- LIVE QUOTES

- LEARN

- HELP

EN

How NOV’s US$200 Million Brazil Expansion Plan Will Impact NOV (NOV) Investors

- NOV Inc. recently announced it will invest US$200,000,000 over the next three years to roughly double capacity at its subsea flexible pipe manufacturing facility in Açu, Brazil, which has been running near full utilization with a backlog stretching well into 2028 and will add about US$50,000,000 to the company’s 2026 capital expenditure plan.

- This expansion underscores how sustained demand for subsea flexible pipe is influencing NOV’s long-term capital allocation, potentially reshaping the balance between growth investment and cash available for other corporate priorities.

- We’ll now explore how NOV’s decision to roughly double Brazilian subsea pipe capacity could influence its existing investment narrative and risk profile.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

NOV Investment Narrative Recap

To own NOV today, you need to believe its offshore and energy infrastructure exposure can translate a solid backlog into better margins and cleaner earnings over time. The Brazil subsea pipe expansion supports that backlog story in a specific niche, but in the near term it also increases capital intensity and may heighten sensitivity to any pullback in offshore final investment decisions, leaving project delays and pricing pressure as key risks.

Among recent developments, the 20% dividend increase to US$0.09 per share stands out alongside this new US$200,000,000 capex commitment. Together, they show NOV balancing reinvestment in capacity with direct cash returns to shareholders, which matters if your short term focus is on earnings quality and capital return discipline while the offshore and international upcycle thesis plays out.

But while higher capacity and a bigger dividend sound encouraging, investors should be aware that...

Read the full narrative on NOV (it's free!)

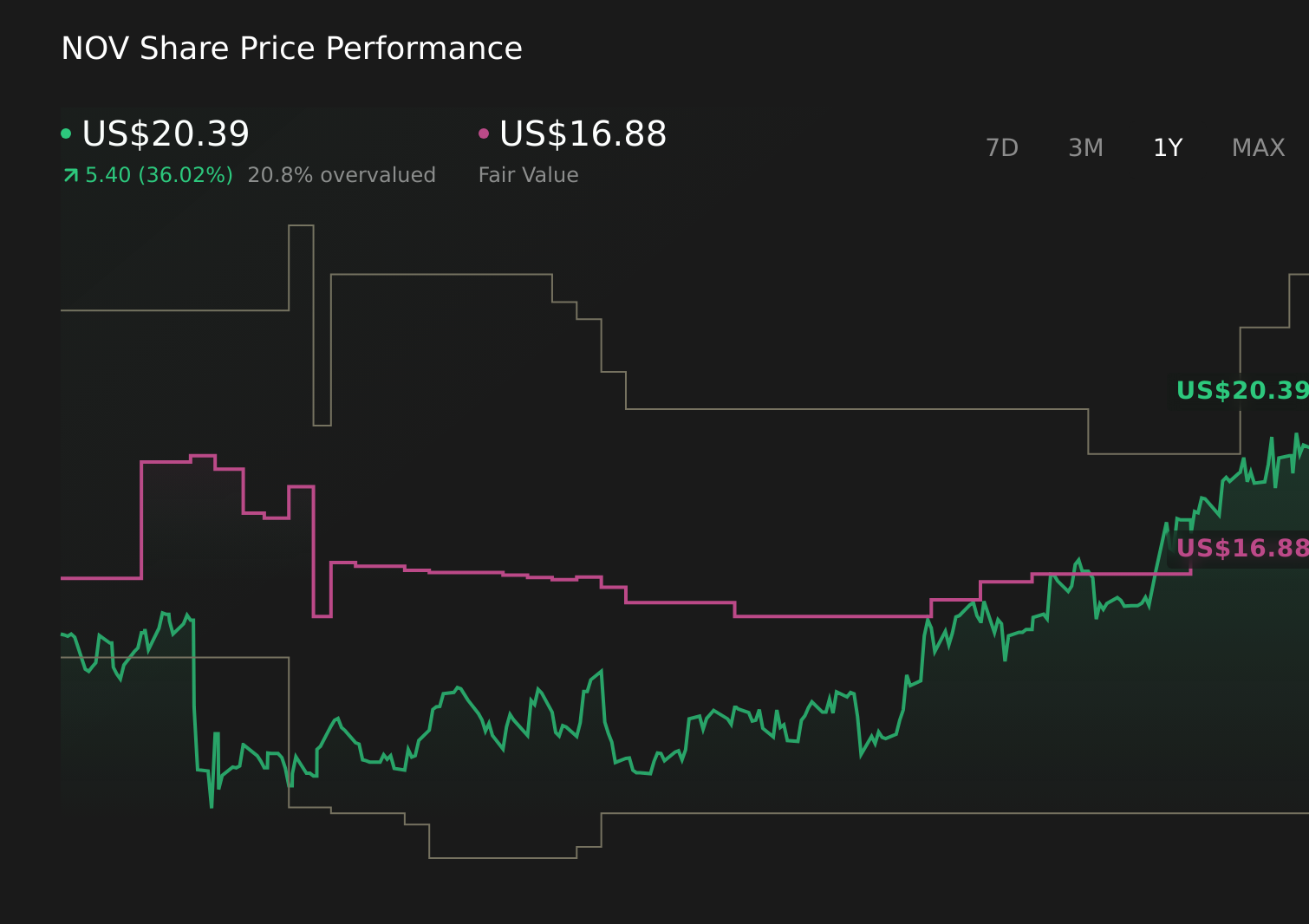

NOV's narrative projects $9.3 billion revenue and $511.2 million earnings by 2029.

Uncover how NOV's forecasts yield a $20.10 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling about US$9.4 billion of revenue and US$587.9 million of earnings by 2029, yet the Brazil expansion and rising cost inflation risk show how quickly those expectations could be revised, so it makes sense for you to compare these bullish assumptions with more cautious views before deciding what fits your own outlook.

Explore 5 other fair value estimates on NOV - why the stock might be worth 13% less than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NOV research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

- Our free NOV research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NOV's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com