- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

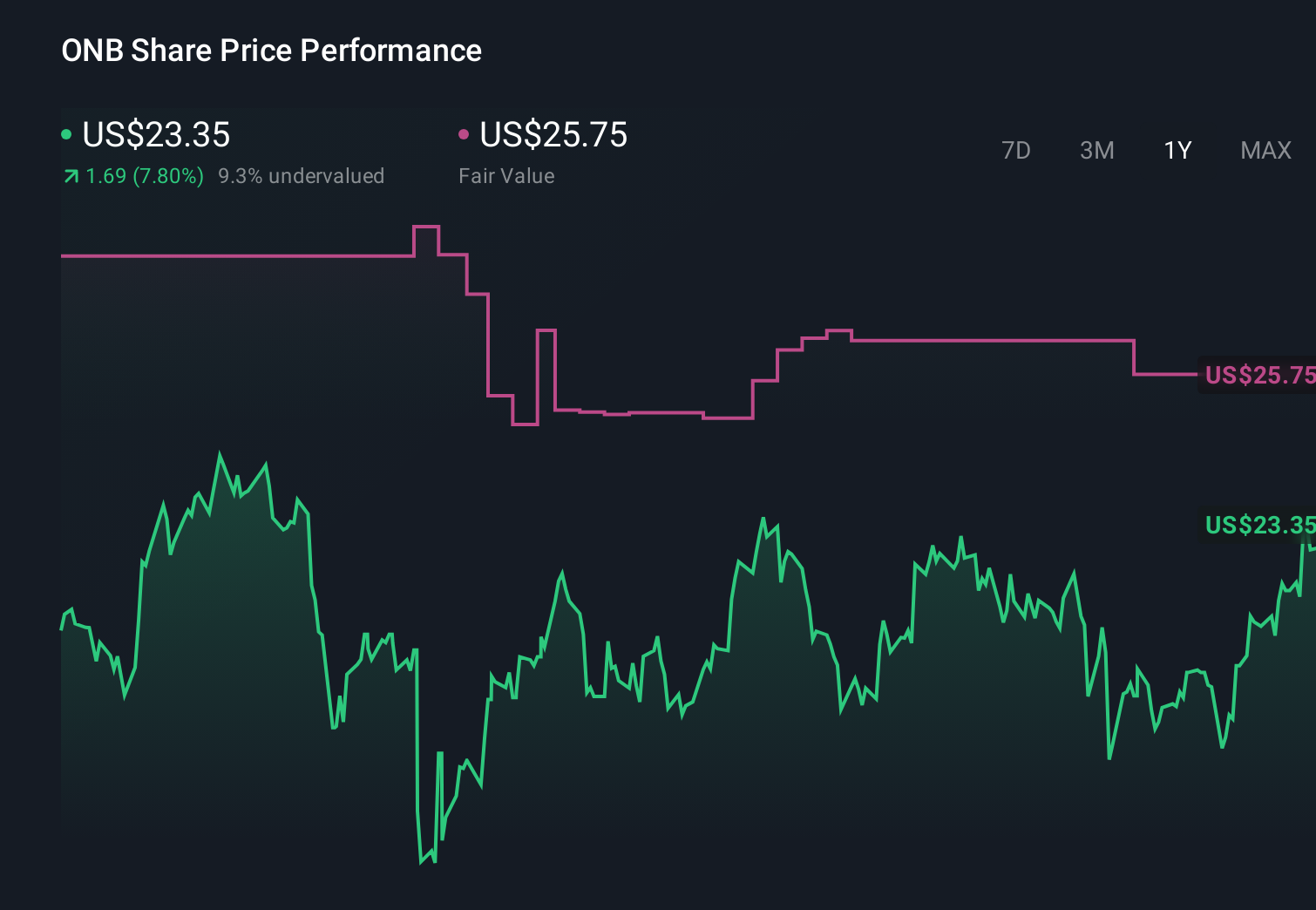

Will Stronger Net Interest Income And Buybacks Shift Old National Bancorp's (ONB) Narrative

- In April 2026, Old National Bancorp reported first-quarter 2026 results showing net interest income of US$572.57 million, net income of US$233.67 million, diluted EPS of US$0.59, and net charge-offs of US$32.00 million.

- The company also disclosed that, while it recorded no share repurchases under its new 2026 authorization through March 31, it had previously completed repurchasing 6,136,609 shares for US$143.63 million under its 2025 program, highlighting ongoing use of capital management tools alongside improving profitability.

- With first-quarter earnings showing substantially higher net interest income, we’ll now examine how this result may influence Old National Bancorp’s investment narrative.

Find 51 companies with promising cash flow potential yet trading below their fair value.

Old National Bancorp Investment Narrative Recap

To own Old National Bancorp, you need to believe it can turn its enlarged Midwest footprint and fee businesses into resilient earnings while managing its commercial real estate risk. The latest quarter’s stronger net interest income and higher net income support that earnings side, but the US$32.00 million in net charge-offs keeps credit quality, especially in CRE, in focus as a key short term risk. Overall, the impact of this quarter on that risk appears incremental rather than transformational.

The recent update on share repurchases, showing 6,136,609 shares bought back for US$143.63 million under the 2025 program, ties directly into the near term earnings catalyst by concentrating results across a smaller share base. Paired with higher net interest income and EPS of US$0.59 in the first quarter of 2026, this capital return activity reinforces how much of the current investment case rests on sustained profitability and disciplined balance sheet management.

Yet even with stronger earnings and buybacks, investors still need to keep an eye on Old National Bancorp’s exposure to commercial real estate, because...

Read the full narrative on Old National Bancorp (it's free!)

Old National Bancorp's narrative projects $3.4 billion revenue and $1.4 billion earnings by 2029. This requires 10.6% yearly revenue growth and a $657.9 million earnings increase from $742.1 million today.

Uncover how Old National Bancorp's forecasts yield a $27.91 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community span from about US$27.91 up to over US$12,000, showing how far apart individual views can be. Against that backdrop, the recent jump in net interest income alongside rising net charge offs gives you concrete results to weigh as you explore these different perspectives on Old National Bancorp’s future performance.

Explore 3 other fair value estimates on Old National Bancorp - why the stock might be worth just $27.91!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Old National Bancorp research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Old National Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Old National Bancorp's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com