- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Enterprise Financial Services (EFSC) Valuation After Q1 Results And Dividend Declaration

Enterprise Financial Services (EFSC) drew fresh attention after reporting first quarter 2026 results, with net interest income of US$166.15 million, net income of US$49.36 million, and a quarterly common dividend set at US$0.34 per share.

See our latest analysis for Enterprise Financial Services.

The first quarter earnings, ongoing share repurchases totaling 3.68% of shares since 2022, and the latest common and preferred dividend declarations have come alongside an 8.95% year to date share price return and a 60.38% three year total shareholder return. Together, these factors suggest that momentum has been building over the medium term.

If this kind of banking story has your attention, it can be useful to compare it with other opportunities and see how different themes are playing out across the market, including 18 top founder-led companies

With EFSC trading at US$58.89, a value score of 5, an indicated intrinsic discount of 51.79% and an analyst target of US$65.80, you have to ask: is there still a buying opportunity here, or is future growth already priced in?

Preferred P/E of 10.9x: Is it justified?

On a P/E of 10.9x, Enterprise Financial Services screens as good value compared with both its peers and the wider US Banks industry, even after the recent share price gains.

The P/E ratio links the $58.89 share price to the company’s earnings. It gives you a quick sense of what the market is willing to pay for each dollar of profit. For a bank, that matters because earnings are closely tied to the core lending and fee based business rather than one off windfalls.

EFSC’s 10.9x P/E sits below the peer average of 13.3x and also below the US Banks industry average of 11.4x, pointing to a discount. The estimated fair P/E of 11.1x is only slightly higher than where the stock trades today.

Explore the SWS fair ratio for Enterprise Financial Services

Result: Price to earnings of 10.9x (UNDERVALUED)

However, you still need to weigh risks such as credit quality pressure on a US$693.68m banking book, as well as any potential setback to EFSC’s US focused growth plans.

Find out about the key risks to this Enterprise Financial Services narrative.

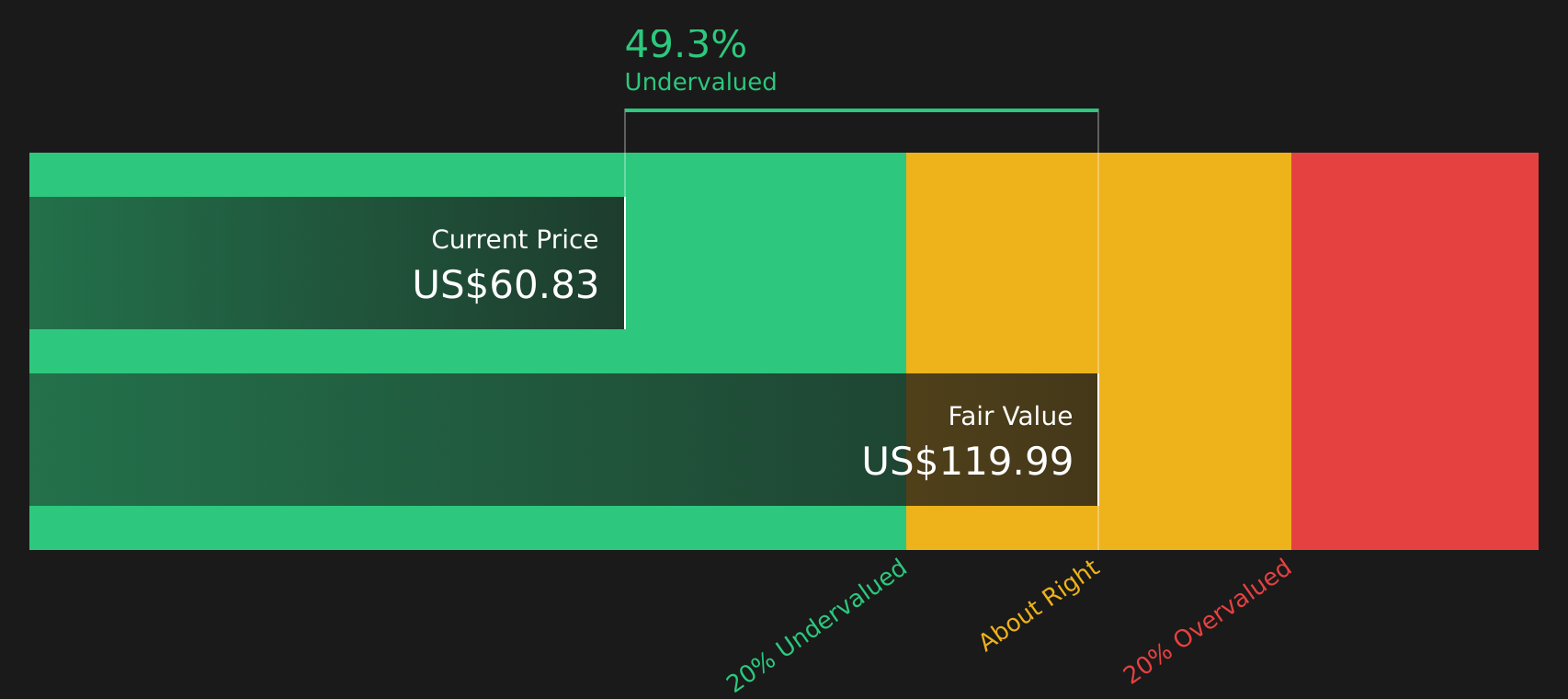

Another View: Cash Flows Paint An Even Cheaper Picture

While the 10.9x P/E suggests EFSC is trading at a discount, our DCF model goes further, valuing the shares at US$122.15 versus the current US$58.89. That gap hints at a much larger margin of safety, but also raises a question: are cash flow assumptions too generous or is the market too cautious?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enterprise Financial Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing both cautious questions and pockets of optimism, it makes sense to review the numbers yourself and decide promptly where you stand. Start by reviewing the 5 key rewards.

Looking for more investment ideas?

If EFSC has sharpened your interest, do not stop here, the wider market is full of other opportunities that could suit your style and goals.

- Target reliability with income potential by scanning for companies that look like 13 dividend fortresses.

- Spot quality at a discount by filtering for businesses flagged in the screener containing 25 high quality undiscovered gems.

- Prioritise sleep at night holdings by focusing on companies within the 70 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com