- LIVE QUOTES

- LEARN

- HELP

EN

Boot Barn Holdings (BOOT) Is Up 14.8% After Raised Guidance And Upgrades From Jefferies And BofA

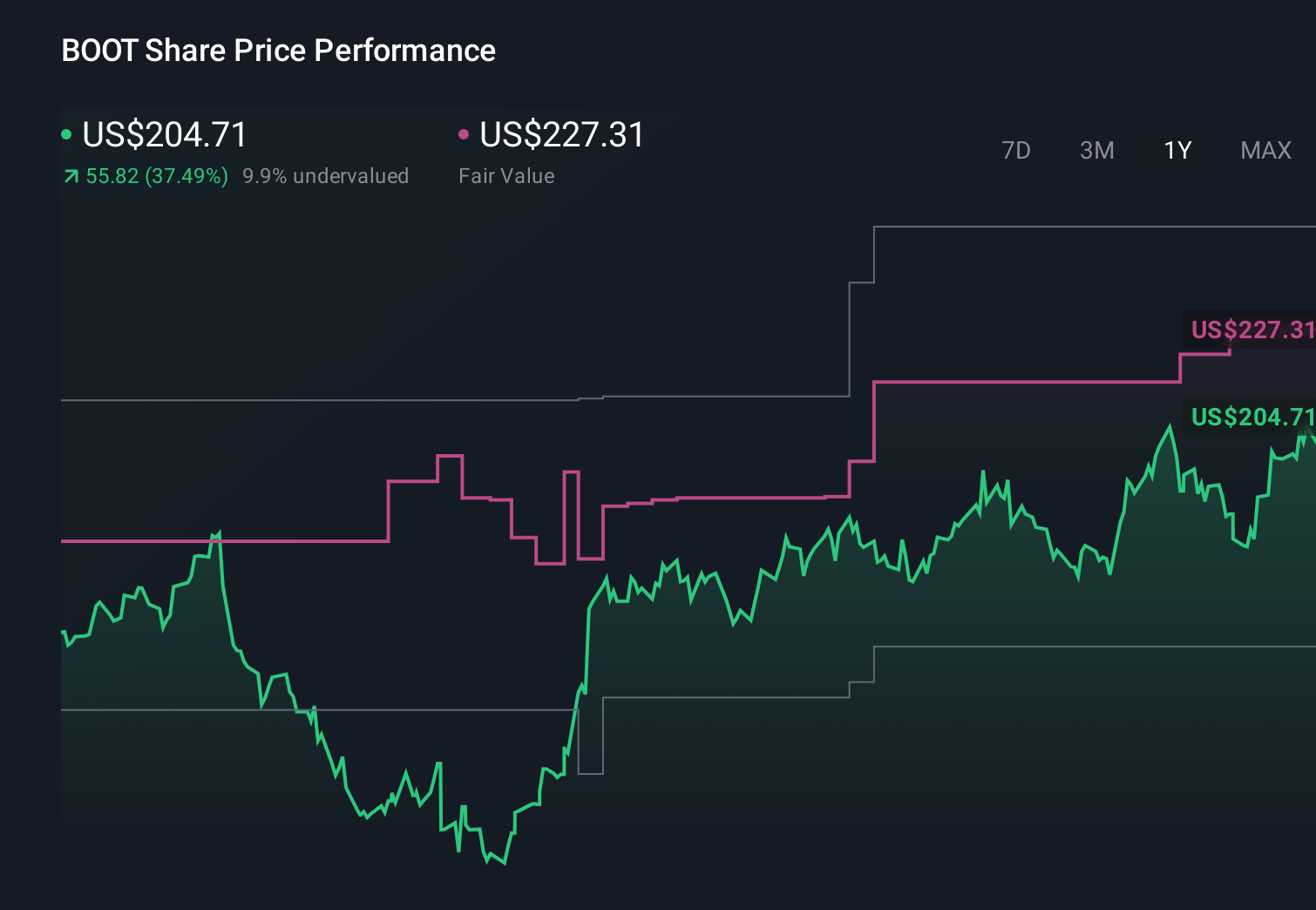

- In early April 2026, Boot Barn Holdings reported strong fiscal third-quarter results and raised its fiscal 2026 sales and EPS guidance, while analysts highlighted the potential impact of higher oil-driven production and shipping costs on its margins later this year.

- The company also drew fresh attention from Wall Street as Jefferies upgraded its rating and Bank of America added Boot Barn to its “Top 10 US Ideas” list, reflecting growing confidence in its store expansion, brand positioning, and balance sheet strength despite broader cost and macro concerns.

- With Jefferies’ upgrade spotlighting resilient sales and store growth, we’ll now examine how this news reshapes Boot Barn’s investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

Boot Barn Holdings Investment Narrative Recap

To own Boot Barn, you need to believe its store expansion, western and workwear focus, and growing omni-channel presence can keep driving results without overreaching. The latest guidance raise supports that store led growth remains the main near term catalyst, while the jump in oil linked production and shipping costs sharpens the biggest short term risk to margins, especially if Boot Barn cannot pass those costs on to customers.

The most relevant update here is the higher fiscal 2026 sales and EPS guidance to US$2.24–US$2.25 billion and US$7.25–US$7.35 per share. That outlook underpins the store expansion and exclusive brand catalysts investors are watching, but may need to be revisited if oil driven cost pressures persist and begin to bite into the gross margin improvement story later in the year.

Yet beneath the upbeat guidance and analyst upgrades, investors should also be aware of the growing risk that higher input and freight costs could...

Read the full narrative on Boot Barn Holdings (it's free!)

Boot Barn Holdings' narrative projects $3.2 billion revenue and $349.8 million earnings by 2029. This requires 13.7% yearly revenue growth and about a $130.8 million earnings increase from $219.0 million today.

Uncover how Boot Barn Holdings' forecasts yield a $237.14 fair value, a 53% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$2.8 billion with higher margins by 2028, so this oil related cost risk may force you to rethink whether that upside story still holds or if the reality could turn out quite differently.

Explore 3 other fair value estimates on Boot Barn Holdings - why the stock might be worth as much as 79% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Boot Barn Holdings research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Boot Barn Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boot Barn Holdings' overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com