- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How CNH’s Weak Q1 Earnings And Reaffirmed 2026 Guidance Have Changed Its Investment Story (CNH)

- In the first quarter of 2026, CNH Industrial N.V. reported broadly flat sales at US$3,170 million and revenue at US$3,826 million, but net income dropped to US$7 million and basic earnings per share from continuing operations fell to US$0.01 compared with a year earlier.

- Management framed the quarter as the trough of the current agriculture cycle, keeping production low to reduce dealer inventories while reaffirming full-year 2026 guidance and highlighting efficiency gains such as faster processing at its Fargo plant.

- We’ll now examine how reaffirmed 2026 guidance amid weak agricultural demand and inventory reduction efforts shapes CNH Industrial’s investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

CNH Industrial Investment Narrative Recap

To own CNH Industrial, you need to believe that its mix of precision technology, operational improvements, and disciplined inventory management can eventually translate into healthier margins despite a tough agriculture backdrop. The latest quarter, with flat sales but sharply lower net income, underlines that the near term still revolves around one key catalyst and one key risk: management’s ability to execute on efficiency and inventory reduction while containing tariff and input cost pressures. This earnings print does not materially change that balance.

The most relevant recent update here is management’s reaffirmation of full year 2026 guidance alongside labeling Q1 as the trough in the agriculture cycle. Keeping production low to reduce dealer inventories by US$500 million, while targeting an industrial EBIT margin of 2.5% to 3.5% and adjusted EPS of US$0.35 to US$0.45, directly connects to the core catalyst of cleaner channels and better margins once demand stabilizes, but it also keeps tariff and cost inflation risks firmly in focus.

Yet investors should not ignore how tariff investigations and higher transport costs could suddenly reshape this story...

Read the full narrative on CNH Industrial (it's free!)

CNH Industrial's narrative projects $20.8 billion revenue and $1.4 billion earnings by 2029. This requires 4.7% yearly revenue growth and about a $900 million earnings increase from $510.0 million today.

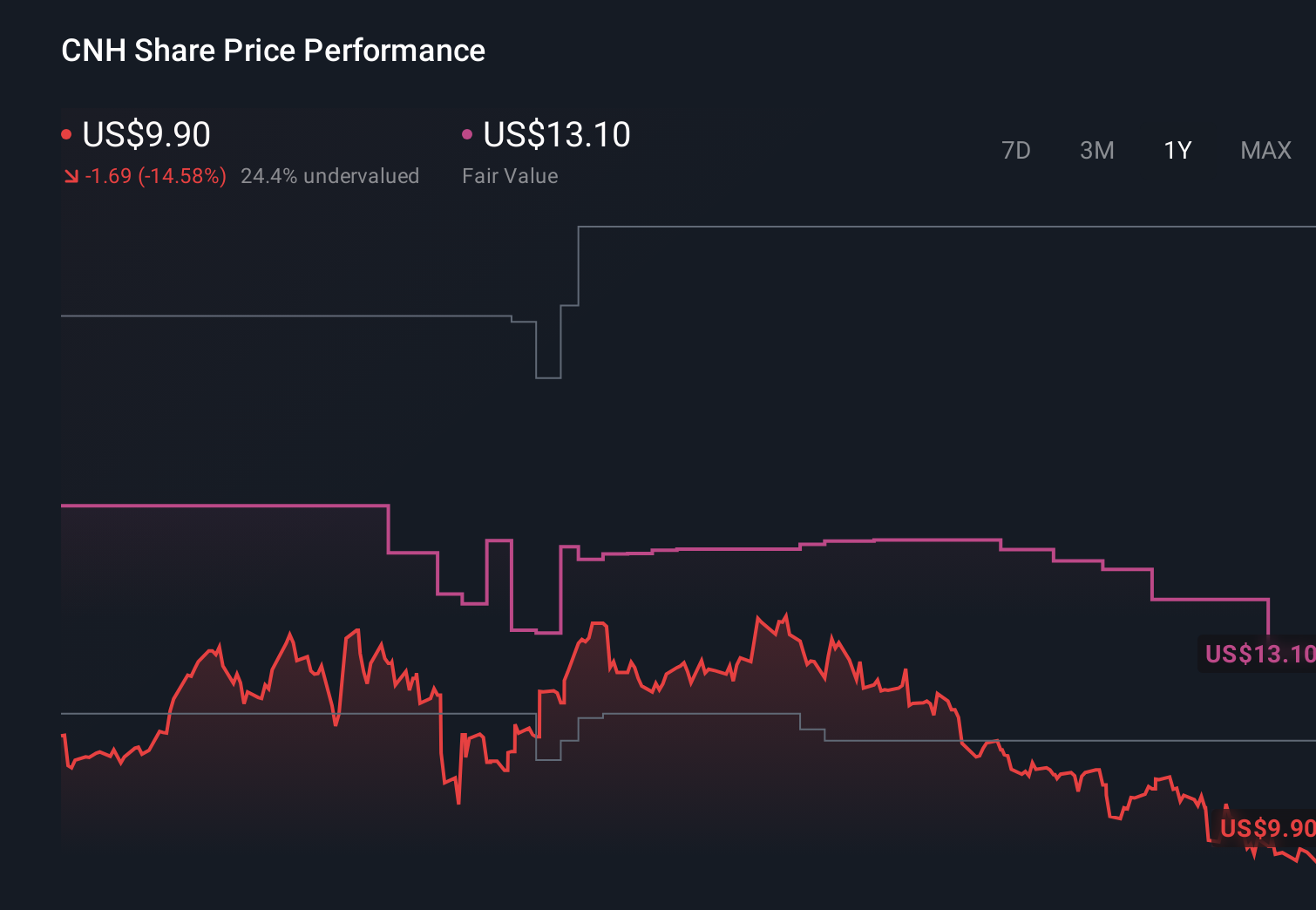

Uncover how CNH Industrial's forecasts yield a $13.88 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were previously modeling revenue of about US$23.3 billion and earnings near US$2.3 billion, so if you lean toward that more upbeat view, it is worth asking how Q1’s weak profit and the risk of escalating trade barriers might push those expectations closer to, or further from, reality.

Explore 6 other fair value estimates on CNH Industrial - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CNH Industrial research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CNH Industrial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CNH Industrial's overall financial health at a glance.

Contemplating Other Strategies?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- Outshine the giants: these 17 early-stage AI stocks could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com