- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

3 Promising Penny Stocks With Market Caps Below $300M

Over the last 7 days, the United States market has remained flat, but it is up 29% over the past year with earnings forecasted to grow by 16% annually. For investors willing to explore beyond well-known companies, penny stocks—typically smaller or newer firms—can offer intriguing opportunities. Despite being an outdated term, penny stocks still represent a viable investment area, especially when focusing on those with strong financials and growth potential.

Top 10 Penny Stocks In The United States

| Name | Share Price | Market Cap | Rewards & Risks |

| WM Technology (MAPS) | $0.33 | $65.58M | ✅ 3 ⚠️ 5 View Analysis > |

| LexinFintech Holdings (LX) | $2.105 | $354.19M | ✅ 3 ⚠️ 2 View Analysis > |

| Information Services Group (III) | $3.11 | $194.03M | ✅ 3 ⚠️ 1 View Analysis > |

| Golden Growers Cooperative (GGRO.U) | $5.00 | $77.45M | ✅ 2 ⚠️ 5 View Analysis > |

| Niagen Bioscience (NAGE) | $4.845 | $388.8M | ✅ 3 ⚠️ 1 View Analysis > |

| Cricut (CRCT) | $4.405 | $924.6M | ✅ 2 ⚠️ 2 View Analysis > |

| Village Farms International (VFF) | $2.80 | $332.65M | ✅ 5 ⚠️ 1 View Analysis > |

| SIGA Technologies (SIGA) | $7.80 | $326.7M | ✅ 2 ⚠️ 1 View Analysis > |

| BAB (BABB) | $0.907475 | $6.61M | ✅ 2 ⚠️ 3 View Analysis > |

| Marine Petroleum Trust (MARP.S) | $4.90 | $9.82M | ✅ 2 ⚠️ 4 View Analysis > |

Click here to see the full list of 346 stocks from our US Penny Stocks screener.

We'll examine a selection from our screener results.

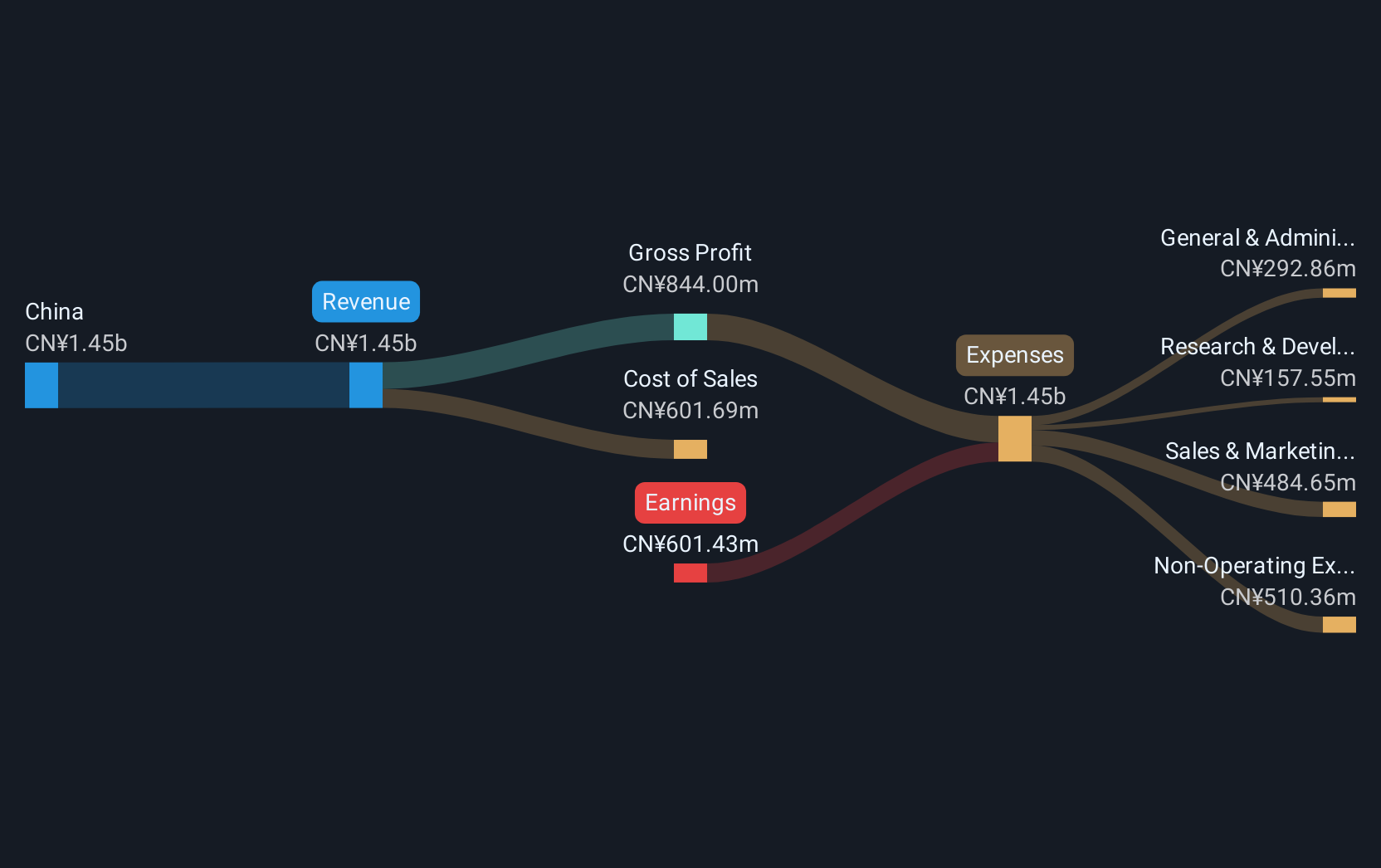

So-Young International (SY)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: So-Young International Inc. operates an online platform for consumption healthcare services in the People's Republic of China, with a market cap of $276.82 million.

Operations: The company does not report distinct revenue segments.

Market Cap: $276.82M

So-Young International Inc. has shown revenue growth, reporting CNY 460.72 million for Q4 2025, up from CNY 369.21 million the previous year, yet remains unprofitable with a net loss of CNY 108.85 million for the quarter. The company has reduced its impairment charges significantly and extended its buyback plan until March 2027. With a seasoned management team and board, So-Young maintains more cash than debt, supporting short-term liabilities effectively with CN¥1.5 billion in assets against CN¥784.1 million in liabilities, positioning it as a potentially undervalued stock trading below fair value estimates despite ongoing challenges.

- Click here and access our complete financial health analysis report to understand the dynamics of So-Young International.

- Learn about So-Young International's future growth trajectory here.

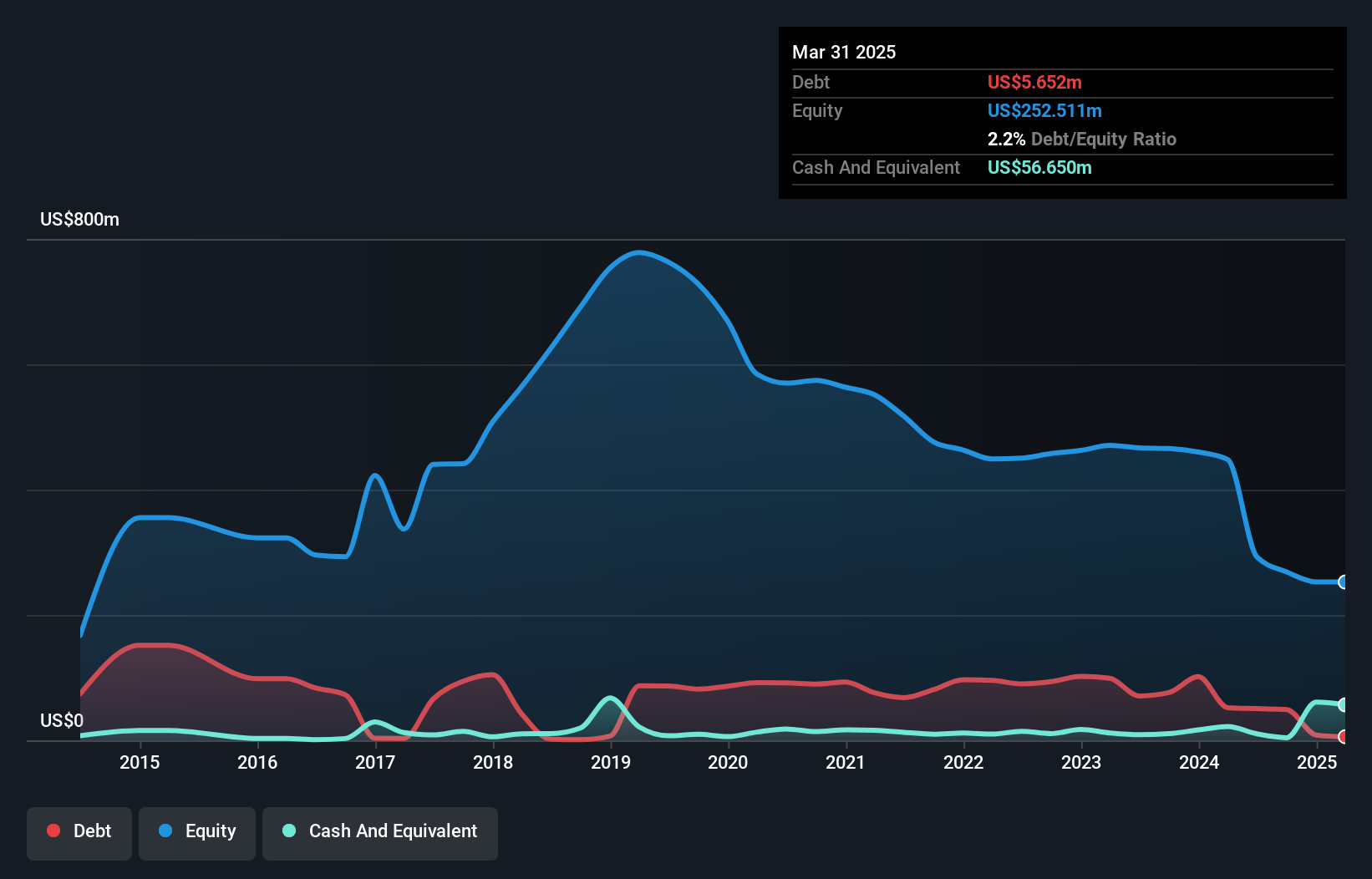

Mammoth Energy Services (TUSK)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Mammoth Energy Services, Inc. is an energy services company operating in the United States, Canada, and internationally with a market cap of $136.85 million.

Operations: The company's revenue is primarily derived from its Sand segment at $16.55 million, followed by Rentals at $11.10 million, Accommodations at $8.95 million, Infrastructure at $4.09 million, and Drilling services contributing $3.68 million.

Market Cap: $136.85M

Mammoth Energy Services, Inc. reported a revenue of US$44.29 million for 2025, slightly down from the previous year, yet achieved a net income of US$4.6 million compared to a significant loss previously. Despite being unprofitable over five years with declining earnings by 14.9% annually, its short-term assets of US$177.1 million comfortably cover liabilities and exceed long-term obligations, while maintaining more cash than debt suggests financial stability amidst volatility concerns. The management team is relatively new with less than one year average tenure; however, the experienced board may provide strategic oversight as the company navigates its challenges in the energy sector.

- Dive into the specifics of Mammoth Energy Services here with our thorough balance sheet health report.

- Assess Mammoth Energy Services' previous results with our detailed historical performance reports.

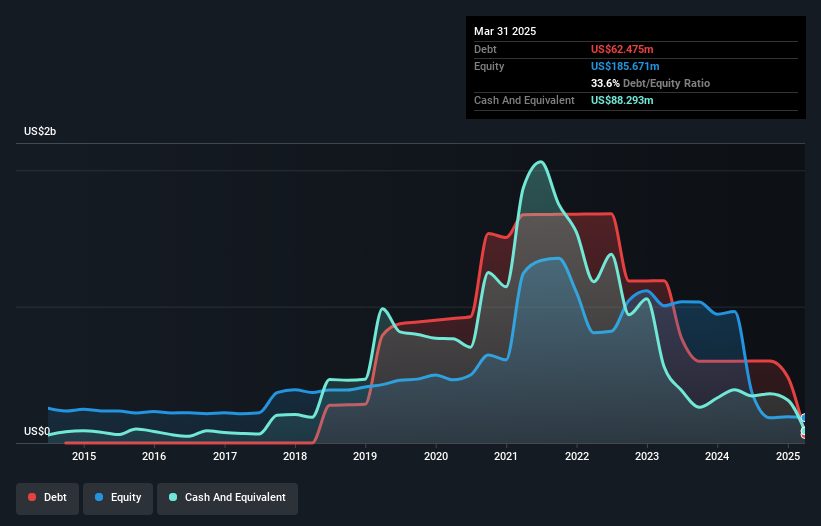

Chegg (CHGG)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Chegg, Inc. operates a learning platform that offers skill development for businesses and lifelong learners, with a market cap of approximately $117.39 million.

Operations: The company generates revenue from its Educational Services segment, specifically within Education & Training Services, totaling $376.91 million.

Market Cap: $117.39M

Chegg, Inc., with a market cap of US$117.39 million, faces challenges typical of penny stocks, such as high volatility and unprofitability. Despite generating US$376.91 million in revenue from its Educational Services segment, the company reported a net loss for 2025 and is not projected to be profitable soon. Recent strategic moves include a proposed reverse stock split and changes in auditors to Grant Thornton LLP. Activist investor Galloway Capital Partners' acquisition of a 5.44% stake suggests potential restructuring for shareholder value enhancement amidst industry disruptions and ongoing financial pressures.

- Navigate through the intricacies of Chegg with our comprehensive balance sheet health report here.

- Gain insights into Chegg's outlook and expected performance with our report on the company's earnings estimates.

Key Takeaways

- Unlock more gems! Our US Penny Stocks screener has unearthed 343 more companies for you to explore.Click here to unveil our expertly curated list of 346 US Penny Stocks.

- Seeking Other Investments? We've found 16 US stocks that are forecast to pay a dividend yeild of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com