- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Dividend Hike And New Buyback Might Change The Case For Investing In F.N.B (FNB)

- In April 2026, F.N.B. Corporation reported first-quarter results showing year-over-year growth in net interest income to US$359.28 million and net income to US$137.05 million, modestly higher net charge-offs of US$15.9 million, largely unchanged full-year 2026 net interest income guidance of US$1.495–1.535 billion, and second-quarter guidance of US$370–380 million.

- Alongside these results, the board raised the quarterly dividend to US$0.13 per share and backed a new US$250 million buyback program, following completion of a prior US$248.9 million authorization, underscoring management’s emphasis on returning capital to shareholders.

- We’ll now consider how the dividend increase and expanded US$250 million share repurchase authorization may influence F.N.B.’s investment narrative.

The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

F.N.B Investment Narrative Recap

To own F.N.B., you have to be comfortable with a regional bank that leans on steady net interest income and disciplined credit costs, while investing heavily in digital banking. The latest quarter’s higher net interest income and reaffirmed 2026 guidance support that view in the near term, though the uptick in net charge offs keeps credit quality as the key short term swing factor and a central risk to watch.

The most relevant development here is the board’s move to raise the quarterly dividend to US$0.13 per share and approve a new US$250 million buyback authorization. For investors focused on capital return, those actions sit alongside net interest income guidance as important markers for how much balance sheet flexibility F.N.B. has while still managing regional concentration, technology spending and credit risk.

Yet even with these capital returns, investors should be aware that F.N.B.’s exposure to commercial real estate, in particular...

Read the full narrative on F.N.B (it's free!)

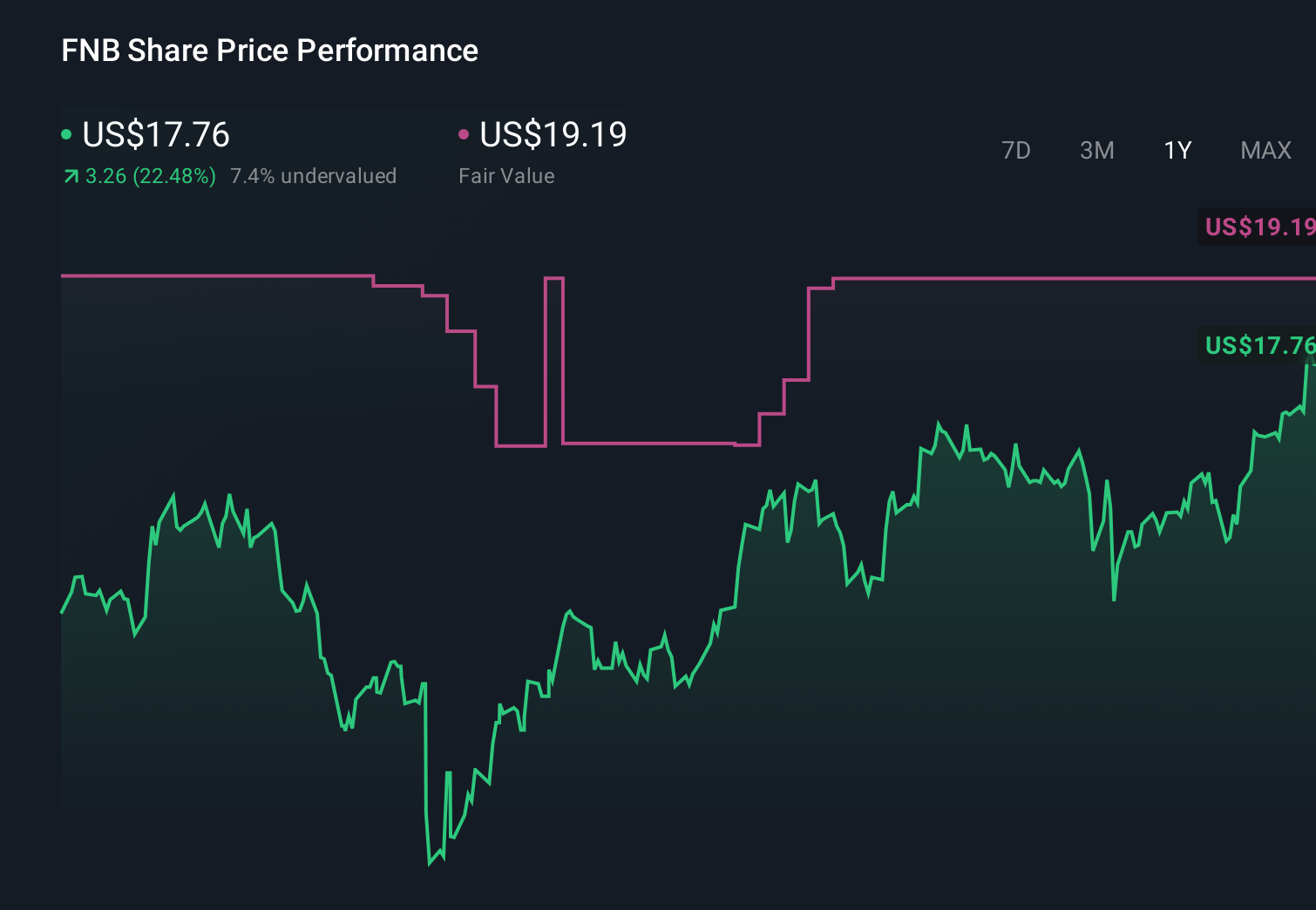

F.N.B's narrative projects $2.3 billion revenue and $760.6 million earnings by 2029.

Uncover how F.N.B's forecasts yield a $20.38 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community currently see F.N.B.’s fair value between US$20.38 and US$63.31, underscoring how far opinions can spread. As you weigh those views, keep in mind that recent net charge offs and regional credit trends could matter just as much as any model output, so it is worth exploring several different angles on the business.

Explore 3 other fair value estimates on F.N.B - why the stock might be worth over 3x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your F.N.B research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free F.N.B research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate F.N.B's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com