- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Manchester United (NYSE:MANU) Valuation Check As Recent Share Gains Meet Mixed Pricing Signals

Recent share performance snapshot

Manchester United (NYSE:MANU) has seen its share price move recently, with a last close of US$18.88. Over the past month and the past 3 months, the stock has recorded total returns of 12.2% and 6.7% respectively.

See our latest analysis for Manchester United.

For context, the recent 1 month share price return of 12.2% and year to date share price return of 19.65% sit alongside a 1 year total shareholder return of 37.11%, while the 3 year total shareholder return of a 2.38% decline shows that momentum has only turned more positive in the shorter term.

If this kind of move has you thinking about what else could be on your radar, it may be worth checking out 18 top founder-led companies

With the shares now at US$18.88 and some metrics suggesting a potential discount to certain value estimates, the key question is whether Manchester United is genuinely undervalued or whether the market is already pricing in future growth.

Preferred Price-to-Sales Ratio of 3.7x: Is it justified?

At a last close of $18.88, Manchester United is trading on a P/S ratio of 3.7x, which screens as expensive relative to both peers and a modelled fair level.

The P/S ratio compares the company’s market value to its annual revenue, so a higher multiple means investors are paying more for each dollar of sales. For a business like Manchester United, where earnings are currently a loss of £9.06m and profitability is still a work in progress, sales-based measures often become a key reference point for how the market is valuing the club’s brand and revenue potential.

Here, the gap is clear. The current 3.7x P/S sits above the peer average of 2.4x and also above the estimated fair P/S ratio of 2.2x. It is also meaningfully higher than the broader US Entertainment industry average of 1.4x. This suggests the market is assigning a premium multiple compared to sector norms, while the fair ratio suggests a level the valuation could move toward if sentiment or assumptions change.

Explore the SWS fair ratio for Manchester United

Result: Price-to-Sales ratio of 3.7x (OVERVALUED)

However, the recent return strength sits alongside a loss of £9.06m and a 3 year total shareholder return decline of 2.38%, which could challenge that premium story.

Find out about the key risks to this Manchester United narrative.

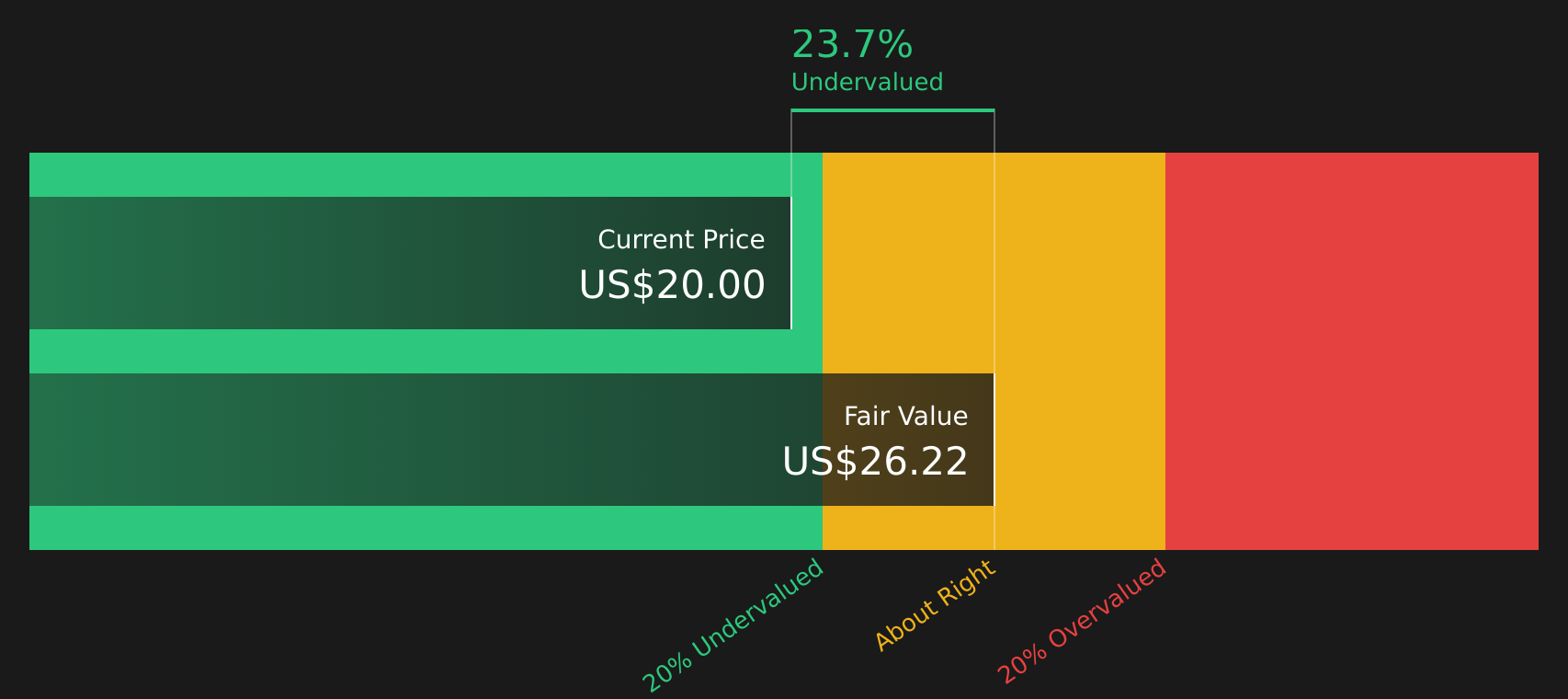

Another view: DCF suggests a different story

While the 3.7x P/S ratio makes Manchester United look expensive on sales, the SWS DCF model points the other way. With the share price at $18.88 versus an estimated future cash flow value of $24.86, the model suggests the stock trades at a 24.1% discount. This raises the question of which signal you trust more.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Manchester United for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value and sentiment can be confusing, so it pays to look at the underlying data yourself and decide how comfortable you are with the current setup. If you want a concise view of both the upside and the concerns flagged by the numbers, start with 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Manchester United has sharpened your focus, do not stop here. Use the Simply Wall St screener to uncover other opportunities that fit your style and risk comfort.

- Target potential bargains by hunting for companies that look mispriced on quality and value using the 51 high quality undervalued stocks.

- Strengthen your income stream by zeroing in on steady payers featured in the 12 dividend fortresses.

- Prioritise resilience by scanning companies highlighted in the 74 resilient stocks with low risk scores before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com