- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

3 Dividend Stocks Yielding Over 3.2% To Enhance Your Portfolio

The United States market has experienced a notable upswing, rising 1.8% over the last week and showing an impressive 30% increase over the past year, with earnings projected to grow by 16% annually in the coming years. In this vibrant market environment, dividend stocks yielding over 3.2% can be a strategic choice for investors seeking to enhance their portfolios with reliable income streams and potential long-term growth.

Top 10 Dividend Stocks In The United States

| Name | Dividend Yield | Dividend Rating |

| Peoples Bancorp (PEBO) | 4.92% | ★★★★★☆ |

| OTC Markets Group (OTCM) | 5.27% | ★★★★★★ |

| Huntington Bancshares (HBAN) | 3.78% | ★★★★★☆ |

| Host Hotels & Resorts (HST) | 4.46% | ★★★★★☆ |

| First Interstate BancSystem (FIBK) | 5.24% | ★★★★★★ |

| Ennis (EBF) | 4.87% | ★★★★★★ |

| Donegal Group (DGIC.A) | 4.66% | ★★★★★★ |

| Dillard's (DDS) | 5.58% | ★★★★★★ |

| Columbia Banking System (COLB) | 4.98% | ★★★★★★ |

| Accenture (ACN) | 3.64% | ★★★★★☆ |

Click here to see the full list of 100 stocks from our Top US Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

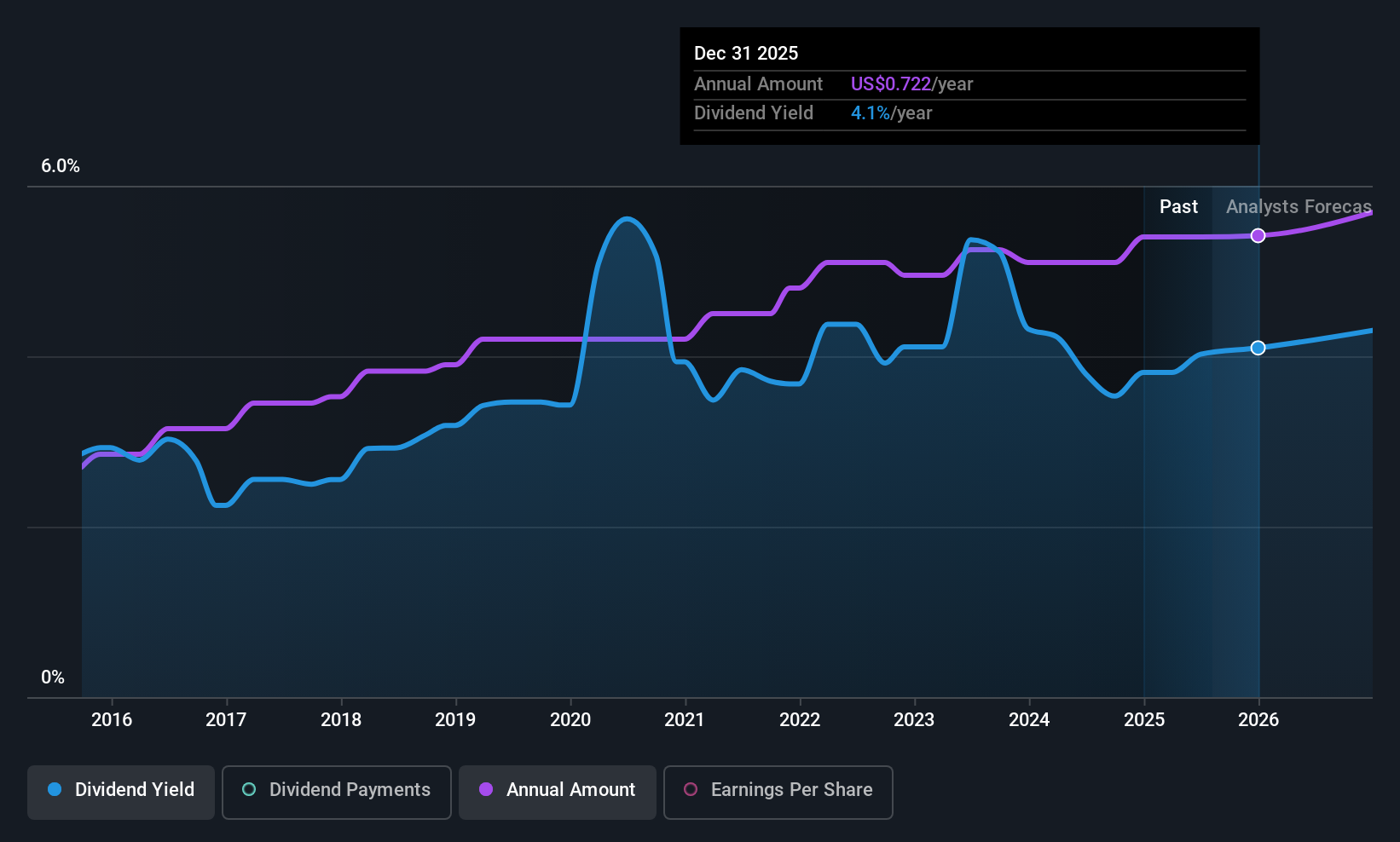

Fulton Financial (FULT)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Fulton Financial Corporation, with a market cap of $4.06 billion, operates as the bank holding company for Fulton Bank, offering a range of banking and financial products and services in the United States.

Operations: Fulton Financial Corporation generates its revenue primarily from its banking segment, which accounts for $1.29 billion.

Dividend Yield: 3.5%

Fulton Financial offers a stable dividend, having consistently increased payments over the past decade. While its 3.52% yield is below the top 25% of U.S. dividend payers, it remains reliable with a low payout ratio of 35%, indicating earnings comfortably cover dividends. Recent financials show modest growth in net interest income and net income for Q1 2026. The company has completed a $300 million fixed-income offering and repurchased shares worth $24.5 million, reflecting strategic capital management initiatives.

- Unlock comprehensive insights into our analysis of Fulton Financial stock in this dividend report.

- The valuation report we've compiled suggests that Fulton Financial's current price could be quite moderate.

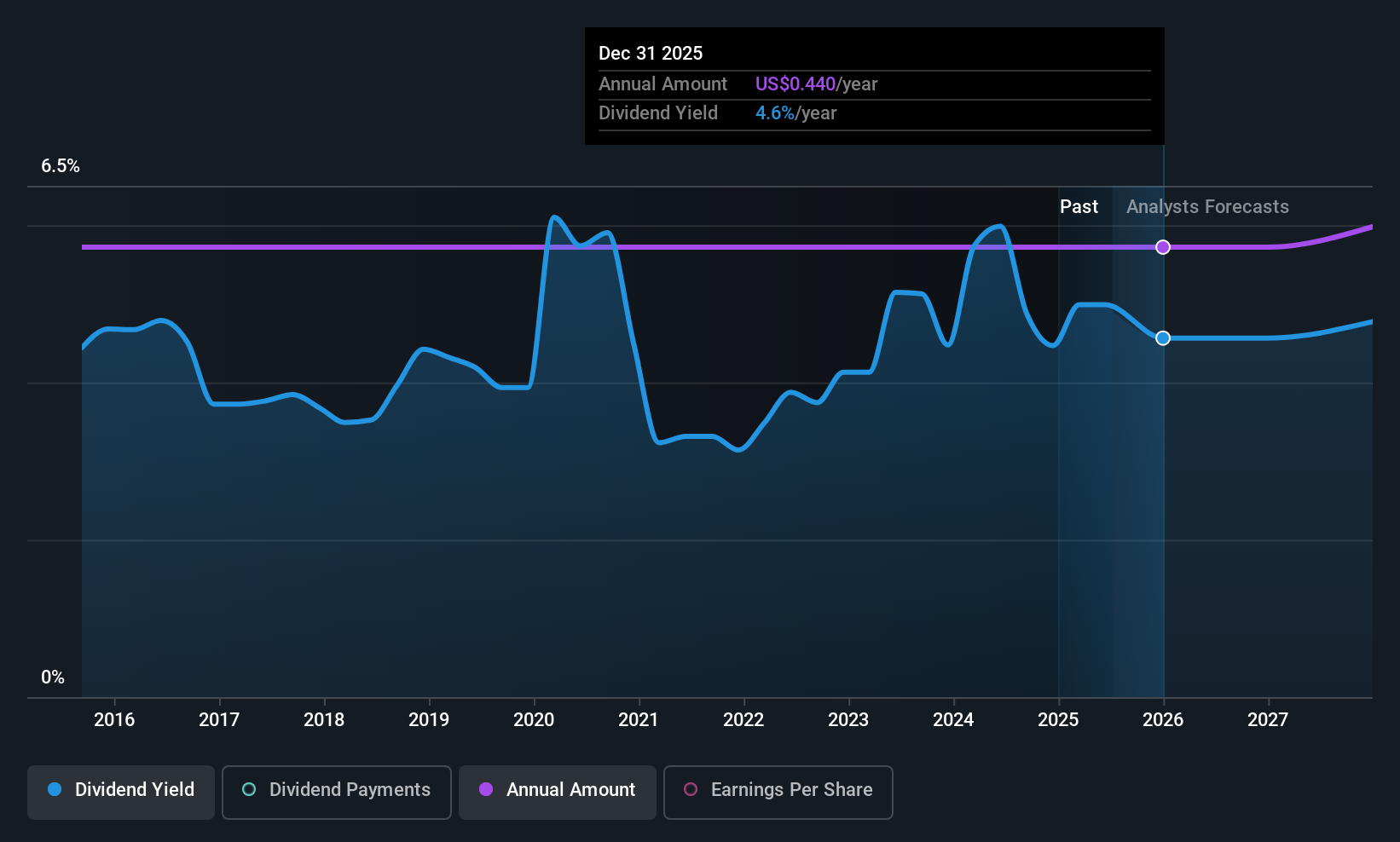

Valley National Bancorp (VLY)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Valley National Bancorp is the holding company for Valley National Bank, offering a range of commercial, private banking, retail, insurance, and wealth management services with a market cap of approximately $7.46 billion.

Operations: Valley National Bancorp generates revenue through its diverse financial services, including commercial banking, private banking, retail banking, insurance products, and wealth management.

Dividend Yield: 3.2%

Valley National Bancorp offers a stable dividend, though it hasn't grown over the past decade. The 3.22% yield is below the top U.S. dividend payers, but dividends are well covered by earnings with a payout ratio of 39.2%. Recent Q1 2026 results show robust growth in net interest income and net income, alongside reduced net charge-offs compared to last year. A share repurchase program for up to 25 million shares reflects strategic financial management.

- Dive into the specifics of Valley National Bancorp here with our thorough dividend report.

- The analysis detailed in our Valley National Bancorp valuation report hints at an deflated share price compared to its estimated value.

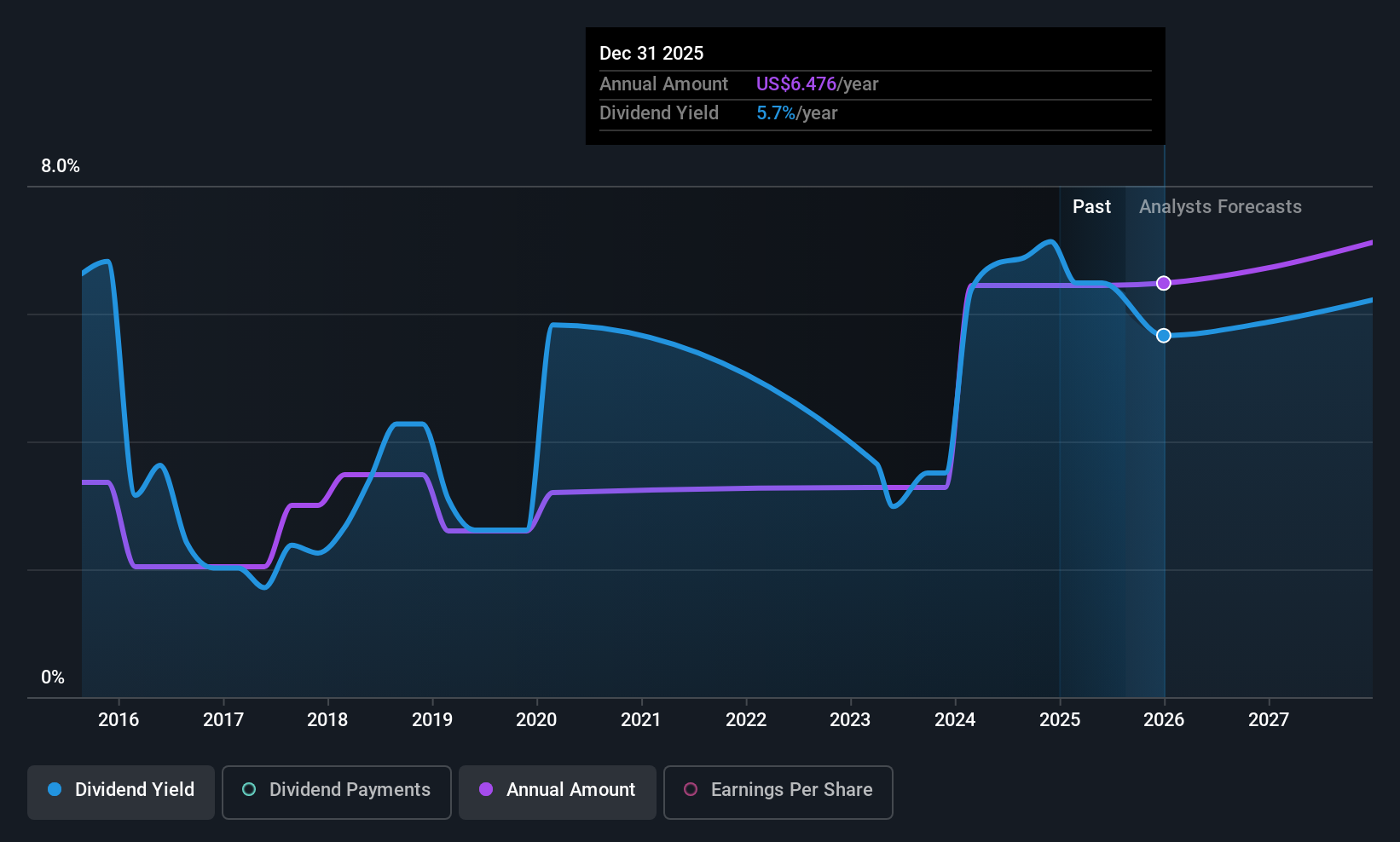

Copa Holdings (CPA)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Copa Holdings, S.A. operates as an airline offering passenger, cargo, and mail transportation services across North America, South America, Central America, and the Caribbean with a market cap of $4.58 billion.

Operations: Copa Holdings generates its revenue primarily from air transportation services, amounting to $3.62 billion.

Dividend Yield: 6%

Copa Holdings offers a high dividend yield of 6.02%, ranking in the top 25% of U.S. dividend payers, but its sustainability is questionable due to a cash payout ratio exceeding free cash flow. Despite volatile dividends over the past decade, recent increases have been approved for 2026. The company trades below fair value and has shown strong earnings growth, supported by rising traffic metrics and strategic share buybacks totaling US$96.01 million since late 2023.

- Delve into the full analysis dividend report here for a deeper understanding of Copa Holdings.

- Our valuation report unveils the possibility Copa Holdings' shares may be trading at a discount.

Turning Ideas Into Actions

- Unlock our comprehensive list of 100 Top US Dividend Stocks by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com