projects $1.8 billion revenue and $698.6 million earnings by 2029.

Uncover how Atlantic Union Bankshares' forecasts yield a $44.00 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Four fair value estimates from the Simply Wall St Community span a wide US$30.79 to US$59.16 range, underlining how differently individual investors read Atlantic Union’s prospects. You should weigh these views against the bank’s heavy Mid Atlantic exposure and integration and digital execution risks, which could all shape how those valuations play out over time.

Explore 4 other fair value estimates on Atlantic Union Bankshares - why the stock might be worth as much as 56% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Atlantic Union Bankshares research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Atlantic Union Bankshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Atlantic Union Bankshares' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 17 early-stage AI stocks could fund your retirement.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com