- LIVE QUOTES

- LEARN

- HELP

EN

Top Growth Stocks With Strong Insider Confidence

Over the last 7 days, the United States market has risen by 1.2%, contributing to a remarkable 33% increase over the past year, with earnings forecasted to grow by 16% annually. In this thriving environment, growth stocks with high insider ownership often signal strong confidence from those closest to the company, making them worth considering for their potential alignment with current market trends.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Upstart Holdings (UPST) | 13% | 53.5% |

| Precigen (PGEN) | 11.9% | 68.4% |

| Karman Holdings (KRMN) | 17.2% | 53.2% |

| GBank Financial Holdings (GBFH) | 27.3% | 42.2% |

| Enovix (ENVX) | 11.3% | 41.1% |

| Clene (CLNN) | 13.2% | 62.2% |

| Caledonia Mining (CMCL) | 14.3% | 28.4% |

| Better Home & Finance Holding (BETR) | 20.6% | 97.4% |

| Astera Labs (ALAB) | 10.5% | 29.0% |

| AppLovin (APP) | 27.3% | 21.4% |

We're going to check out a few of the best picks from our screener tool.

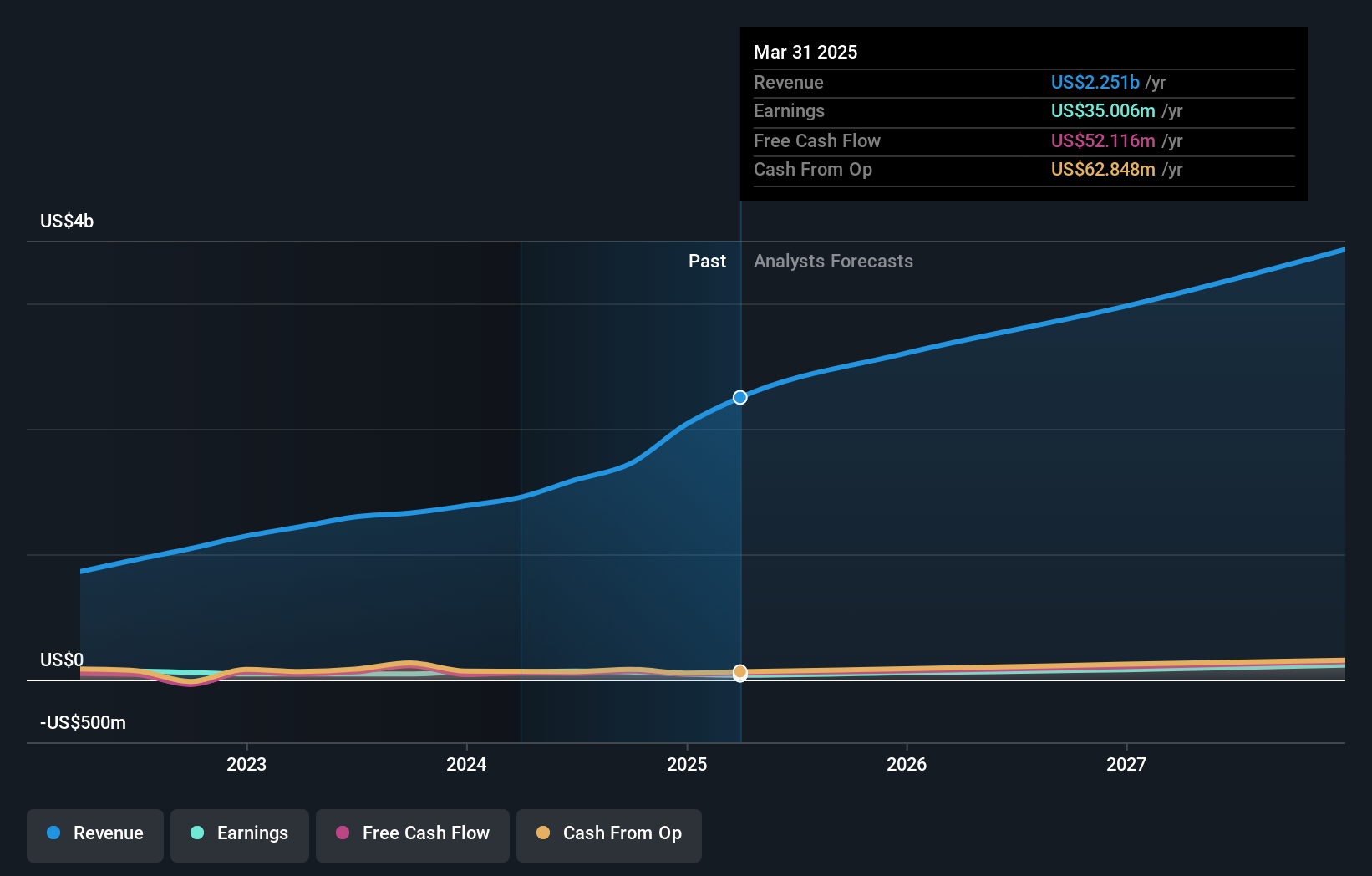

Astrana Health (ASTH)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Astrana Health, Inc. is a healthcare management company that offers medical care services in the United States and has a market cap of approximately $1.29 billion.

Operations: Astrana Health generates revenue through three primary segments: Care Delivery ($250.74 million), Care Partners ($3.02 billion), and Care Enablement ($246.66 million).

Insider Ownership: 10.8%

Earnings Growth Forecast: 30.3% p.a.

Astrana Health demonstrates potential as a growth company with high insider ownership. Recent earnings showed significant revenue growth to US$950.53 million in Q4 2025, with a turnaround from a net loss to US$6 million net income. Despite volatile share prices and lower profit margins, earnings are forecasted to grow significantly at 30.3% annually, outpacing the broader market. However, interest payments remain poorly covered by earnings and recent filings indicate delayed SEC submissions and increased buyback plans totaling $100 million authorization.

- Dive into the specifics of Astrana Health here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that Astrana Health is priced lower than what may be justified by its financials.

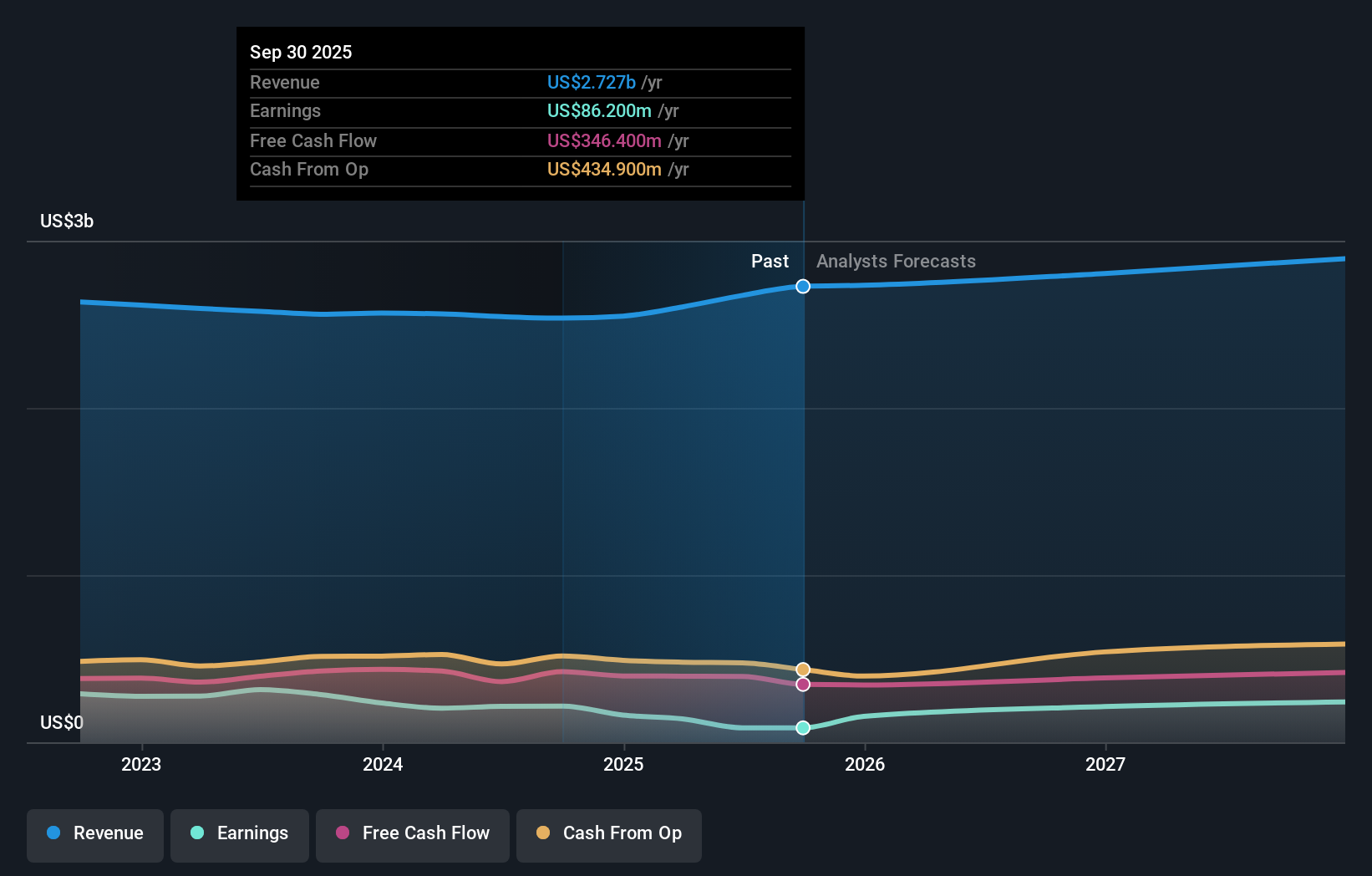

Playtika Holding (PLTK)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Playtika Holding Corp. develops mobile games across various regions including the United States, Europe, and Asia Pacific, with a market cap of approximately $1.21 billion.

Operations: The company's revenue is primarily derived from its Computer Graphics segment, which generated $2.76 billion.

Insider Ownership: 27%

Earnings Growth Forecast: 66.4% p.a.

Playtika Holding is exploring strategic alternatives to enhance shareholder value, with Morgan Stanley advising. Despite a high debt level and negative equity, the company trades at a good value compared to peers. Earnings are expected to grow significantly by 66.4% annually, with profitability anticipated in three years. However, revenue growth lags behind the market at 1.5% per year, and its dividend yield of 12.74% is not well covered by earnings.

- Click to explore a detailed breakdown of our findings in Playtika Holding's earnings growth report.

- The valuation report we've compiled suggests that Playtika Holding's current price could be quite moderate.

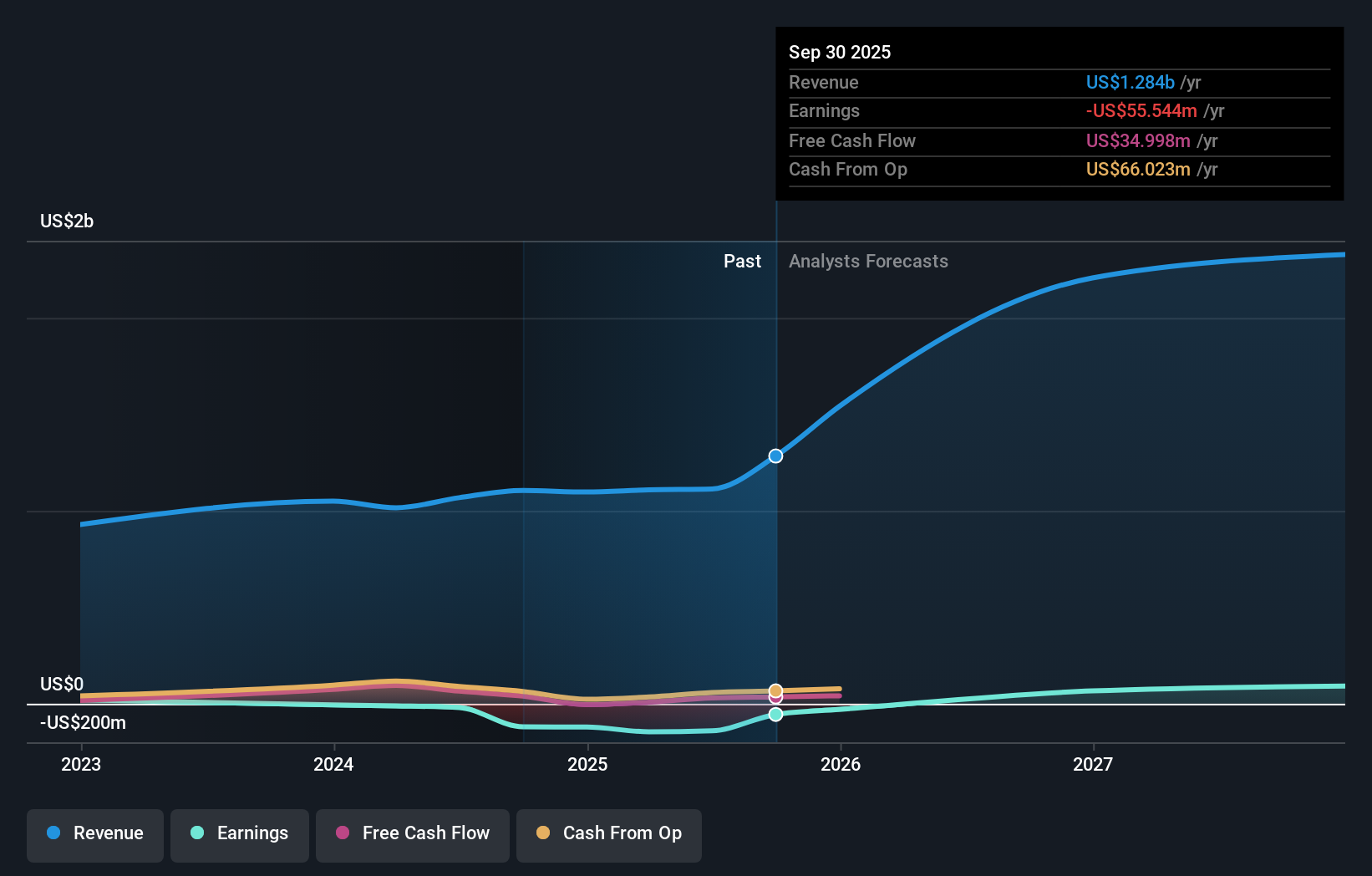

TIC Solutions (TIC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TIC Solutions, Inc. offers critical asset integrity services in North America and has a market cap of $1.57 billion.

Operations: The company's revenue segments include Geospatial services generating $131.26 million, Consulting Engineering contributing $300.15 million, and Inspection and Mitigation providing $1.10 billion in revenue.

Insider Ownership: 11.3%

Earnings Growth Forecast: 110.1% p.a.

TIC Solutions is trading significantly below its estimated fair value, indicating potential undervaluation. Despite a substantial net loss reduction from the previous year, revenue growth of 39.4% outpaces the US market average. The company anticipates profitability within three years, with earnings projected to grow over 110% annually. Recent leadership change sees Benjamin Heraud as CEO, and a $200 million share repurchase program has been announced alongside a $500 million shelf registration filing for future capital needs.

- Click here and access our complete growth analysis report to understand the dynamics of TIC Solutions.

- Upon reviewing our latest valuation report, TIC Solutions' share price might be too pessimistic.

Where To Now?

- Reveal the 205 hidden gems among our Fast Growing US Companies With High Insider Ownership screener with a single click here.

- Seeking Other Investments? Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com