- LIVE QUOTES

- LEARN

- HELP

EN

Assessing ProPetro (PUMP) Valuation As PROPWR Expansion Supports Results And Investor Interest

Why recent ProPetro moves have investors paying closer attention

ProPetro Holding (PUMP) has drawn fresh attention after its industrialized model and core completions business generated solid results and free cash flow, even as slower completions activity and tariff pressures weighed on the sector.

At the same time, the growing role of the PROPWR platform in the overall business has added a new angle for investors. It highlights how ProPetro is balancing its legacy hydraulic fracturing operations with newer power generation opportunities.

See our latest analysis for ProPetro Holding.

ProPetro’s recent quarterly update and focus on its PROPWR platform have come alongside a strong 90-day share price return of 45.44% and a very large 1-year total shareholder return of 161.03%. However, the 7-day share price return of 6.28% suggests some of that momentum has cooled in the near term.

If you are comparing ProPetro with other energy related names tied to infrastructure and power demand, it can be useful to scan for companies linked to the broader build out of grid and power systems using our 27 power grid technology and infrastructure stocks

With a 1 year total shareholder return above 160%, annual revenue growth of 8.22% and net income growth near 94%, plus an intrinsic value estimate that sits about 28% above the current price, is ProPetro still mispriced, or has the market already baked in future gains?

Most Popular Narrative: 1.9% Undervalued

With ProPetro’s fair value narrative sitting at $14.00 against a last close of $13.73, the gap is small, but the story behind it is detailed.

Early traction and long-term visibility in the PROPWR power business, including the recent 10-year, 80-megawatt contract and confidence in fully deploying 220 megawatts by end of 2025, expands addressable markets and creates a stable, recurring cash flow stream, expected to drive sustained revenue and margin growth.

Curious how a power platform this small in reported revenue can still sit at the center of the fair value story? The narrative leans heavily on future cash generation, margin lift from next generation fleets, and a valuation multiple that assumes the earnings profile looks very different a few years from now.

Result: Fair Value of $14.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on completions activity and PROPWR scaling according to plan, while fleet oversupply and a concentrated customer base could quickly pressure both utilization and margins.

Find out about the key risks to this ProPetro Holding narrative.

Another Angle on Valuation

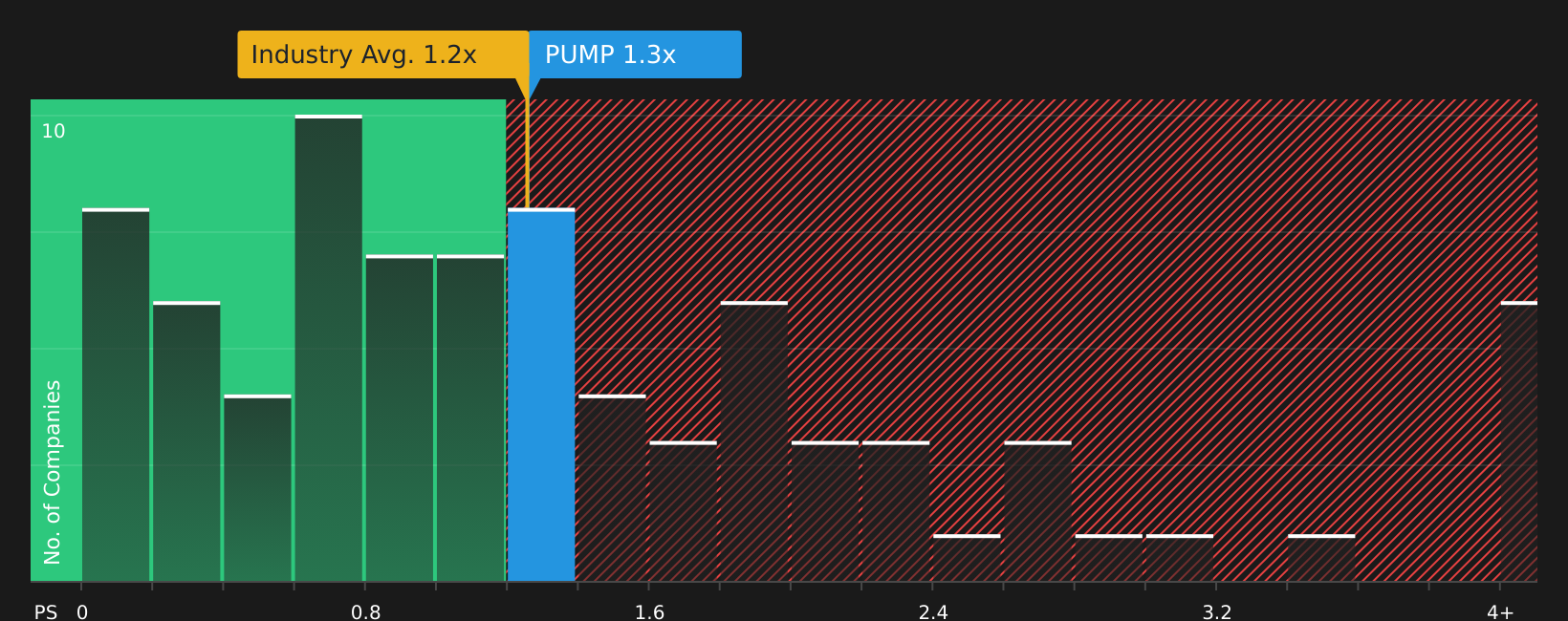

The fair value story built on future cash flows suggests ProPetro is trading about 28% below an intrinsic value estimate of $19.11. However, on a simple P/S of 1.3x versus a fair ratio of 0.9x and a peer average of 1.1x, the stock screens as expensive, so which signal matters more to you?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on value and the PROPWR story still taking shape, do you feel the balance of risk and reward suits your style or not? Move quickly, review the numbers yourself, and let the full picture guide you using the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If ProPetro has piqued your interest, do not stop here. The next step is seeing how it stacks up against other opportunities across quality, value, and resilience.

- Target future compounders by scanning a curated list of companies that look attractively priced on fundamentals with the 62 high quality undervalued stocks

- Protect your capital by focusing on companies that pair healthier balance sheets with earnings support using the solid balance sheet and fundamentals stocks screener (40 results)

- Hunt for under-the-radar names with strong underlying metrics before they are widely discussed through the screener containing 25 high quality undiscovered gems

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com