- LIVE QUOTES

- LEARN

- HELP

EN

Assessing Northrop Grumman (NOC) Valuation After Recent Share Price Weakness

Why Northrop Grumman Is Drawing Fresh Investor Attention

Northrop Grumman (NOC) is back on many watchlists after recent trading weakness, with the stock showing a 2.4% one-day decline and a 4.1% pullback over the past week despite solid long-term returns.

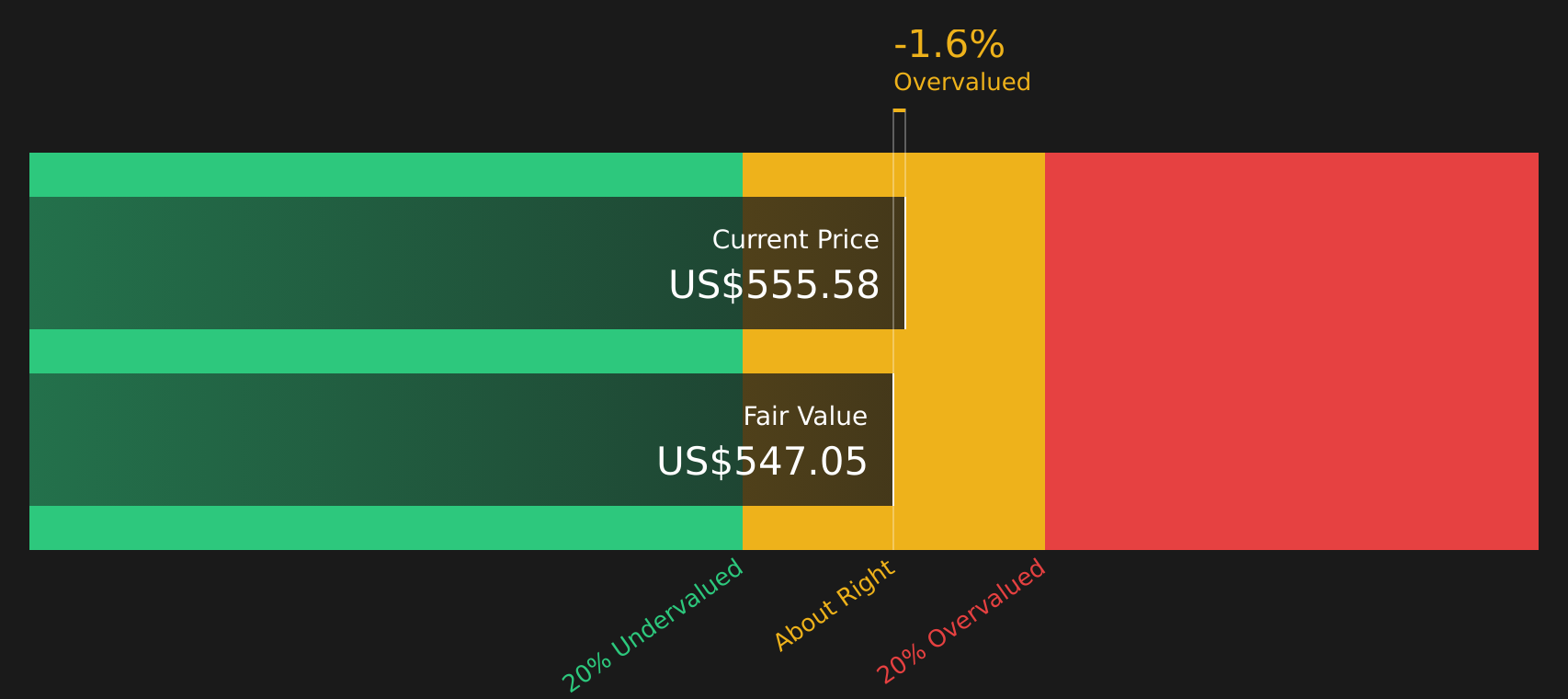

See our latest analysis for Northrop Grumman.

Despite the recent 8.2% 30 day share price decline and this week’s pullback, Northrop Grumman still sits at US$673.73, with a year to date share price return of 15.0% and a 1 year total shareholder return of 28.2%, suggesting momentum has cooled after a stronger run.

If defense spending themes have your attention, it can be useful to see what else is moving in adjacent areas and check out 30 power grid technology and infrastructure stocks

With Northrop Grumman trading below the average analyst price target yet flagged with an intrinsic premium, the key question is whether recent share weakness is opening a new entry window or if markets are already pricing in future growth.

Most Popular Narrative: 8.5% Undervalued

The most followed narrative currently places Northrop Grumman’s fair value at about $736 per share, compared with the last close at $673.73, framing today’s pullback against a slightly higher long term anchor.

The ramp-up of advanced autonomous and integrated systems such as Beacon and IBCS, combined with ongoing investments in solid rocket motor capacity (targeting a near-doubling by 2029), positions the company to address high-growth, higher-margin market segments, which may support future operating margins and underlying cash flow.

Curious what sits behind that premium for advanced programs and cash generation potential? The narrative focuses on calibrated revenue growth, slightly tighter margins, and a future earnings multiple that still reflects sector strength without moving into extremes.

Result: Fair Value of $736.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on large U.S. defense programs staying on track and on international customers not shifting too quickly toward homegrown systems or competing platforms.

Find out about the key risks to this Northrop Grumman narrative.

Another Lens On Valuation

The analyst narrative leans on earnings forecasts and a future P/E of 27.8x to suggest Northrop Grumman is 8.5% below a fair value of about $736. In contrast, the SWS DCF model points to a present value closer to $531.66, which would frame today’s $673.73 price as expensive rather than discounted. Which set of assumptions do you trust more for your own work?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northrop Grumman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed, this is the moment to look through the assumptions, pressure test the forecasts, and weigh both sides of the story using 3 key rewards and 2 important warning signs

Ready To Hunt For Your Next Idea?

If Northrop Grumman is on your radar, it makes sense to widen the lens and line up a few other candidates that fit different roles in your portfolio.

- Target potential value opportunities by scanning a focused set of companies using the 58 high quality undervalued stocks.

- Prioritize resilience and sleep-better-at-night holdings by reviewing the 72 resilient stocks with low risk scores.

- Get ahead of the crowd by researching the screener containing 23 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com