- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Delek Logistics Partners (DKL) Valuation As Recent Price Gains Meet Conflicting Fair Value Signals

Setting the scene for Delek Logistics Partners

With no single headline event driving attention, Delek Logistics Partners (DKL) is drawing interest as investors weigh its recent share performance, current valuation metrics, and the scale of its US$2.9b market footprint.

See our latest analysis for Delek Logistics Partners.

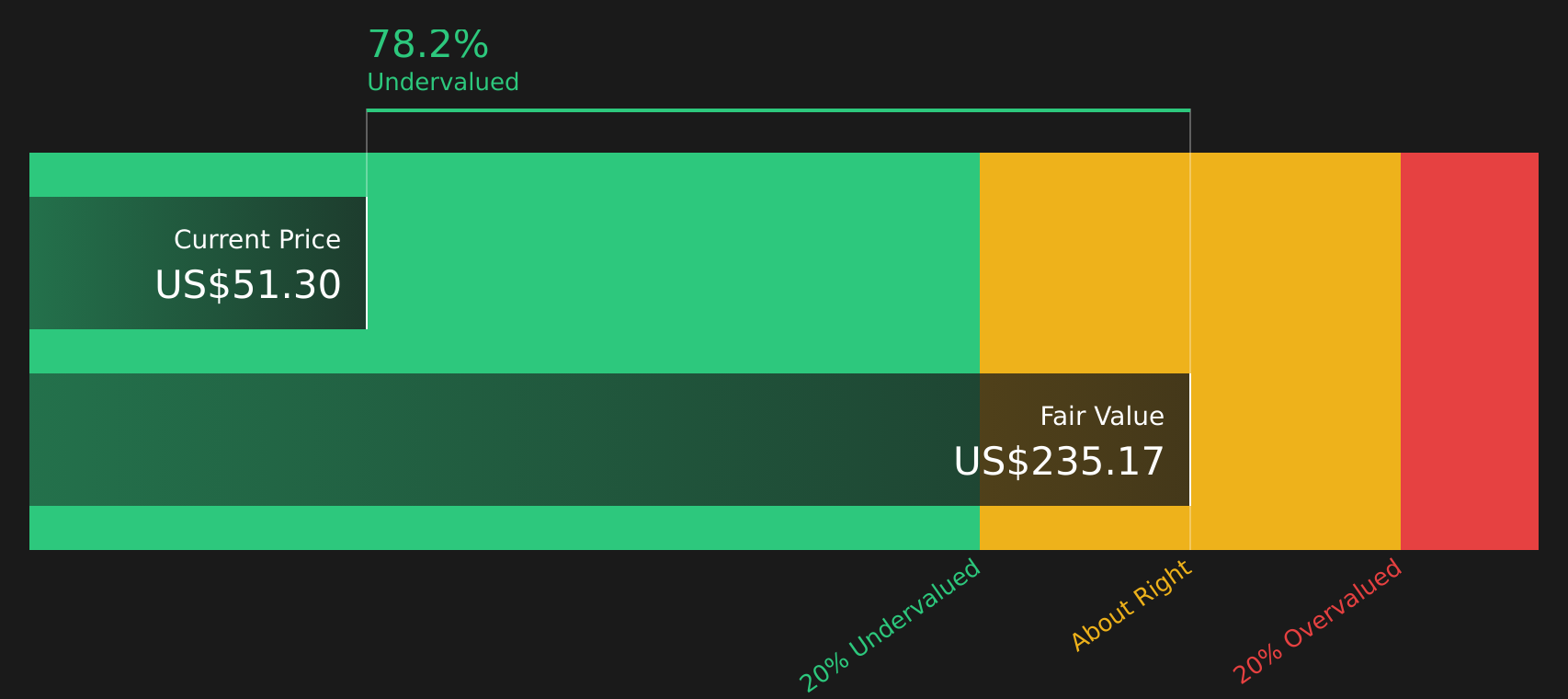

At a share price of US$53.95, Delek Logistics Partners has seen momentum build recently, with a 7.3% 1 month share price return and a 14.8% year to date share price return contributing to a 55.0% 1 year total shareholder return.

If you are looking beyond midstream and energy, this could be a good moment to broaden your search with the 17 top founder-led companies

With Delek Logistics Partners trading near US$53.95, ahead of its analyst price target and with an intrinsic value estimate suggesting a wide discount, you have to ask whether this is a genuine mispricing or whether the market is already factoring in future growth.

Most Popular Narrative: 5% Overvalued

With the most followed narrative putting fair value at $51.40 versus the last close of $53.95, the current unit price sits slightly ahead of that estimate while the story leans heavily on future project execution.

The full commissioning and expected ramp to capacity of the new Libby 2 gas plant in the Delaware Basin, along with associated investments (amine unit and AGI wells), positions Delek Logistics to capitalize on rising energy demand and stable domestic energy infrastructure needs, likely boosting gathering and processing volumes, EBITDA, and revenue growth.

Want to see how a single gas complex, fee based contracts, and margin assumptions combine to justify that fair value gap and future earnings profile?

Result: Fair Value of $51.40 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh the risk that high leverage and reliance on fossil fuel demand could pressure returns if volumes or contract terms shift against expectations.

Find out about the key risks to this Delek Logistics Partners narrative.

Another Angle On What The Price Is Saying

The consensus narrative suggests Delek Logistics Partners is about 5% overvalued at $53.95 versus a $51.40 fair value. Yet the SWS DCF model presents a different perspective, with a future cash flow value of $247.84 per unit, indicating the market may be applying a substantial discount to long term cash generation. Which interpretation aligns more closely with your own assumptions?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Delek Logistics Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Feeling torn between the risks and rewards in this story? If you want to move past headlines to what the numbers actually say, take a moment to review the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Delek Logistics Partners has sharpened your focus, do not stop here. Broaden your watchlist with other opportunities that could better match your goals and risk comfort.

Use these focused stock ideas to stay ahead of the crowd and avoid missing companies that quietly fit your preferred mix of quality, value, and resilience.

- Spot potential bargains early by scanning 49 high quality undervalued stocks that combine solid fundamentals with prices the market may not fully appreciate yet.

- Prioritize resilience and sleep a little easier at night by checking 72 resilient stocks with low risk scores designed to highlight companies with lower overall risk scores.

- Unearth lesser known opportunities by searching the screener containing 25 high quality undiscovered gems that pair quality metrics with relatively limited current attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com