- LIVE QUOTES

- LEARN

- HELP

EN

EMCOR Group (EME) Is Up 6.1% After New US$500 Million Buyback And Dividend Move - Has The Bull Case Changed?

- In early April 2026, EMCOR Group’s board declared a regular quarterly cash dividend of US$0.40 per share, payable on April 30 to shareholders of record as of April 16, while investors also reacted to upbeat guidance and a new US$500.00 million share repurchase authorization.

- This combination of cash returns and confidence in future performance has sharpened focus on how EMCOR balances shareholder payouts with funding growth in areas like data center and infrastructure projects.

- We’ll now examine how EMCOR’s newly authorized US$500.00 million buyback could reshape its existing investment narrative around cash returns and growth.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

EMCOR Group Investment Narrative Recap

To own EMCOR Group, you need to believe it can keep turning complex electrical and mechanical projects in data centers and infrastructure into solid, repeatable earnings while managing labor and project risk. In the near term, the key catalyst is how upcoming earnings align with recent upbeat guidance, while the biggest risk remains cost pressure from labor and large projects. The new dividend and US$500.00 million buyback support confidence but do not fundamentally change these near term drivers.

The fresh US$500.00 million share repurchase authorization stands out most here, especially given EMCOR has already retired about 9.3% of its shares under the existing plan. If executed in line with past activity, this could modestly enhance per share metrics and support sentiment around its guidance, but it still sits alongside familiar execution risks in industrial, high tech, and oil and gas exposed projects.

Yet behind the strong recent return profile, investors should also weigh how rising wage pressures or persistent labor shortages could eventually affect...

Read the full narrative on EMCOR Group (it's free!)

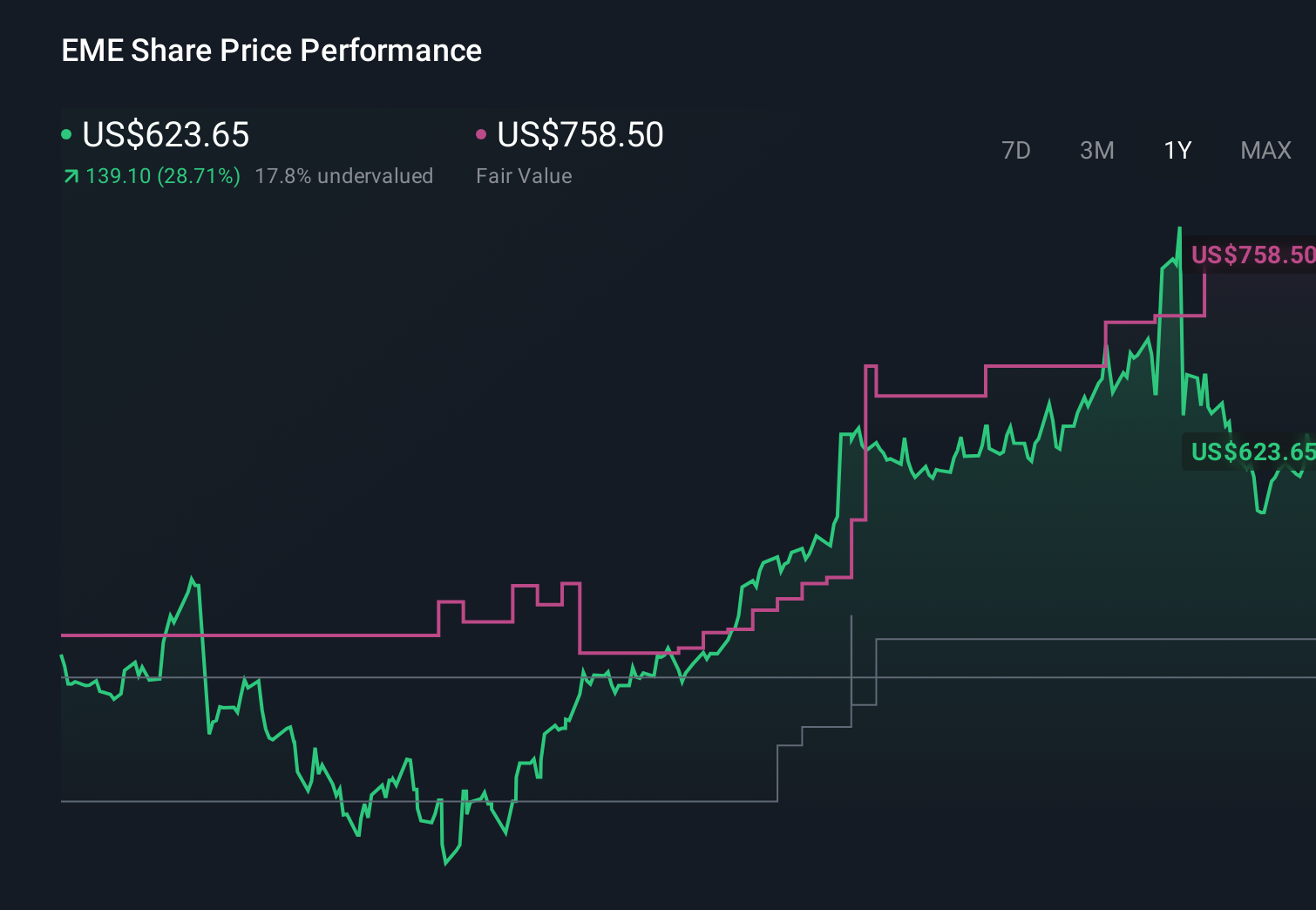

EMCOR Group's narrative projects $20.9 billion revenue and $1.6 billion earnings by 2029.

Uncover how EMCOR Group's forecasts yield a $869.29 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some analysts see a much brighter path than consensus, with bullish models once projecting around US$21.2 billion of revenue and US$1.4 billion of earnings by 2028. If EMCOR’s new buyback and guidance mark the early stages of that stronger scenario, you should recognize that this is a more optimistic narrative than the baseline and be open to comparing several viewpoints before deciding what you believe.

Explore 6 other fair value estimates on EMCOR Group - why the stock might be worth 32% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your EMCOR Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 59 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com