- LIVE QUOTES

- LEARN

- HELP

EN

Will New Special-Mission Deals and Upgraded SkyCourier Capabilities Change Textron's (TXT) Narrative?

- Over the past week, Textron Aviation secured fresh defense and special-mission business with Belgium and the Peruvian Army, while also unveiling an in‑flight operable door for the Cessna SkyCourier that expands its military, humanitarian and commercial mission roles from around 2028.

- This combination of new international government customers and mission‑enhancing product features underlines how Textron is deepening its role in specialized defense and relief aviation.

- We’ll now examine how Belgium’s selection of the Cessna SkyCourier for Special Operations Forces could influence Textron’s broader investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Textron Investment Narrative Recap

To own Textron, you need to believe its mix of aviation, defense and industrial businesses can turn steady program execution into dependable earnings growth, while managing cost and product mix pressures. The Belgian SkyCourier order and Peruvian King Air 360C deal support the near term aviation and defense demand story, but they do not materially change the key catalyst around execution in Bell and Aviation or the ongoing risk of margin pressure from weaker segments.

The most relevant update here is Belgium’s decision to add five Cessna SkyCouriers to its Special Operations Forces fleet, marking the aircraft’s entry into the global defense market. This aligns with the broader catalyst of Textron’s defense exposure, where investors are watching how new platforms and variants, such as the in flight operable SkyCourier door from 2028, might complement larger programs like FLRAA and support higher utilization of the aviation installed base.

But against this encouraging defense traction, investors should also be aware of the risk that Textron’s segment mix and cost structure could still...

Read the full narrative on Textron (it's free!)

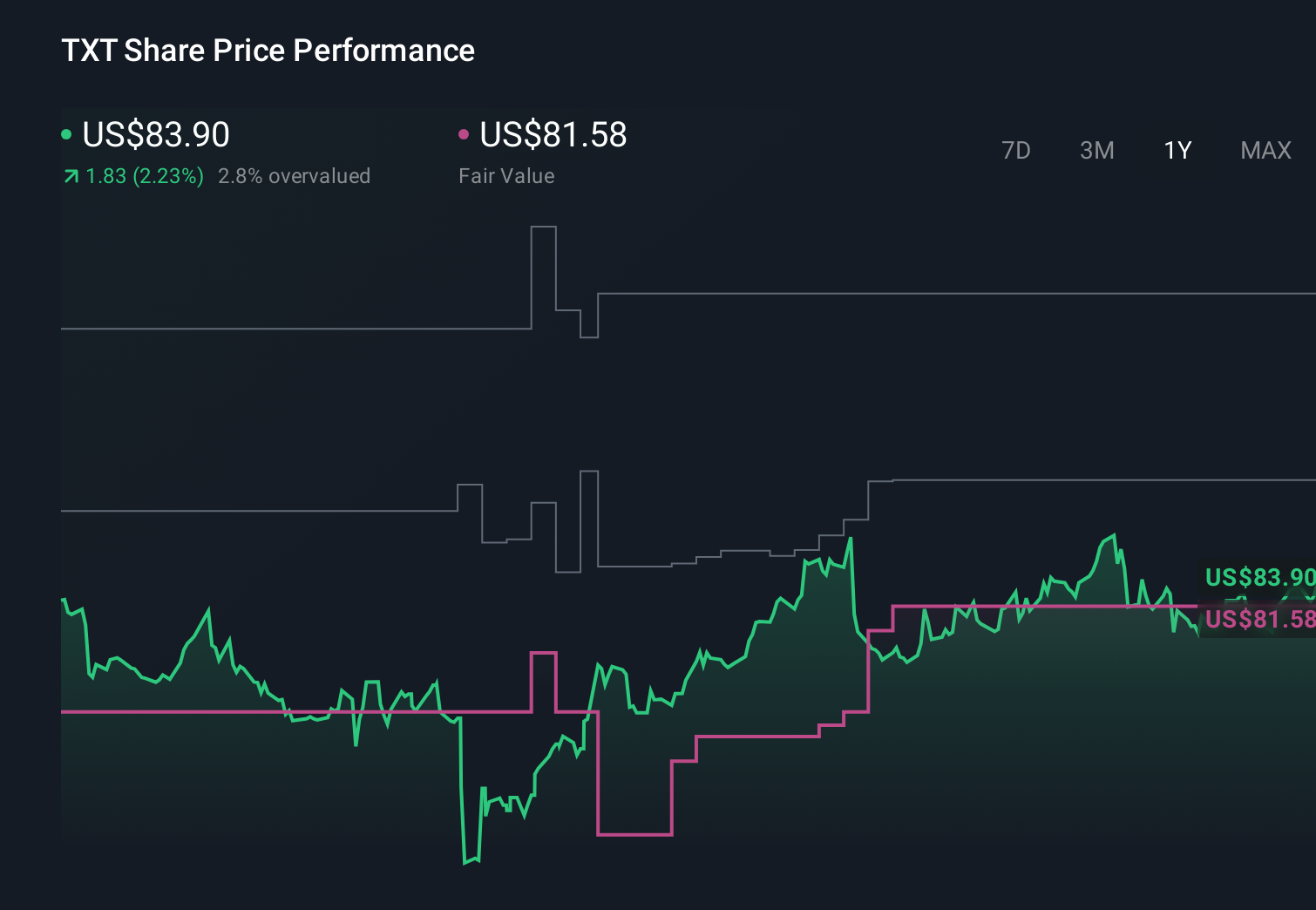

Textron's narrative projects $16.7 billion revenue and $1.2 billion earnings by 2029. This requires 4.2% yearly revenue growth and an earnings increase of about $277 million from $923.0 million today.

Uncover how Textron's forecasts yield a $98.95 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Textron could reach about US$17.3 billion of revenue and US$1.2 billion of earnings by 2029, so if you see rising defense-contract dependence as a key risk, this new Belgium and Peru news might either reinforce that concern or suggest upside that those forecasts did not fully capture.

Explore 5 other fair value estimates on Textron - why the stock might be worth 17% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Textron research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Textron research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Textron's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 62 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com