- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Undiscovered Gems: US Stocks To Watch In May 2026

The United States market has experienced a flat performance over the last week, yet it boasts an impressive 29% increase over the past year with earnings projected to grow by 16% annually. In this dynamic environment, identifying stocks that combine strong fundamentals with untapped potential can be key to uncovering promising investment opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.27% | 1.25% | -3.09% | ★★★★★★ |

| Tri-County Financial Group | 54.21% | -0.70% | -10.52% | ★★★★★★ |

| Cashmere Valley Bank | 31.63% | 5.07% | 1.43% | ★★★★★★ |

| Bank of the James Financial Group | 10.99% | 5.54% | 3.94% | ★★★★★★ |

| Sound Financial Bancorp | 16.13% | 0.44% | -12.60% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.53% | 11.34% | ★★★★★★ |

| Union Bankshares | 374.44% | 1.11% | -7.71% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

| Oxford Bank | 12.42% | 14.34% | 4.14% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

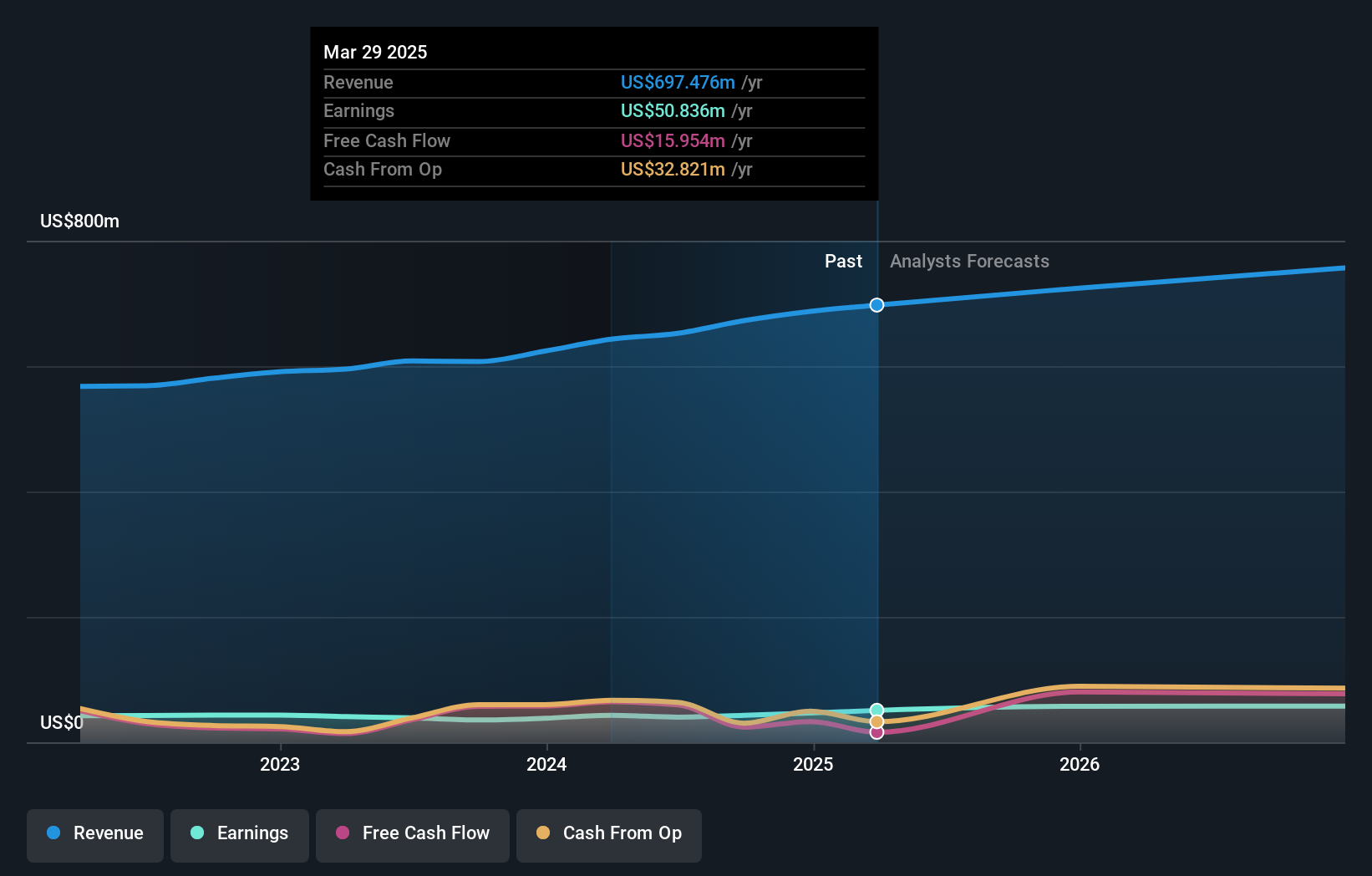

CRA International (CRAI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: CRA International, Inc. offers economic, financial, and management consulting services globally with a market capitalization of $1.01 billion.

Operations: The primary revenue stream for CRA International comes from its professional and consulting services, generating $751.58 million. The company's market capitalization stands at approximately $1.01 billion.

CRA International, a compelling player in the advisory space, is trading at 51.9% below its estimated fair value, offering potential upside for investors. The company's net debt to equity ratio stands at a satisfactory 7.4%, with interest payments well covered by EBIT at 15.5 times coverage. Over the past year, earnings grew by 16.8%, outpacing the Professional Services industry average of 2.9%. Despite challenges like reliance on antitrust work and talent retention issues, CRA's strategic investments in talent and technology position it well to harness opportunities from regulatory complexities and M&A activity surges.

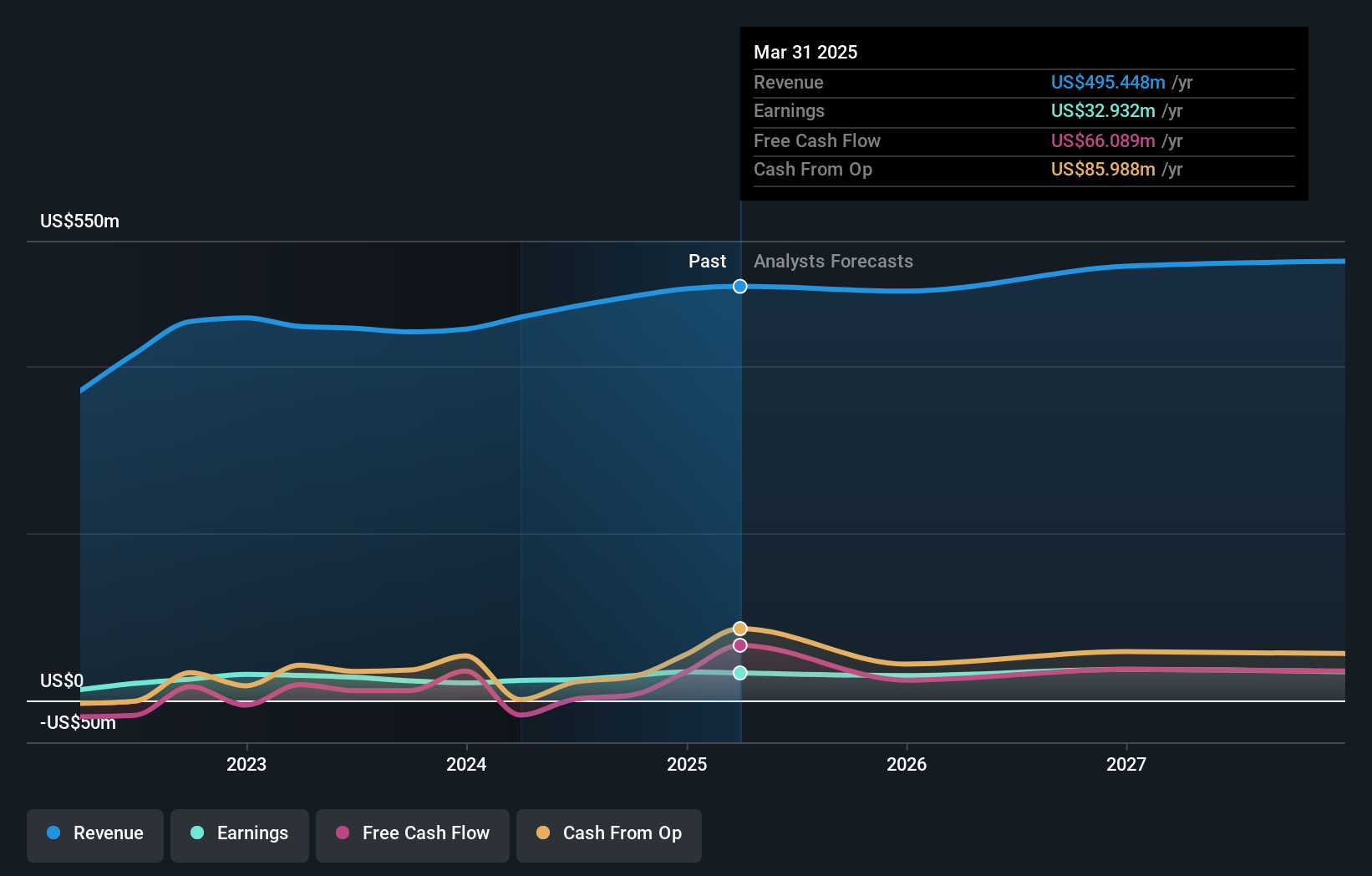

NWPX Infrastructure (NWPX)

Simply Wall St Value Rating: ★★★★★★

Overview: NWPX Infrastructure, Inc. manufactures and sells water-related infrastructure products in the United States and Canada, with a market cap of $828.88 million.

Operations: NWPX Infrastructure generates revenue primarily from the sale of water-related infrastructure products across the United States and Canada. The company's cost structure includes expenses related to manufacturing and distribution, impacting its profitability metrics. Notably, it has demonstrated a net profit margin trend worth observing over recent financial periods.

NWPX Infrastructure, a key player in water infrastructure products across North America and Canada, showcases strong financial health with earnings growth of 27.5% over the past year, outpacing the construction industry average of 26.5%. Its price-to-earnings ratio stands at 22.6x, notably below the industry average of 41.7x, indicating potential value for investors. The company's interest payments are well-covered by EBIT at a multiple of 24.4x, suggesting robust financial management. Despite challenges from shifting funding priorities towards sustainable materials and reliance on government projects, NWPX's solid backlog and federal infrastructure spending hint at future growth opportunities.

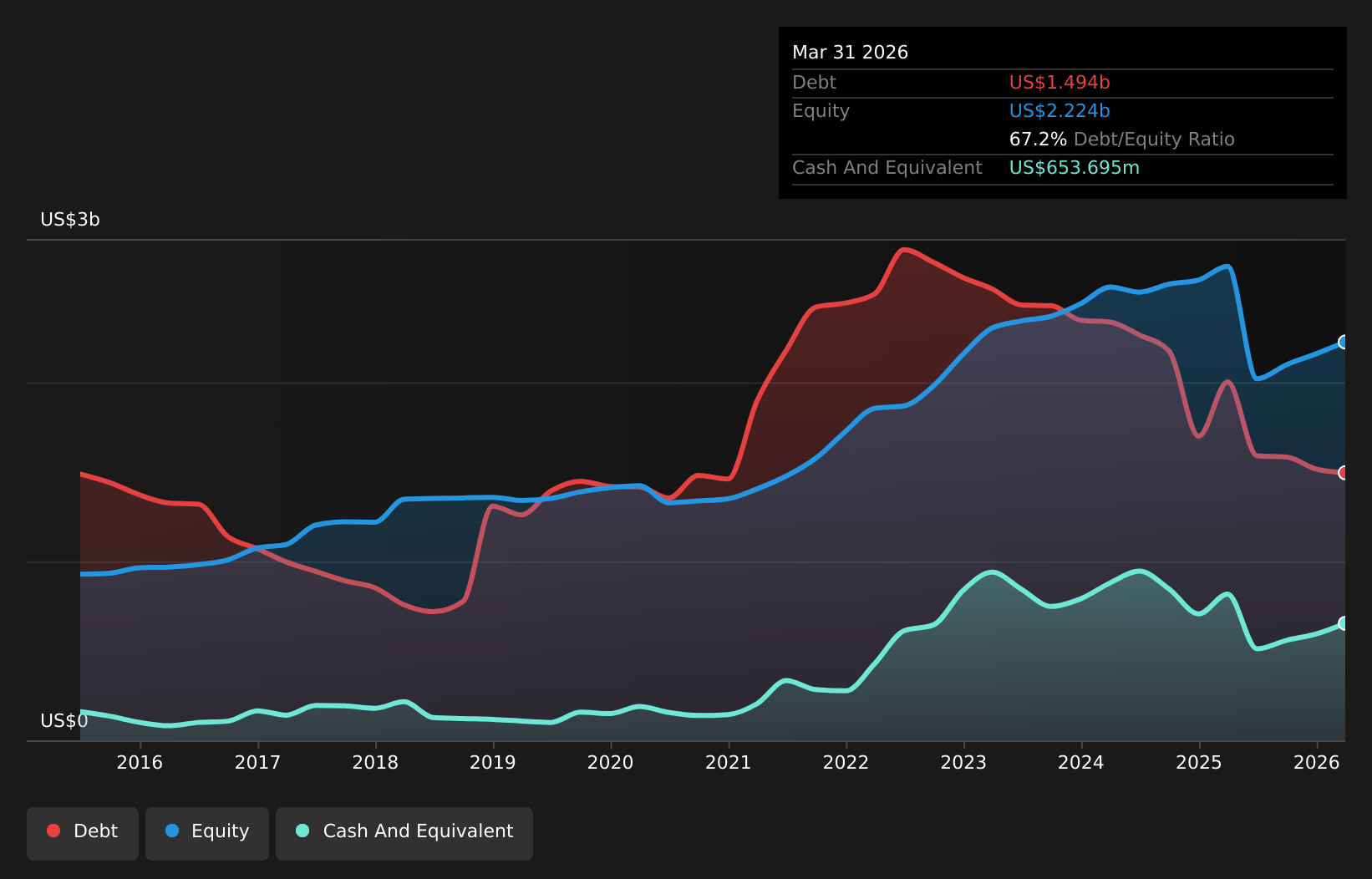

Costamare (CMRE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Costamare Inc. is a global owner and operator of containerships and dry bulk vessels, with a market cap of approximately $1.95 billion.

Operations: Costamare generates revenue primarily through the ownership and operation of containerships and dry bulk vessels. The company has a market cap of approximately $1.95 billion.

Costamare, with its solid footing in the shipping industry, presents a compelling case for investors. Its debt to equity ratio improved significantly from 135% to 67.2% over five years, indicating financial prudence. The company's earnings growth of 16.8% last year outpaced the industry's -6.6%, showcasing resilience and strong management execution. Despite a lower price-to-earnings ratio of 5.9x compared to the US market's average of 19.3x, Costamare faces challenges ahead with projected earnings declines averaging 16.2% annually over three years due to potential shifts in trade patterns and regulatory landscapes impacting margins and operations costs.

Where To Now?

- Take a closer look at our US Undiscovered Gems With Strong Fundamentals list of 335 companies by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com