- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Willis Towers Watson’s New Data Center Insurance Deepening Its Digital Moat or Stretching Focus (WTW)?

- In early April 2026, Willis, a WTW business, launched Digital Infrastructure Protector, an end-to-end lifecycle insurance and risk solution for data center owners and operators, offering integrated construction and operations coverage with more than US$3 billion in capacity through collaboration with Zurich.

- The solution’s combination of customized policy wording, evidence-based broking, and access to WTW’s Global Digital Infrastructure Group highlights how the firm is tailoring risk management to increasingly complex digital infrastructure needs worldwide.

- We’ll now examine how this new Digital Infrastructure Protector offering could influence Willis Towers Watson’s investment narrative and long-term positioning.

This technology could replace computers: discover 25 stocks that are working to make quantum computing a reality.

Willis Towers Watson Investment Narrative Recap

To own Willis Towers Watson, you need to believe it can keep carving out higher value, specialized advisory and risk solutions while managing fee pressure and intense competition. The Digital Infrastructure Protector launch fits that thesis by targeting complex data center risks, but it does not materially change the near term focus on upcoming Q1 2026 results as a key catalyst or the risk that AI and automation could compress pricing for its core services.

Among recent announcements, the creation of WTW’s Global Digital Infrastructure Group in February 2026 is especially relevant, as it underpins the new Protector product with cross sector expertise. Together, that specialized talent base and the Zurich collaboration suggest WTW is leaning harder into complex, higher margin niches such as digital infrastructure, which aligns closely with the catalyst of increased demand for advanced risk management and consulting solutions.

Yet behind this push into digital infrastructure, investors still need to be aware of how accelerating AI driven automation could...

Read the full narrative on Willis Towers Watson (it's free!)

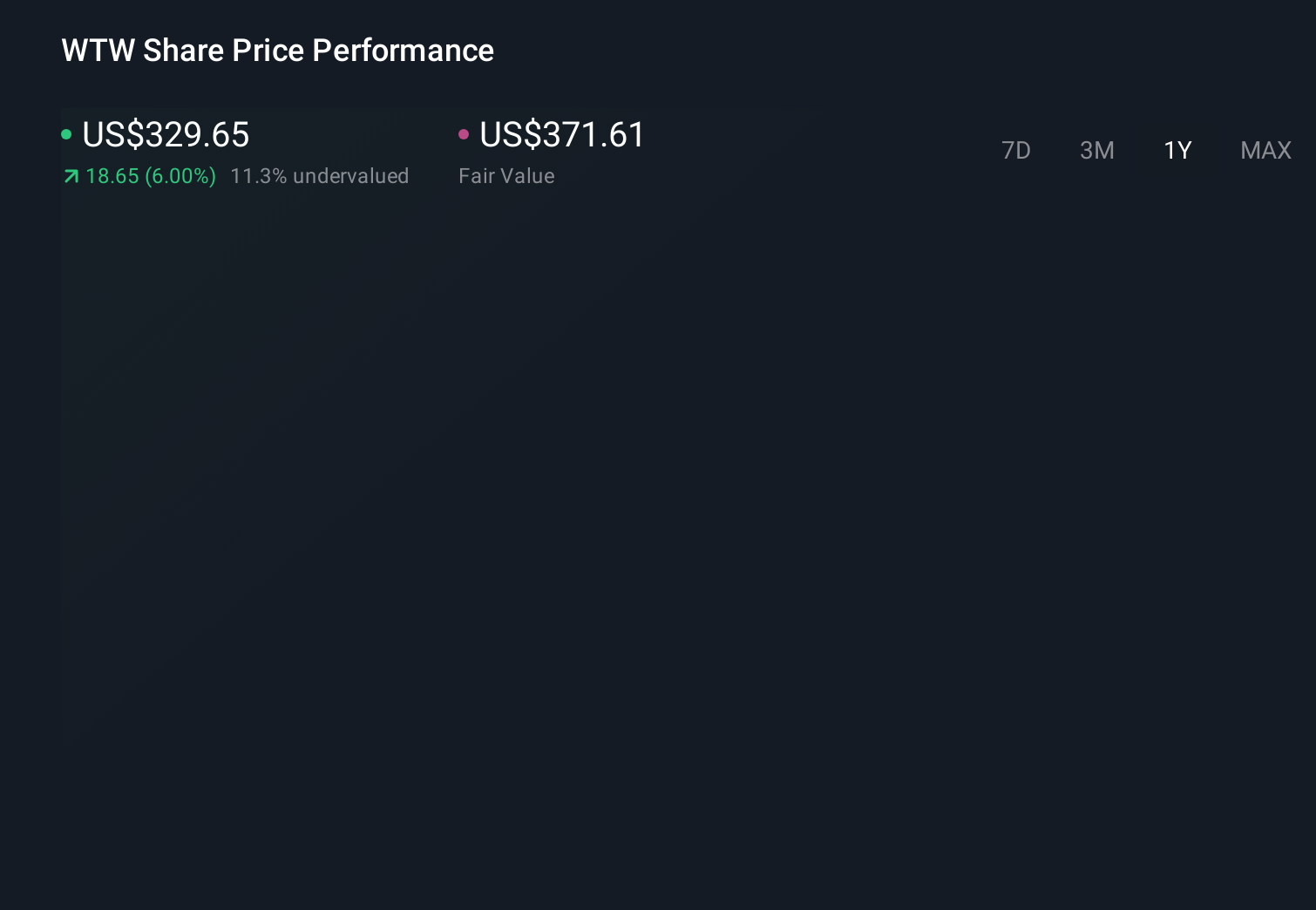

Willis Towers Watson's narrative projects $11.9 billion revenue and $1.8 billion earnings by 2029. This requires 6.9% yearly revenue growth and a $0.2 billion earnings increase from $1.6 billion today.

Uncover how Willis Towers Watson's forecasts yield a $370.63 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have only two fair value estimates for WTW, spanning a wide US$186.63 to US$370.63 per share. Readers should weigh these against the risk that AI fueled commoditization of broking and consulting could pressure WTW’s pricing power and long term profitability.

Explore 2 other fair value estimates on Willis Towers Watson - why the stock might be worth 37% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Willis Towers Watson research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Willis Towers Watson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Willis Towers Watson's overall financial health at a glance.

No Opportunity In Willis Towers Watson?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com