- LIVE QUOTES

- LEARN

- HELP

EN

Should Marqeta’s (MQ) New AI Fraud Scoring Engine Require Action From Investors?

- In March 2026, Marqeta enhanced its Real-Time Decisioning platform with an AI-powered risk score that evaluates over 300 transaction attributes in milliseconds to help customers assess and manage fraud risk at the authorization stage.

- By combining machine learning with its existing rules engine and proprietary card program data, Marqeta aims to reduce fraud losses and false declines while tailoring risk controls to each customer’s unique transaction patterns.

- We’ll now explore how Marqeta’s new AI-driven risk scoring capability could influence its investment narrative and long-term risk services positioning.

We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Marqeta Investment Narrative Recap

To own Marqeta, you need to believe its modern card issuing platform can keep winning embedded finance demand while progressing toward profitability. The new AI-powered risk scoring fits that thesis by strengthening higher-margin risk services, but it does not directly change the near term focus on growing net revenue and managing ongoing customer concentration and pricing pressure risks.

Among recent developments, the appointment of Patti Kangwankij as CFO in February 2026 stands out here. Her payments background at Stripe and JPMorgan puts more attention on scaling Marqeta’s risk and compliance products, including Real-Time Decisioning, within the company’s push toward improved margins and the 2026 revenue and gross profit growth targets.

Yet despite these product gains, investors should also be aware that Marqeta’s heavy reliance on a small number of major customers still...

Read the full narrative on Marqeta (it's free!)

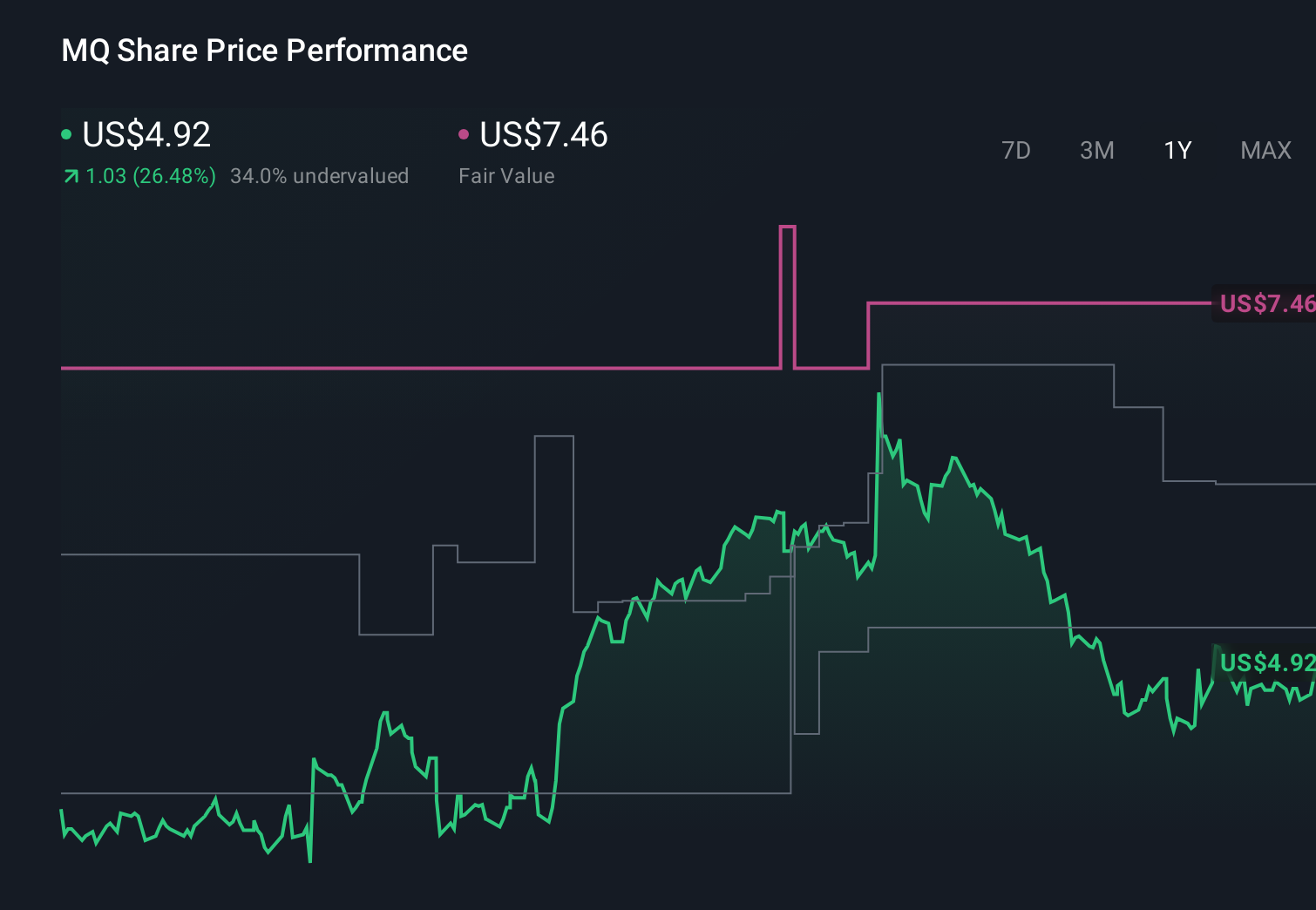

Marqeta's narrative projects $955.7 million revenue and $59.4 million earnings by 2029. This requires 15.2% yearly revenue growth and a $73.3 million earnings increase from -$13.9 million today.

Uncover how Marqeta's forecasts yield a $5.18 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue near US$1.0 billion and US$194.5 million in earnings by 2028, so this AI fraud upgrade could either reinforce or challenge that view, especially if you are weighing it against the risk that rising EU data rules might constrain how effectively Marqeta can use transaction data in the first place.

Explore 4 other fair value estimates on Marqeta - why the stock might be worth as much as 77% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Marqeta research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free Marqeta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Marqeta's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com