- LIVE QUOTES

- LEARN

- HELP

EN

How Investors Are Reacting To MINISO Group Holding (MNSO) Rising Sales, Weaker Earnings and Bigger Dividends

- MINISO Group Holding Limited reported fourth-quarter 2025 results showing higher sales of CNY 6,254.07 million but a net loss of CNY 141.52 million, while for the full year sales rose to CNY 21,443.83 million alongside lower net income of CNY 1,205.05 million, and it completed a HK$ 632.51 million repurchase of 19,003,004 shares representing 6.17% of its share base.

- Despite weaker profitability and higher impairment losses in 2025, the company increased shareholder payouts with a US$ 0.0941 final ordinary dividend and a US$ 0.3664 semi-annual dividend declared for payment in April and May 2026.

- Against this backdrop of rising sales but weaker earnings, we’ll explore how the richer dividend payouts might reshape MINISO’s investment narrative.

We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

MINISO Group Holding Investment Narrative Recap

To own MINISO, you need to believe its offline, IP-led lifestyle format can keep growing globally without eroding margins, even as competition and costs rise. This latest set of results highlights that the key near term catalyst is still revenue growth from new stores and IP products, while the biggest risk is that weaker profitability and rising impairments persist; the 2025 numbers suggest that risk has become more visible, but not thesis-breaking on their own.

Among the recent announcements, the completion of the HK$632.51 million buyback, retiring 6.17% of shares, stands out. Combined with higher dividends, it points to a capital return profile that could amplify any future earnings recovery per share, but it also raises the bar for management to control costs and avoid further impairment-driven hits that might undercut those shareholder returns.

Yet beneath the higher dividends and completed buyback, there is a separate risk investors should be aware of around rising impairments and...

Read the full narrative on MINISO Group Holding (it's free!)

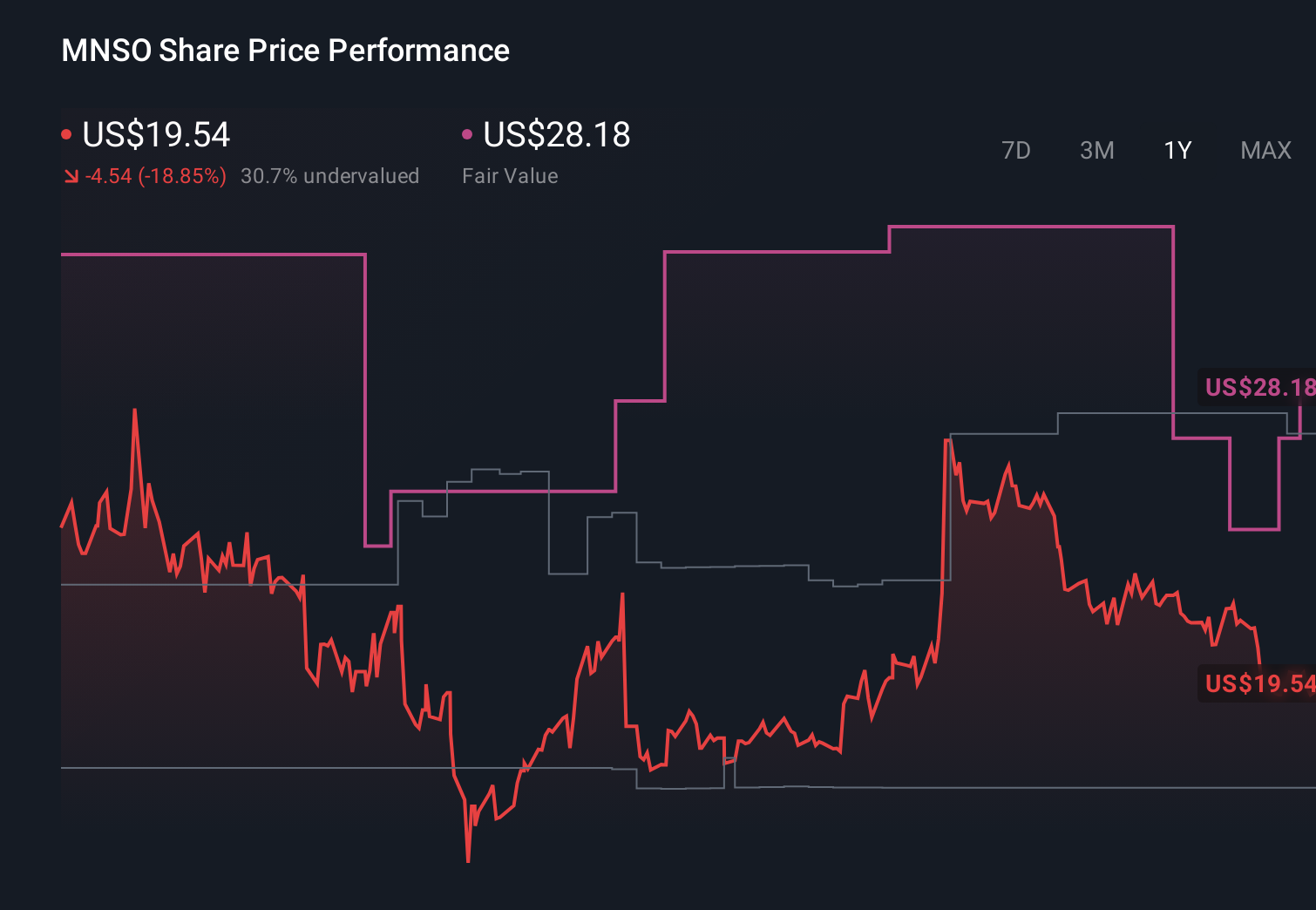

MINISO Group Holding's narrative projects CN¥31.7 billion revenue and CN¥4.9 billion earnings by 2028. This requires 19.4% yearly revenue growth and a CN¥2.5 billion earnings increase from CN¥2.4 billion today.

Uncover how MINISO Group Holding's forecasts yield a $26.87 fair value, a 65% upside to its current price.

Exploring Other Perspectives

The most cautious analysts were already assuming only about CN¥28.8 billion of revenue and CN¥4.0 billion of earnings by 2028, so this setback may strengthen their view that offline focused expansion and cost pressures could prove more problematic than the consensus expects.

Explore 7 other fair value estimates on MINISO Group Holding - why the stock might be worth just $23.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MINISO Group Holding research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MINISO Group Holding research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MINISO Group Holding's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com