- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

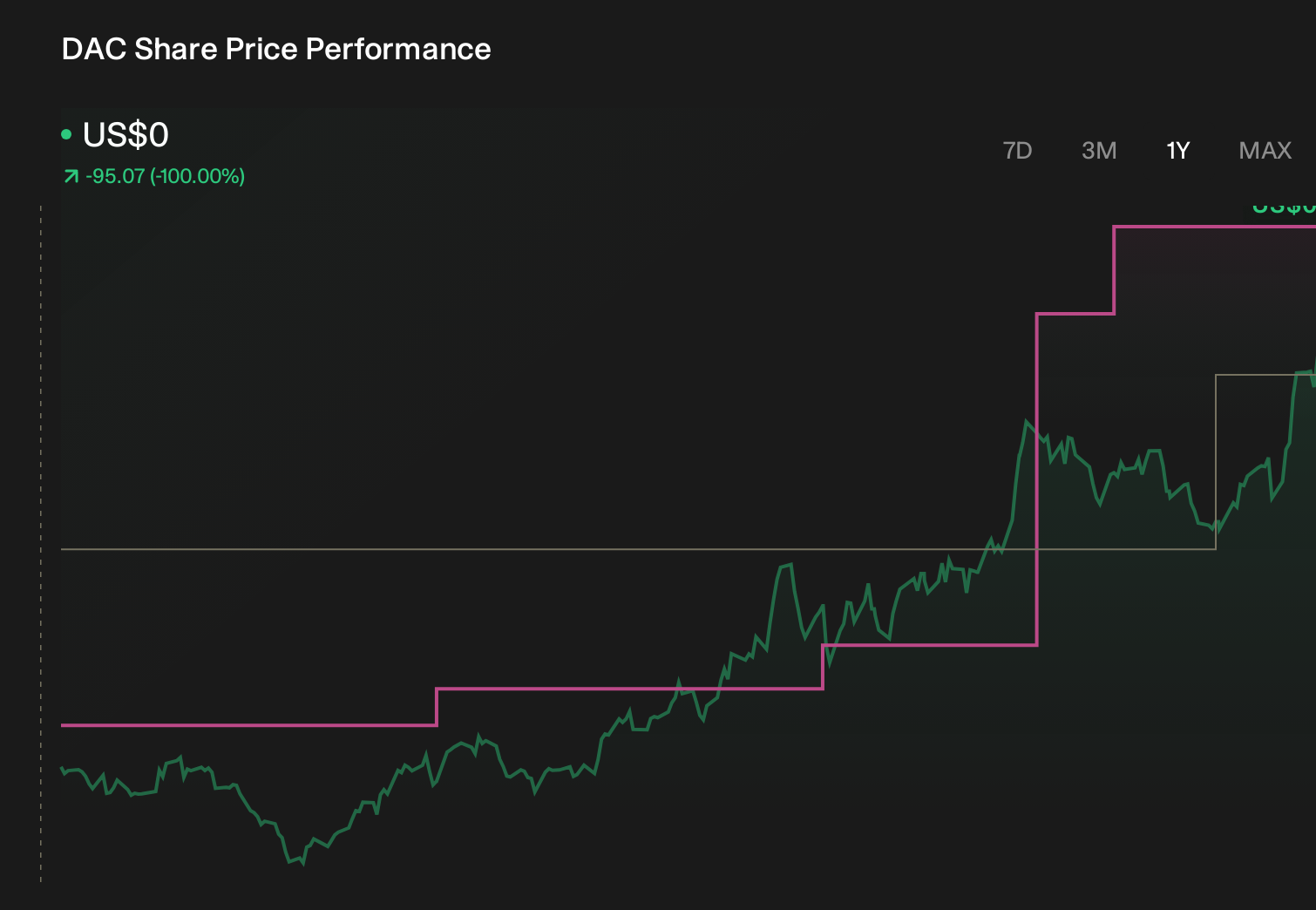

How Investors May Respond To Danaos (DAC) Beating Profit And Revenue Expectations In Q4 Earnings

- In February 2026, Danaos Corporation reported earnings per share of 7.14 and revenue of US$266.26 million, both ahead of analyst expectations.

- The twin surprises in profit and sales highlight how Danaos’s containership fleet is currently converting charter demand into stronger-than-forecast financial results.

- With this earnings beat as a backdrop, we’ll now examine how stronger-than-expected profitability reshapes Danaos’s existing investment narrative.

AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Danaos Investment Narrative Recap

To own Danaos, you need to believe its contracted charter backlog and focus on larger, fuel efficient containerships can keep earnings resilient, even as shipping cycles shift. The recent EPS and revenue beat reinforces that near term, the key catalyst remains the company’s ability to convert its high charter coverage into solid cash flows, while the main risk is that weaker freight and charter markets eventually pressure renewal rates and vessel values. For now, this report does not materially change that trade off.

The most relevant recent announcement alongside this earnings surprise is Danaos’s ongoing share buyback program, which has retired over 3.2 million shares since 2022 under a US$300 million authorization. In the context of strong recent profitability, continued repurchases tighten the share count at a time when the market is grappling with forecasts of declining revenue and earnings over the coming years, amplifying both the upside from sustained cash generation and the downside if shipping conditions soften faster than expected.

Yet behind the solid backlog and active buybacks, one risk investors should be aware of is what happens when current long term charters start to roll off and...

Read the full narrative on Danaos (it's free!)

Danaos' narrative projects $892.0 million revenue and $234.0 million earnings by 2029.

Uncover how Danaos' forecasts yield a $109.00 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members see Danaos’s fair value between US$109 and about US$224 per share, across 2 individual estimates. Against that wide range, the recent earnings beat and heavy charter coverage remind you that differing views on future contract renewals and shipping demand can materially change how you think about the company’s longer term earnings power, so it is worth weighing several perspectives before deciding how this fits into your portfolio.

Explore 2 other fair value estimates on Danaos - why the stock might be worth as much as 95% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Danaos research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Danaos research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Danaos' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 21 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com