- LIVE QUOTES

- LEARN

- HELP

EN

Did EPD’s Earnings Beat and Valuation Gap Just Shift Enterprise Products Partners' Investment Narrative?

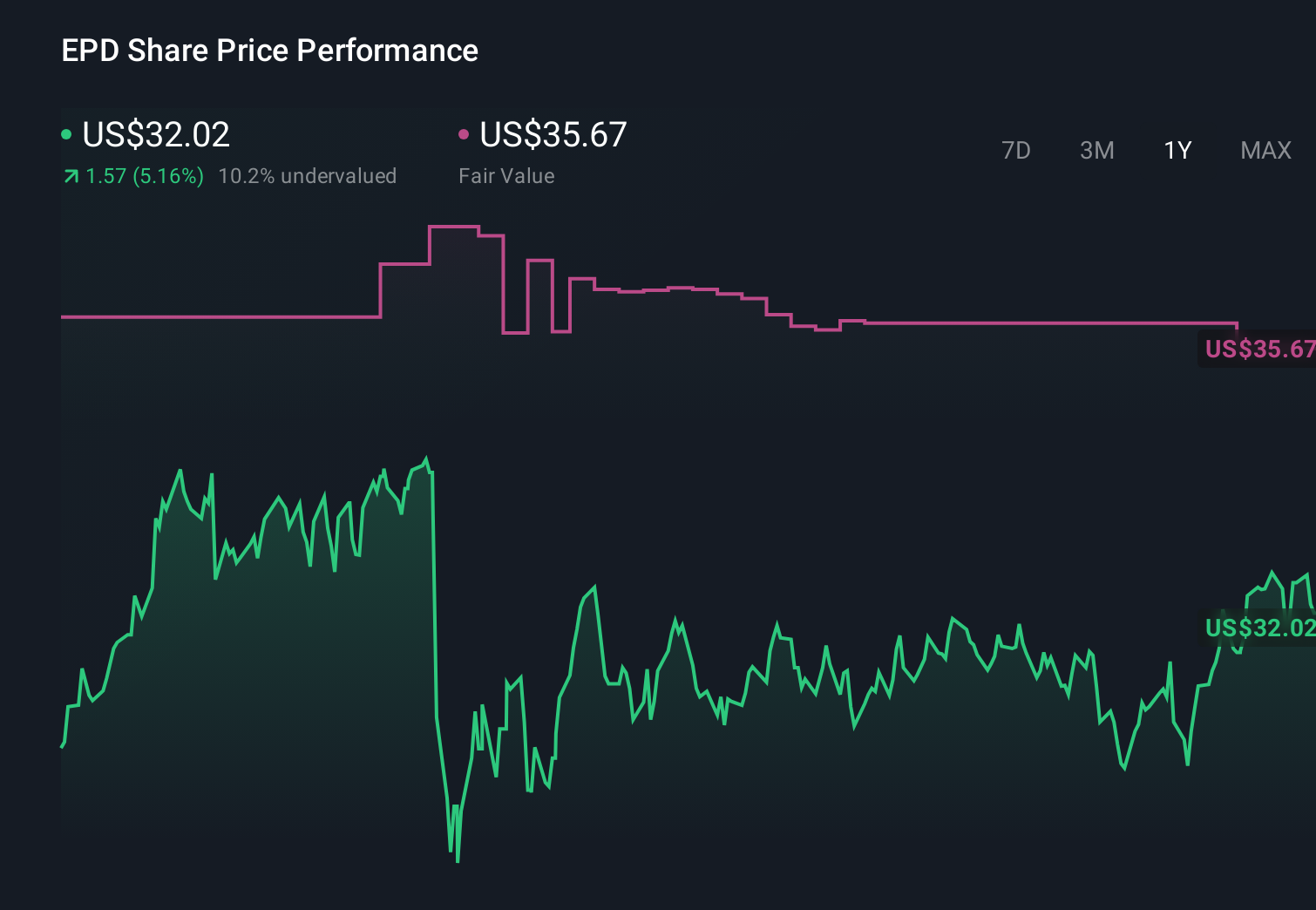

- Enterprise Products Partners recently presented at the World Chemical Forum 2026, while also reporting quarterly revenue and earnings that surpassed analyst expectations and prompted positive estimate revisions.

- What stands out is that analysts now see the partnership’s earnings outlook improving even as it continues to trade at a discount to peers, highlighting a perceived gap between fundamentals and valuation.

- With this strong earnings surprise and upgraded forecasts in mind, we’ll now explore how the news affects Enterprise Products Partners’ broader investment narrative.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to believe in the durability of its fee-based midstream model and the payoff from its ongoing capacity expansions. The latest earnings beat and higher analyst estimates support that near term earnings outlook, but do not materially change the key short term catalyst of bringing new Permian processing and export projects online, or the biggest risk around its sizable US$31.9 billion debt load.

The most relevant update here is Mizuho’s higher US$44 price target following management’s guidance for double digit adjusted EBITDA growth in 2027 tied to organic growth projects. That ties directly into the project completion catalyst, as investors are watching how efficiently Enterprise converts its large capital program into higher throughput and export volumes without adding undue balance sheet strain.

Yet even with improving earnings expectations, investors should be aware that Enterprise’s high debt levels could become more challenging if ...

Read the full narrative on Enterprise Products Partners (it's free!)

Enterprise Products Partners' narrative projects $58.4 billion revenue and $7.1 billion earnings by 2029. This requires 3.6% yearly revenue growth and a $1.3 billion earnings increase from $5.8 billion.

Uncover how Enterprise Products Partners' forecasts yield a $38.24 fair value, in line with its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community value Enterprise Products Partners between US$34 and about US$91 per unit, showing very different expectations for its potential. When you set those views against the importance of bringing new processing and export projects online, it underlines how differently people weigh growth opportunities versus execution risks, and why it can be useful to compare several perspectives before forming your own view.

Explore 8 other fair value estimates on Enterprise Products Partners - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com