- LIVE QUOTES

- LEARN

- HELP

EN

CAVA Group (CAVA) Is Up 6.7% After Another Earnings Beat And Resilient Same-Store Sales

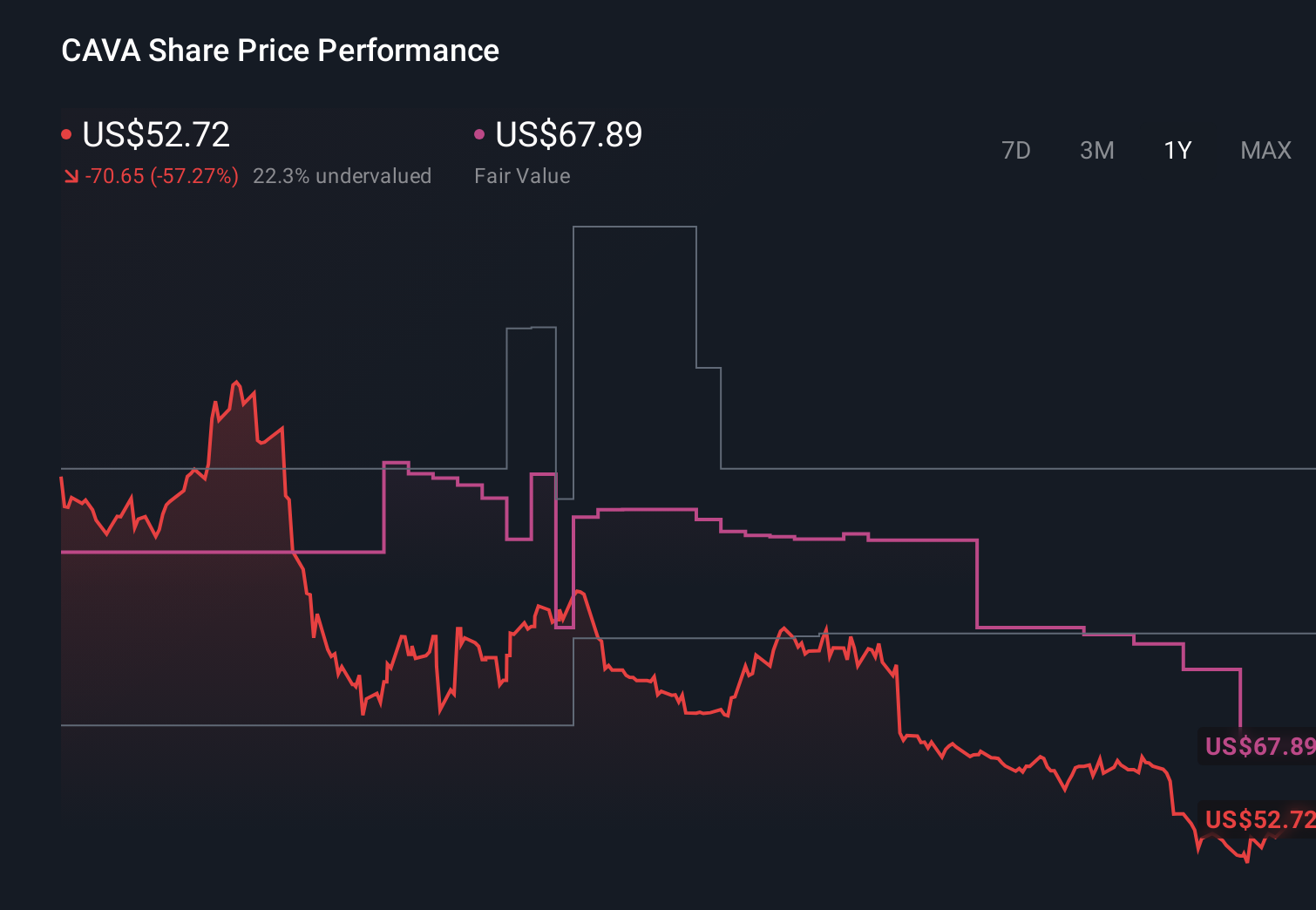

- CAVA Group recently reported record full-year revenue and another quarter of beating earnings and sales estimates, helped by lower menu prices and a 0.5% rise in same-restaurant sales despite broader industry weakness.

- This performance, led by CEO Brett Schulman and CFO Tricia Tolivar, highlights how customer-focused menu adjustments can support growth even as many competitors face softer demand.

- Next, we’ll examine how this ongoing earnings outperformance and operational resilience may influence CAVA’s existing investment narrative and outlook.

Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

CAVA Group Investment Narrative Recap

To own CAVA, you have to believe its fast casual Mediterranean concept can keep drawing traffic and support expanding to many more locations, while managing costs. The latest quarter of record revenue and another earnings beat reinforces the near term catalyst of unit growth and menu engagement, but it does not remove the key risk that softening same restaurant sales or higher costs could pressure margins and returns as the footprint grows.

The recent amendment to CAVA’s credit facility, which extends debt maturity to 2031 and doubles revolving commitments to US$150,000,000, is especially relevant here. It gives the company more financial flexibility to fund new restaurant openings and technology investments that underpin the growth story, but it also increases exposure to the risk that weaker traffic or thinner margins could make that added capital less productive over time.

Yet behind the strong quarter, investors should still be watching the risk that...

Read the full narrative on CAVA Group (it's free!)

CAVA Group's narrative projects $2.1 billion revenue and $119.1 million earnings by 2029. This requires 21.7% yearly revenue growth and a $55.4 million earnings increase from $63.7 million today.

Uncover how CAVA Group's forecasts yield a $84.00 fair value, in line with its current price.

Exploring Other Perspectives

Some of the lowest target analysts were already cautious, assuming revenue of about US$2.1 billion and earnings of roughly US$120.7 million by 2029, and they worry that rapid expansion plus possible menu fatigue could limit the benefit of results like this, which shows how differently you and other shareholders might weigh the same new data.

Explore 10 other fair value estimates on CAVA Group - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CAVA Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free CAVA Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CAVA Group's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 58 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com