- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Exploring 3 Undiscovered Gems in the US Market

The United States market has remained flat over the last week but is up 28% over the past year, with earnings expected to grow by 16% annually. In this dynamic environment, identifying stocks that are poised for growth yet remain under the radar can offer unique opportunities for investors seeking to capitalize on emerging trends and untapped potential.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.27% | 1.25% | -3.09% | ★★★★★★ |

| Security Federal | 17.59% | 5.00% | -1.81% | ★★★★★★ |

| Cashmere Valley Bank | 31.63% | 5.07% | 1.43% | ★★★★★★ |

| Bank of the James Financial Group | 10.99% | 5.06% | 2.18% | ★★★★★★ |

| Anbio Biotechnology | NA | -30.09% | -3.45% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.46% | 11.04% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

Willdan Group (WLDN)

Simply Wall St Value Rating: ★★★★★★

Overview: Willdan Group, Inc. offers professional, technical, and consulting services including engineering, program management, policy advisory, and software and data analytics mainly in the United States with a market capitalization of $1.11 billion.

Operations: The company generates revenue primarily from two segments: Energy, contributing $576.05 million, and Engineering & Consulting, contributing $105.50 million.

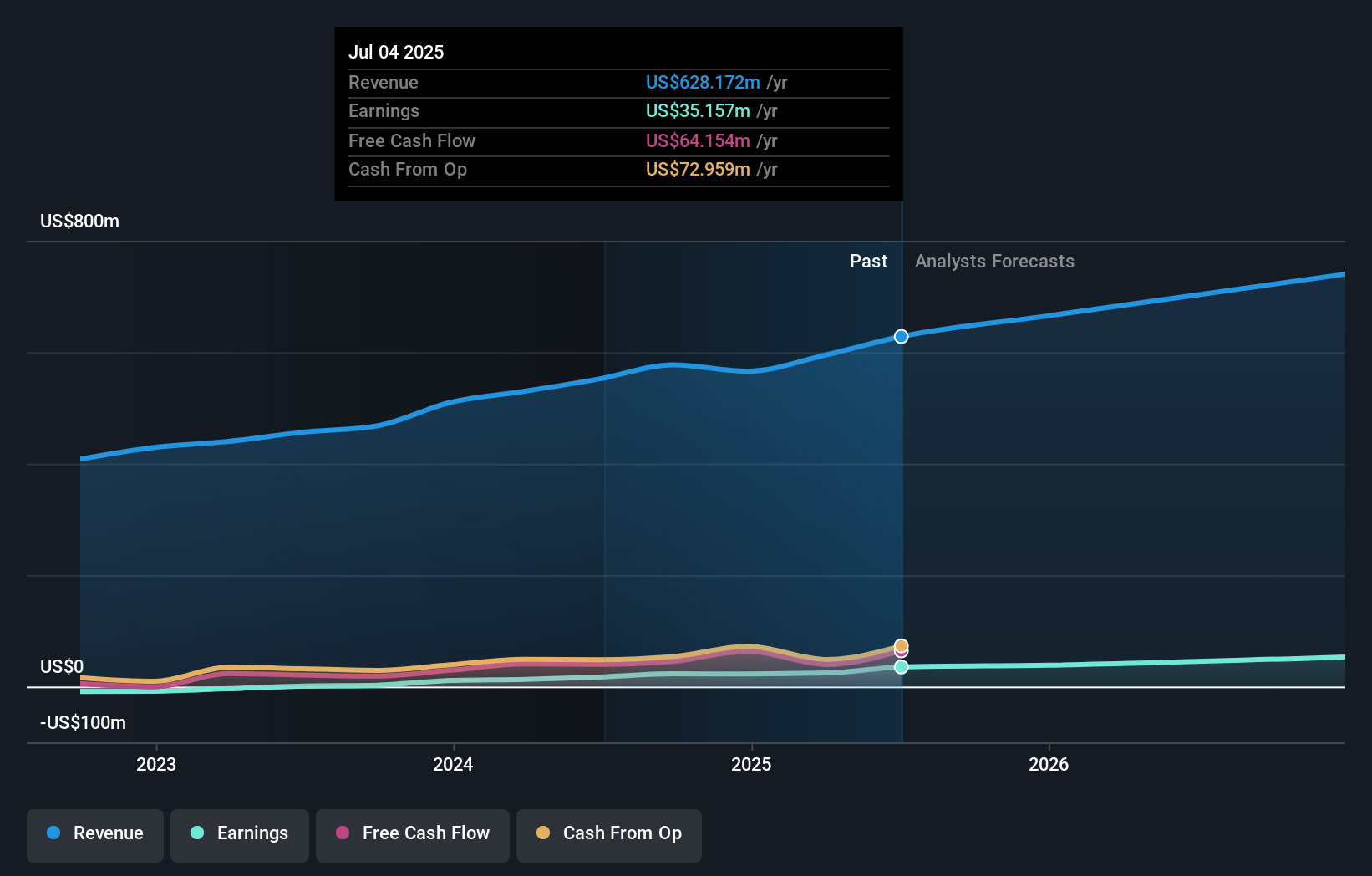

Willdan Group, a nimble player in the professional services sector, has shown remarkable earnings growth of 131.8% over the past year, significantly outpacing its industry peers. The company's debt-to-equity ratio has impressively decreased from 67.3% to 15.9% over five years, indicating strong financial health with more cash than total debt on hand. Recent projects like a $27 million contract with New York City and a $112 million deal with San Diego for energy efficiency highlight its strategic positioning in the sustainability space. Trading at nearly half its estimated fair value suggests potential for investors eyeing growth opportunities in infrastructure and green initiatives.

Ituran Location and Control (ITRN)

Simply Wall St Value Rating: ★★★★★★

Overview: Ituran Location and Control Ltd., along with its subsidiaries, offers location-based telematics services and machine-to-machine telematics products across Israel, Brazil, and other international markets, with a market cap of $1.16 billion.

Operations: Ituran generates revenue primarily from its telematics services and products. The company has reported a net profit margin of 12.5%, reflecting its profitability in the industry.

Ituran Location and Control, a nimble player in the telematics sector, is debt-free and boasts high-quality earnings. The company has seen its earnings grow at an impressive 17.8% annually over the past five years, with a Price-To-Earnings ratio of 20x that sits comfortably below the industry average of 35.4x. Recent collaborations with automotive giants like Daimler India and Nissan are likely to enhance revenue streams as Ituran expands into untapped markets through innovative services like motorcycle telematics in South America. Despite these promising developments, currency fluctuations could impact profitability when converting earnings to U.S. dollars.

REX American Resources (REX)

Simply Wall St Value Rating: ★★★★★★

Overview: REX American Resources Corporation, along with its subsidiaries, is engaged in the production and sale of ethanol in the United States, with a market capitalization of approximately $1.65 billion.

Operations: REX American Resources generates revenue primarily from ethanol and by-products, amounting to $1.66 billion. The company also reports a negative figure of -$1.01 billion related to unallocated equity method ethanol investments.

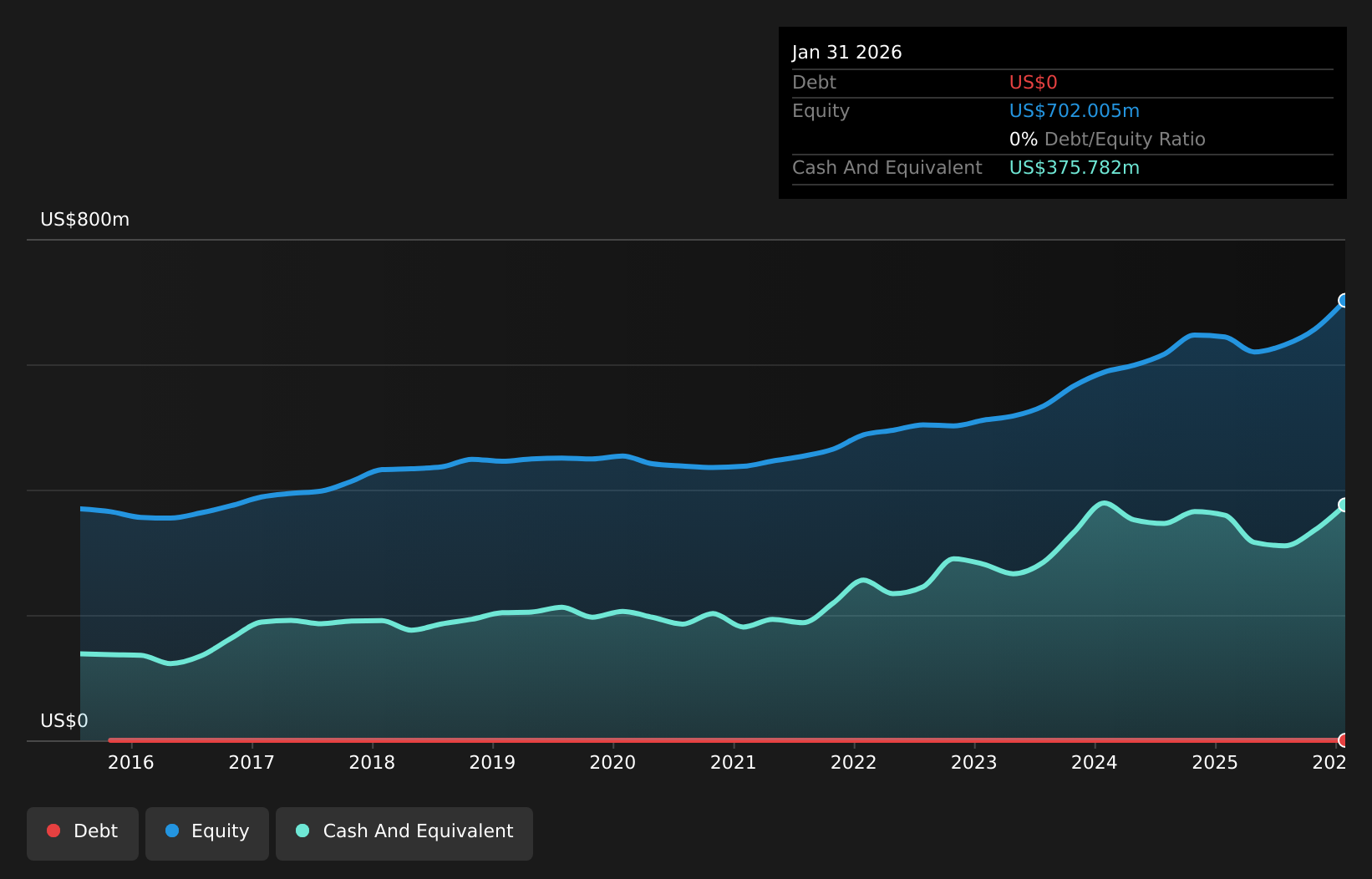

REX American Resources, a nimble player in the ethanol and carbon capture sectors, is making strategic moves to bolster its financial standing. With no debt on its books for the past five years and earnings growth of 42.6% over the last year, REX stands out in its industry. Trading at a 12.8% discount to fair value estimates, it offers potential upside for investors. Despite facing regulatory risks and cost pressures, REX's initiatives like share repurchases—totaling $65.41 million since 2021—aim to enhance shareholder value while navigating challenges such as low selling prices impacting profit margins currently at 9%.

Make It Happen

- Investigate our full lineup of 337 US Undiscovered Gems With Strong Fundamentals right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com