- LIVE QUOTES

- LEARN

- HELP

EN

Is Watts Water Technologies (WTS) Still Attractive After Recent Pullback And Strong Five Year Run?

- If you are wondering whether Watts Water Technologies is priced attractively at its recent levels, the starting point is understanding what the current market price is implying about its future.

- The share price recently closed at US$287.95, with returns of 1.5% over 7 days, a 5.9% decline over 30 days, 3.4% year to date, 58.6% over 1 year, 87.8% over 3 years, and 151.1% over 5 years.

- Recent coverage of the company has focused on its role within capital goods and water-related solutions. This helps explain why investors are paying close attention to how the stock is priced, and that context matters when you look at both the shorter term pullback and the longer term returns.

- On Simply Wall St's 6 point valuation framework, Watts Water Technologies currently has a valuation score of 2 out of 6. The next step is to compare what different valuation approaches say about the stock, and then consider a more complete way to think about value that comes at the end of this article.

Watts Water Technologies scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Watts Water Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business might be worth today by projecting its future cash flows and discounting them back to a present value using a required return.

For Watts Water Technologies, the model uses a 2 Stage Free Cash Flow to Equity approach based on projected free cash flows in $. The latest twelve month free cash flow is about $362 million. Analyst inputs cover the next few years, with Simply Wall St extending those projections further out. By 2029, free cash flow is projected at $528.8 million, with additional estimates running through 2035.

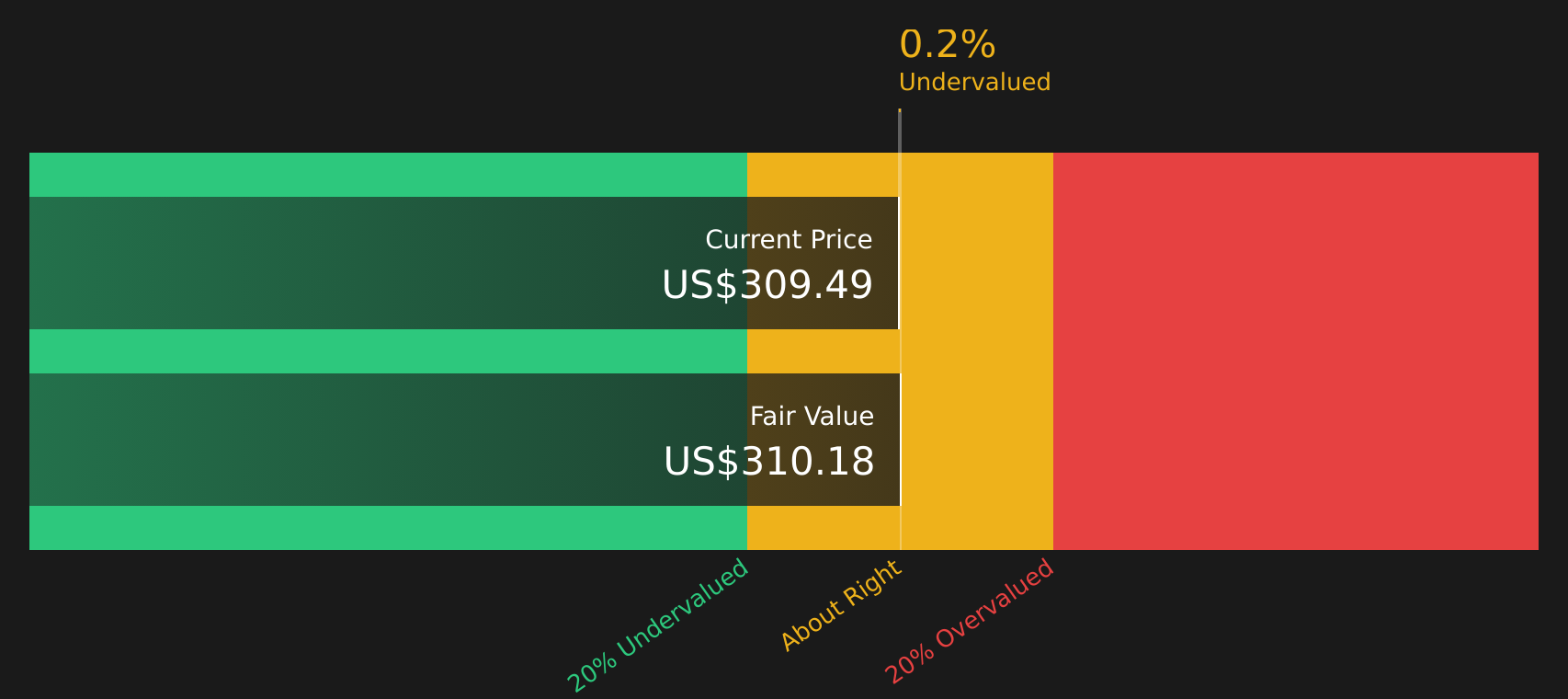

Combining these cash flow projections and discounting them back results in an estimated intrinsic value of about $312.39 per share. Compared with the recent share price of $287.95, the model implies the stock is about 7.8% undervalued, which sits within a reasonable margin of error for this type of analysis.

Result: ABOUT RIGHT

Watts Water Technologies is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Watts Water Technologies Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it links what you pay for each share directly to the earnings that business is currently generating. It helps you see how many dollars the market is willing to pay today for one dollar of current earnings.

What counts as a “normal” P/E will vary. Higher expected earnings growth or lower perceived risk often justify a higher multiple, while slower growth or higher risk typically point to a lower one. This is why simple comparisons need some context.

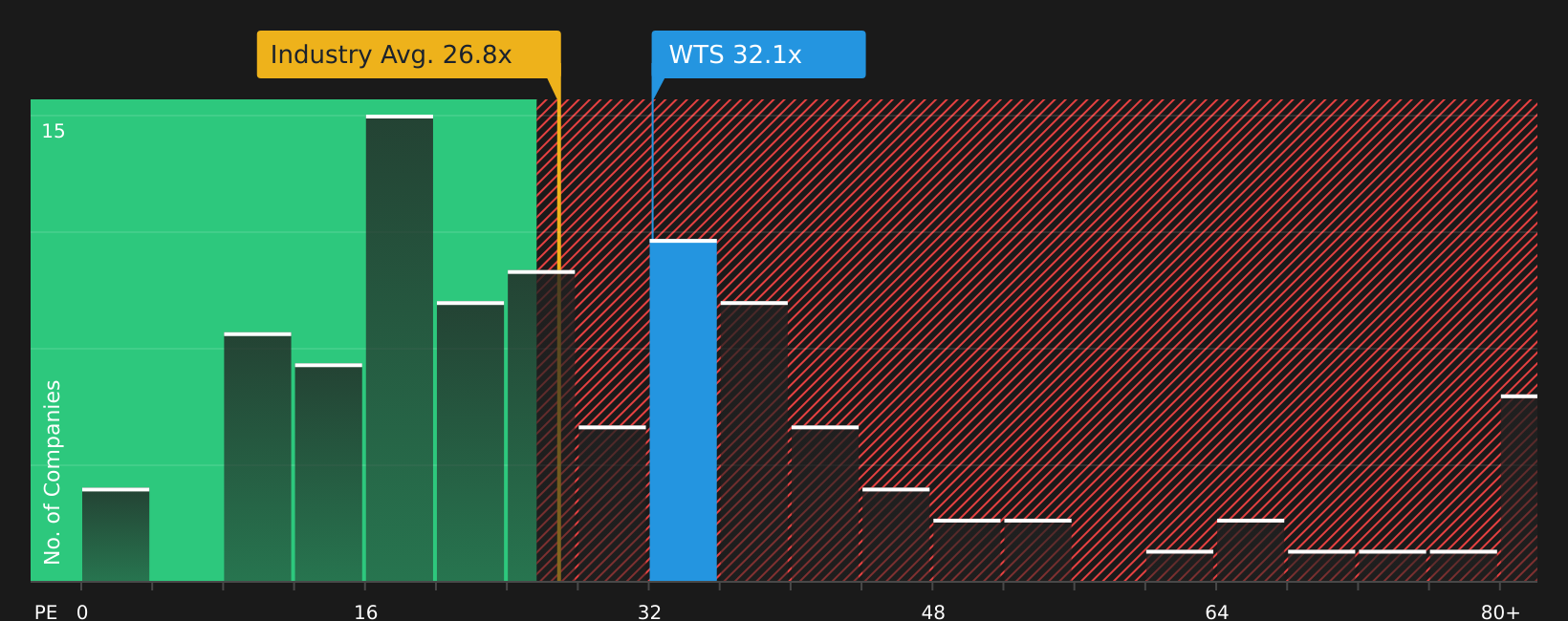

Watts Water Technologies currently trades on a P/E of 28.17x. That is above the Machinery industry average of about 26.21x and below the peer average of 31.10x. Simply Wall St’s proprietary “Fair Ratio” for Watts Water Technologies is 22.77x, which is the P/E level implied by factors such as its earnings growth profile, profit margins, size, risks and industry.

This Fair Ratio is designed to be more tailored than a basic peer or industry comparison because it adjusts for company specific characteristics rather than treating all Machinery stocks as the same. Comparing the current P/E of 28.17x with the Fair Ratio of 22.77x suggests the shares are pricing in more optimism than this framework implies.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Watts Water Technologies Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring your view of Watts Water Technologies together with the numbers by tying a simple story about the business to a set of revenue, earnings and margin estimates. This is translated into a fair value you can compare with the current price, all within an easy tool on Simply Wall St's Community page that updates when new information such as news or earnings arrives. For example, one investor might align with a cautious fair value around US$278.79 that reflects concerns about mature markets and margin pressure, while another might lean toward a more optimistic fair value closer to US$340 that reflects confidence in acquisitions, digital offerings and a higher future P/E. Each of those Narratives clearly links its story, forecast and fair value so you can decide how the gap between fair value and price fits your own decision on when to act.

For Watts Water Technologies however, we will make it really easy for you with previews of two leading Watts Water Technologies Narratives:

🐂 Watts Water Technologies Bull Case

Fair value: US$338.56

Implied undervaluation vs last close: 15.0%

Revenue growth assumption: 6.8%

- Focuses on growth in intelligent water management, regulatory demand and acquisitions supporting recurring revenue and margins.

- Highlights investments in automation, supply chain and tariff management that are intended to support cost efficiency and resilience.

- Assumes analysts' earnings and margin forecasts, along with their price target range, are broadly consistent with the current share price.

🐻 Watts Water Technologies Bear Case

Fair value: US$278.79

Implied overvaluation vs last close: 3.3%

Revenue growth assumption: 6.8%

- Raises concerns about reliance on mature Western markets, competition and potential pressure on traditional product demand.

- Flags risks from regulatory costs, infrastructure spending timing and possible margin compression if pricing or growth falls short of expectations.

- Still recognises support from acquisitions, U.S. manufacturing and recurring revenue, but views the current share price as leaving limited room for disappointment.

Once you have a sense of which story feels closer to your own expectations, you can build or adjust a personal narrative that matches your revenue, margin and P/E assumptions. You can then compare that fair value with the current share price to judge whether the gap is attractive enough for your next move.

Do you think there's more to the story for Watts Water Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com