- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

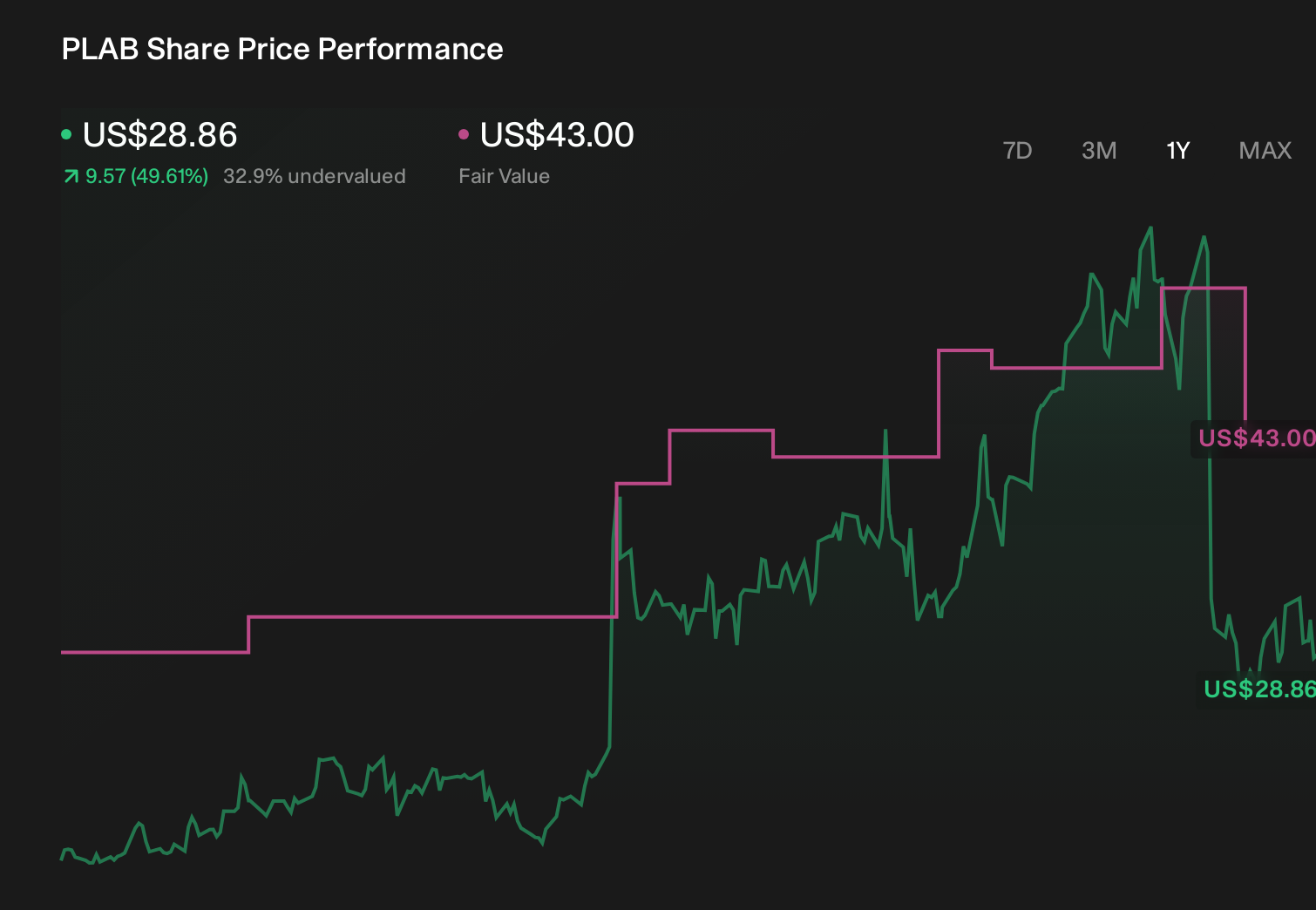

Positive Momentum and Analyst Optimism Around Photronics’ Photomask Niche Might Change The Case For Investing In Photronics (PLAB)

- In recent weeks, Photronics drew renewed attention after passing a price‑momentum screen and receiving upbeat analyst coverage highlighting its current strength in the semiconductor photomask market.

- What stands out is the combination of positive momentum signals and broadly favorable analyst recommendations, which together suggest increasing confidence in how the company is positioned within semiconductor materials and equipment.

- Next, we will examine how this analyst optimism about Photronics’ role in semiconductor photomasks influences the company’s broader investment narrative.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

Photronics Investment Narrative Recap

To own Photronics, you need to believe that its position in semiconductor photomasks and display masks will keep it relevant as chip complexity and advanced displays evolve. Recent price momentum and more positive analyst commentary support that view but do not materially change the key short term catalyst, which is execution on new capacity and technology ramps, or the biggest risk, which is still end market and order visibility volatility.

The most relevant recent announcement here is the delivery of Photronics’ most advanced mask writer to its Korea facility, scheduled for installation in Q2 2026. This upgrade ties directly to its growth catalyst in AMOLED and Gen 8.6 displays, where higher mask complexity could support better economics, while still leaving the company exposed to swings in demand and capital intensity in Asia.

Yet behind the recent momentum and capacity upgrades, investors should be aware that...

Read the full narrative on Photronics (it's free!)

Photronics' narrative projects $973.4 million revenue and $138.1 million earnings by 2029. This requires 4.1% yearly revenue growth and about a $1.6 million earnings increase from $136.5 million today.

Uncover how Photronics' forecasts yield a $47.00 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span roughly US$19.30 to US$47.00, underlining how differently individual investors see Photronics. Set against this wide range, the company’s heavy multiyear capital spending program raises important questions about how consistently future returns on those investments might support the current market price.

Explore 6 other fair value estimates on Photronics - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Photronics research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com