- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Enterprise Financial Services (EFSC) Valuation After Q1 2026 Beat And Dividend Increase

Enterprise Financial Services (EFSC) drew fresh attention after Q1 2026 results and a higher common dividend, with earnings slightly above consensus and management emphasizing stable margins, asset quality progress, and continued balance sheet and deposit growth.

See our latest analysis for Enterprise Financial Services.

The latest Q1 results and dividend increase come as the share price trades at US$58.83, with an 8.3% 1 month share price return and a 17.2% 1 year total shareholder return. This suggests momentum has been building rather than fading.

If you are looking beyond regional banks, this could be a good moment to broaden your search and uncover 1 top founder-led companies

With Q1 earnings slightly ahead of expectations, a higher common dividend, and the share price still below the published analyst target, the key question now is whether EFSC is undervalued or whether the market is already accounting for potential future growth.

Price to Earnings of 10.9x: Is it justified?

On a simple valuation check, Enterprise Financial Services is trading on a P/E of 10.9x, while peers sit closer to 12.7x and the wider US Banks industry at 11.7x.

The P/E multiple compares the current share price to the company’s earnings per share and is a common way investors weigh what they are paying for each dollar of profit in the banking sector. With EFSC also screened as high quality earnings, a lower P/E than peers can indicate the market is pricing its profit stream more cautiously than the group.

Compared to the estimated fair P/E of 11x, the current 10.9x level is very close to the mark, while still sitting at a discount to both peer and industry averages. If market expectations shift closer to the fair ratio and peer levels, the valuation could converge toward that range.

Explore the SWS fair ratio for Enterprise Financial Services

Result: Price-to-Earnings of 10.9x (UNDERVALUED)

DCF valuation points to a wide gap

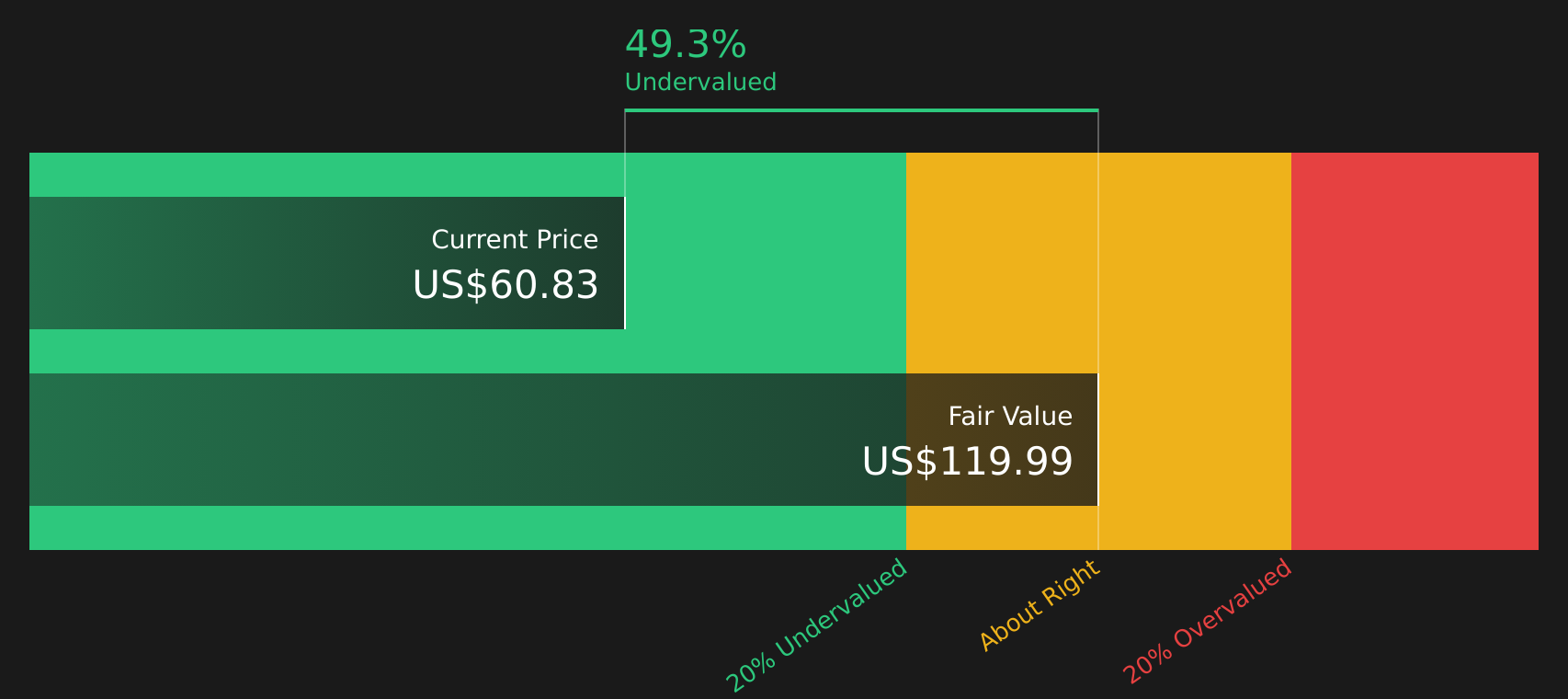

Alongside the P/E cross check, the SWS DCF model currently values EFSC at a fair value of $124.59 per share, versus the recent close at $58.83. That points to a large discount based on projected future cash flows.

The DCF framework estimates the present value of the cash EFSC is expected to generate in the future and discounts those amounts back using a required rate of return. For a regional bank with positive earnings, a history of earnings growth and a 2.31% dividend, this approach puts more weight on the durability of cash generation and less on short term market swings.

Look into how the SWS DCF model arrives at its fair value.

However, higher interest costs or a turn in credit quality could quickly challenge current assumptions about EFSC’s earnings power and the valuation gap that exists today.

Find out about the key risks to this Enterprise Financial Services narrative.

Another angle on value

The SWS DCF model paints a very different picture, with an estimated fair value of $124.59 per share versus the current $58.83, implying EFSC is deeply undervalued. That is a much bigger gap than the modest P/E discount, so which signal should matter more for you right now?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Enterprise Financial Services for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 1 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of valuation signals and optimistic rewards may leave you with questions, so take a closer look at the details and pressure test the thesis for yourself. To see which positives are already on the radar and decide whether they fit your own expectations, review the 5 key rewards

Looking for more investment ideas?

If EFSC sparks your interest, do not stop there. Broaden your watchlist now, or you risk missing other opportunities that fit your style and goals.

- Target steady paychecks by checking out income ideas through the 13 dividend fortresses that focus on higher yielding companies.

- Hunt for potential bargains using the screener containing 1 high quality undiscovered gems that zeroes in on strong businesses the market may be overlooking.

- Put resilience first by scanning the 72 resilient stocks with low risk scores that highlights companies with lower risk profiles and more robust fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com