- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Why InterDigital (IDCC) Is Up 12.6% After New Wi‑Fi And TV Licensing Deals And What's Next

- In early April 2026, InterDigital, Inc. announced new patent license agreements with Buffalo Americas, Inc. for Wi‑Fi 5 and Wi‑Fi 6 network devices, alongside fresh licensing deals with a global TV manufacturer.

- These agreements broaden InterDigital’s coverage across networking and consumer electronics, reinforcing the breadth and relevance of its global patent portfolio.

- Next, we’ll explore how these newly signed licensing agreements, alongside growing recurring revenue confidence, may reshape InterDigital’s investment narrative.

Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

InterDigital Investment Narrative Recap

To own InterDigital, you need to believe its core wireless and video patent portfolio can keep converting into recurring, high‑margin licensing income across smartphones, PCs and connected devices. The Buffalo Americas Wi‑Fi 5/6 deal and the new TV manufacturer agreements appear directionally helpful for that thesis, but they do not fundamentally change the key near term swing factor, which is the timing and terms of major license renewals, or the biggest risk around evolving patent and FRAND regulation.

The most relevant recent development here is Jefferies’ focus on InterDigital’s path toward US$1,000,000,000 in annual recurring revenue, highlighting how each additional agreement can reinforce confidence in the scale and durability of royalty streams. The Buffalo Americas and TV licensing wins fit into this broader push beyond smartphones into networking and consumer electronics, which could matter for how investors reassess both the sustainability of current earnings and the sensitivity of the story to any shift in licensing rules.

Yet beneath these positives, investors should be aware that growing regulatory scrutiny of patent licensing could still...

Read the full narrative on InterDigital (it's free!)

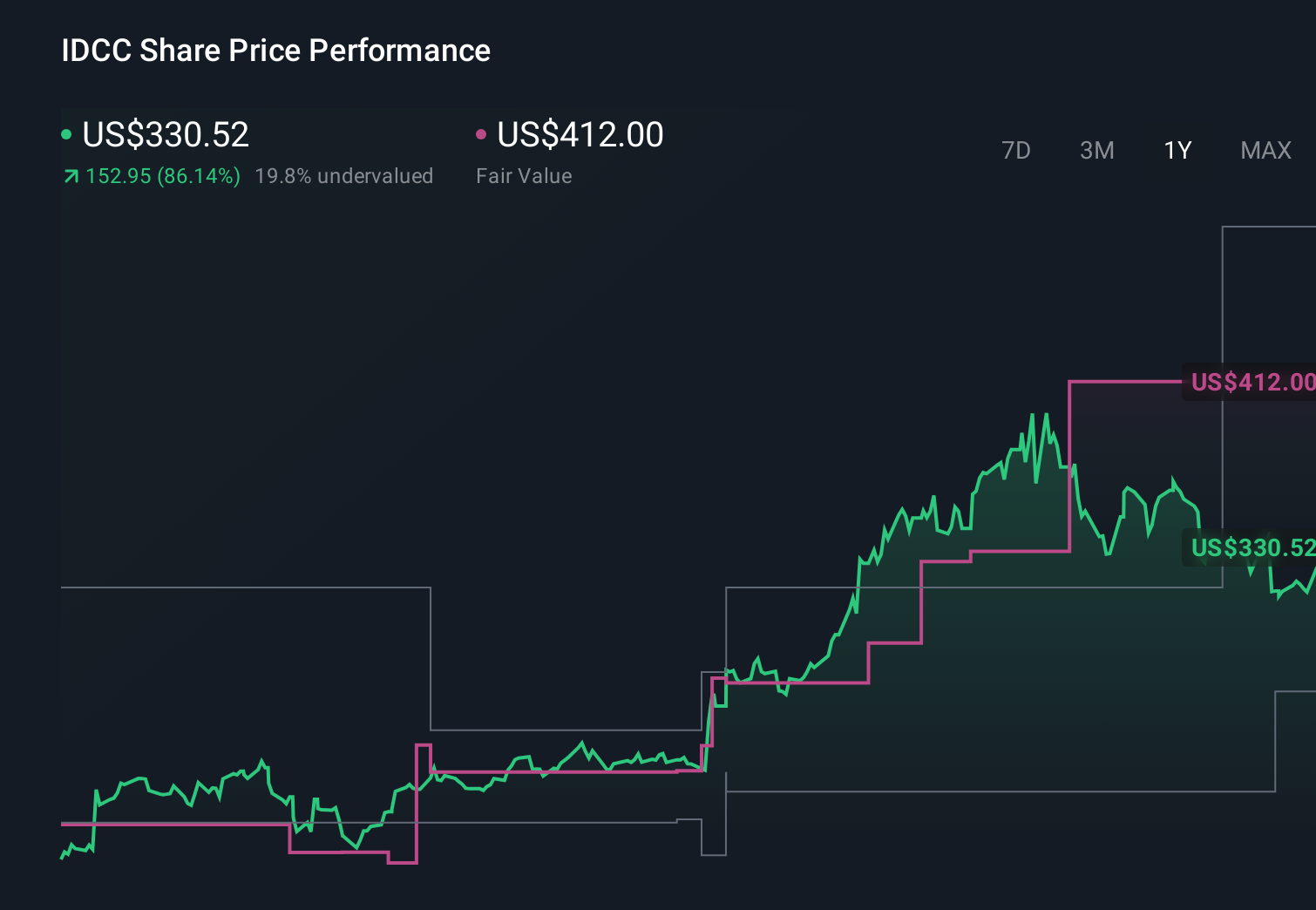

InterDigital's narrative projects $633.9 million revenue and $173.4 million earnings by 2028. This implies a 10.8% yearly revenue decline and a $290.1 million earnings decrease from $463.5 million today.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 31% upside to its current price.

Exploring Other Perspectives

While the baseline view stays cautious about recurring growth, the most optimistic analysts were already modeling roughly US$1,000,000,000 in revenue and almost US$488,000,000 in earnings by 2029, so news like the Buffalo and TV deals could push that bullish case further, or expose how differently you and they weigh long term IP and regulatory risks.

Explore 5 other fair value estimates on InterDigital - why the stock might be worth as much as 31% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com