- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

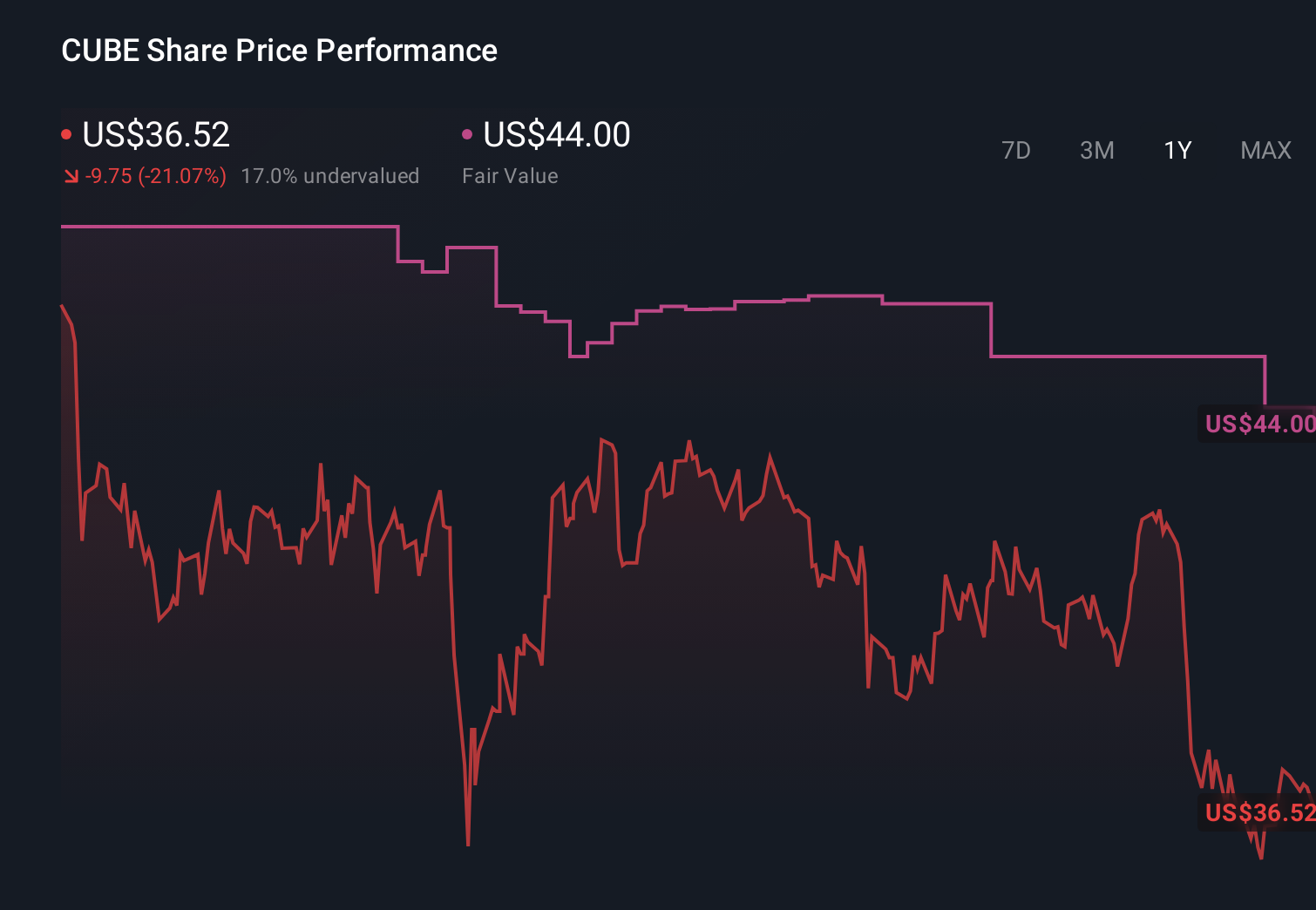

The Bull Case For CubeSmart (CUBE) Could Change Following Reaffirmed 2026 Earnings Guidance And Q1 Results

- In April 2026, CubeSmart reported first-quarter 2026 results showing sales of US$239.93 million and revenue of US$281.93 million, with net income easing to US$82.89 million and diluted EPS from continuing operations at US$0.36, while also issuing second-quarter and reaffirmed full-year 2026 earnings guidance.

- Alongside modest top-line growth, CubeSmart’s guidance for fully diluted 2026 EPS of US$1.55–US$1.63 and same-store revenue growth between 0.25% decline and 1.25% highlights management’s cautious yet steady outlook for its storage portfolio.

- We’ll now examine how CubeSmart’s reaffirmed full-year 2026 earnings guidance could influence its investment narrative and long-term business assumptions.

Outshine the giants: these 17 early-stage AI stocks could fund your retirement.

CubeSmart Investment Narrative Recap

To own CubeSmart, I think you need to believe that storage demand and disciplined cost control can offset near term pressure from softer same store growth and Sunbelt competition. The reaffirmed 2026 EPS and revenue guidance suggests the latest quarter does not materially change the key near term catalyst of operating stabilization, nor does it remove the main risk that subdued same store revenue growth could drag on earnings momentum.

The most relevant update here is CubeSmart’s reaffirmed full year 2026 diluted EPS guidance of US$1.55 to US$1.63, paired with same store revenue growth of negative 0.25% to 1.25%. This guidance frames expectations around how quickly move in rates and portfolio level revenue can recover, which sits at the heart of today’s biggest catalyst and the risk that stabilization proves slower than investors hope.

Yet beneath this steady 2026 outlook, investors should be aware that slower same store revenue growth could still...

Read the full narrative on CubeSmart (it's free!)

CubeSmart's narrative projects $1.2 billion revenue and $347.3 million earnings by 2029.

Uncover how CubeSmart's forecasts yield a $42.00 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community estimate CubeSmart’s fair value between US$40.00 and about US$52.86, highlighting a wide spread of views. Against this, management’s cautious same store revenue outlook reminds you that differing growth assumptions can materially shape expectations for the business over time.

Explore 4 other fair value estimates on CubeSmart - why the stock might be worth just $40.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CubeSmart research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CubeSmart research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CubeSmart's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com